Mapping PSI Rules into Your Firm’s Workflow: From Client Onboarding to Year‑End Review

Mapping PSI rules into your firm’s workflow, from client onboarding to year‑end review, helps you manage personal services income in a consistent, low‑stress way. When you build simple steps for personal services income (PSI) into each stage of your process, you reduce the risk that special tax rules will be overlooked or applied late.

Why Personal Services Income Needs a Structured Workflow

PSI can affect how tax obligations are calculated, which tax deductions can be claimed and how much taxable income a person needs to report. It applies where income received is mainly a reward for someone’s own personal efforts or skills, rather than from an income producing asset, a large team or their business structure. Because PSI can arise in almost any industry and with many types of personal services, firms that work with contractors and small business clients need a simple and practical approach.

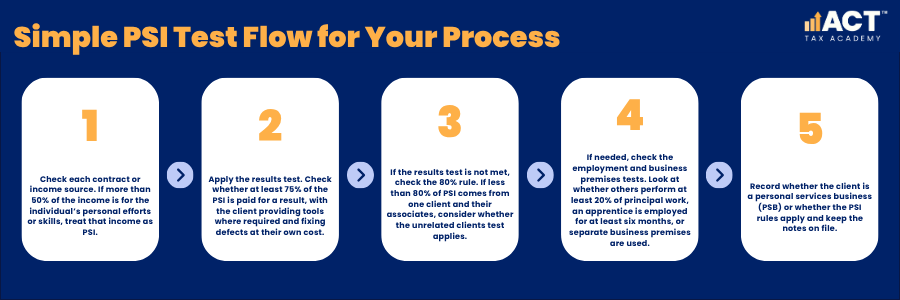

Under the personal services income rules, the first question is whether a taxpayer derives income that is mainly for their personal efforts or skills. If they earn PSI, the next step is to check whether the PSI rules apply or whether the client can self-assess as a personal services business. A client can generally self-assess as a PSB if they meet the results test for at least 75% of their PSI, or if they meet one of the other PSB tests and less than 80% of their PSI comes from the same client and that client’s associates.

What Makes PSI Rules Such a Big Risk for Firms?

PSI rules are a risk because they can change how clients pay tax and what they can claim as deductions. Where PSI rules apply, income may need to be taxed to the individual even if it was invoiced through a company, trust or other personal services entity. If the rules are not handled correctly, clients can lose a tax benefit they were expecting and may face amended assessments, interest and penalties.

Personal services income can arise across a wide range of services, from consulting to trades, professional work and contracting in small business. This can make it easy for PSI to slip through the cracks if your workflow relies on memory rather than clear questions. Mapping how PSI rules work into your systems helps your team spot PSI income early and deal with it in a calm, step‑by‑step way.

How Should PSI Filters Be Built Into Client Onboarding?

Your PSI workflow should start at client onboarding, when you first learn how the client earns income and how their business is structured. Intake forms for individuals, sole trader clients and those using a company or trust to provide services should all include questions about personal services income. The aim is to test the individual’s PSI position early and flag whether further guidance or professional advice is required.

At this stage, you want to know whether income generated is linked mainly to personal efforts, whether 80% or more of the PSI comes from one client and that client’s associates, and how the client’s business structure supports their work. You can then decide whether to note PSI as a medium or high risk and whether your engagement letter should reference PSI income and related tax obligations. Gathering this information early also makes it easier to explain why some clients may need to report PSI or claim certain deductions differently.

Why Does Your Engagement and Structuring Advice Need PSI Built In?

Once you have gathered basic PSI information, it should shape your engagement and business structure advice. A personal services entity, such as a company or trust, does not automatically change how PSI rules work, especially where income splitting is the main goal. Clients need to understand that if personal services income (PSI) is present and the PSI rules apply, the income may still be taxed to them personally.

Your role is to explain in plain language how PSI affects their tax return, including what income is treated as PSI income and when certain deductions may be limited. Where there is a realistic path to becoming a PSB, you can help them understand which PSB tests may apply and what genuine operational or contractual changes may be needed. Any changes should reflect the actual working arrangements, not just the wording of invoices or contracts. Where personal services income rules clearly apply, your advice should focus on setting expectations and keeping the client informed, rather than promising a tax benefit that may not be allowed.

How Do You Map PSI Tests into Everyday Workflow Steps?

The Australian Taxation Office asks taxpayers to self-assess whether they have PSI and whether the PSB tests are met. You can reflect this approach by building the PSI tests into your workflow in a sequence your team uses every time. This makes it easier to explain to clients how the rules work, without slipping into heavy jargon.

First, your team should check whether the income is mainly from personal efforts or skills, rather than an income producing asset or standard business model. If the client earns PSI, you then move through the results test, unrelated clients test, employment test and business premises test. At each stage, you note the outcome and whether further information or a personal services business determination may be needed.

Where Does Documentation and Evidence Sit in a PSI‑Aware Workflow?

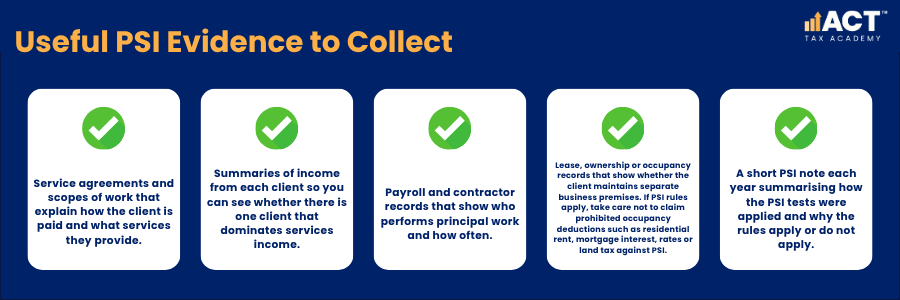

Your PSI mapping is only effective if it is supported by evidence that shows how the PSI tests were applied. At each stage, you should identify documents that show how income is generated, how many clients there are and what the contractual relationships look like. Good records also help you demonstrate that any tax benefit claimed was based on real facts and not just assumptions.

Copies of contracts help show whether the client is paid for a result, the work performed and who is responsible for defects. Schedules of income received from each client support the unrelated clients test and the “one client” questions for each income year. Records of staff, one or more apprentices and the business premises arrangement are important for the employment test and business premises test.

How Should PSI Rules Shape Your Mid‑Year and Pre‑Year‑End Reviews?

As the income year progresses, PSI positions can change, especially where clients move between different types of work or new contracts. Mid‑year and pre‑year‑end reviews give you a chance to re‑check the PSI tests and adjust your guidance where needed. This means you are not waiting until tax return time to discover that a client now earns PSI from only one client, or that broader compliance processes such as Single Touch Payroll (STP) reporting and reconciliation also need attention.

During these reviews, you can revisit whether income is still mainly from personal efforts or whether more income producing assets or staff now contribute to the income. You can also re‑run a short version of the PSI tests to confirm whether the results test or other PSB tests still fit the client’s situation. This allows you to suggest practical changes, seek further guidance or, where the client cannot self-assess as a PSB, consider whether a PSB determination may be available due to unusual circumstances, and to flag other ATO risks such as STP non‑compliance penalties that might affect the client’s overall position.

How Do PSI Rules Affect Year‑End Tax Return Preparation?

By year‑end, a PSI‑aware workflow should give you a clear view of which clients earn PSI and whether they are a personal services business or subject to PSI rules. This makes it easier to complete the income tax return and report PSI correctly. It also helps you explain why some clients can claim deductions in the usual way, while others face certain deductions being limited.

Your team needs to be comfortable using the PSI items in your software and any PSI decision tool you rely on to support self-assessment, while keeping file notes that explain the final position. For clients where PSI rules apply, you may need to attribute PSI to the individual who performed the work and review deductions carefully. Certain deductions cannot be claimed against PSI, including residential rent, mortgage interest, rates and land tax, payments to associates for non-principal work, and super contributions for associates for non-principal work. Clear notes on how you report PSI and which rules apply will support consistent handling and make reviews smoother.

How Can Your Firm Train and Support Staff on PSI‑Aware Workflows?

To make PSI part of everyday work, your team needs training that links the rules to real client examples. Short sessions can walk through how PSI income arises, how the PSI tests operate and how to use tools like a PSI decision tool to test the individual’s PSI position. This makes it easier for staff to talk about PSI without hiding behind technical language.

You can support this training with checklists inside your onboarding forms, review templates and year‑end workpapers so PSI checks happen at the same points for every client. From there, regular file reviews help confirm that PSI notes are complete and that staff understand when to seek professional advice from a senior team member. Over time, this builds confidence and helps your firm deliver consistent, practical guidance on personal services income and related tax obligations.

Conclusion

When you map PSI rules into your firm’s workflow, you turn a complex area into a simple, repeatable series of steps from onboarding to final tax return. By asking about personal efforts, clients, contracts and business premises early, you can self-assess PSI calmly rather than rushing at the end of the income year. This structured approach helps you explain outcomes in clear language and reduces the chance of surprises for clients.

If you support contractors, sole trader clients or small business owners who provide services, now is a good time to review how you handle PSI. Start by adding PSI questions to your onboarding, building short PSI notes into your files and using tools that support self-assessment and reporting. With clear processes, your team can handle personal services income with confidence and give clients practical, reassuring guidance on how the rules work for their business.