Building a PSI Checklist for Bookkeeping Staff: Questions to Ask Before Coding Income and Expenses

Building a PSI checklist for bookkeeping staff: questions to ask before coding income and expenses is one of the simplest ways to keep Personal Services Income (PSI) tidy and avoid headaches later. It helps your team spot where PSI rules might apply before they code income or expenses, instead of trying to fix everything at tax return time. This is especially important for sole trader and small business clients where most of the income received comes from one person’s personal efforts or skills.

What Is Personal Services Income and Why Does It Matter for Bookkeepers?

Personal Services Income (PSI) is income produced mainly from an individual’s personal efforts or skills, rather than from an income producing asset, large team or extensive systems. When most of the income from a contract is really a reward for one person’s work, it is likely to be Personal Services Income (PSI). This is different from income that flows mainly from equipment, stock, or intellectual property that is separate from the worker.

If the PSI rules apply, special tax rules can limit deductions and change how personal income is reported in the income tax return. In many cases, the entity that earns the income must report PSI for the test individual’s PSI, and some tax deductions may be treated like those of an employee. When bookkeepers understand this, they can code transactions and keep notes in a way that supports accurate records and helps the accountant review the PSI position.

How Should Your PSI Checklist Support Key ATO Tests?

The ATO uses the results test, unrelated clients test, employment test and business premises test to work out whether a taxpayer can self-assess as a Personal Services Business (PSB). The 80% rule is also critical, because unless the results test is met, a taxpayer generally cannot self-assess using the other PSB tests if 80% or more of the PSI comes from the same client and its associates. Bookkeepers should not make the tax determination, but they can record the facts the accountant or registered tax adviser needs to help the client self-assess under the ATO rules, which is especially important where clients may be subject to monthly BAS obligations for non-compliant businesses.

A good checklist prompts staff to collect details that show whether the income received comes from one client or from unrelated clients, and whether the person is truly paid for a result. This helps the accountant decide if the client can be treated as a Personal Services Business (PSB) or if special tax rules will limit certain deductions. When the underlying facts are captured well, your team can back up the position taken in the income tax and company records.

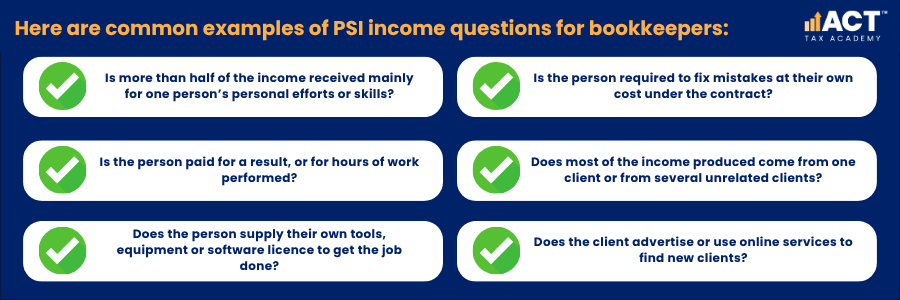

What Income Questions Should Bookkeepers Ask Before Coding Sales?

Before coding any sales, ask whether the income generated is mainly for work performed by one person’s skills or whether it relies more on equipment, staff or systems. If more than 50% of the income under a contract is a reward for an individual’s personal efforts or skills, the ATO generally treats all of the income from that contract as PSI. That simple question sets the tone for how carefully the rest of the transaction should be handled.

Next, ask whether the client is paid for a specific result or just for time spent. That may point toward the results test, but the ATO requires more. For at least 75% of the PSI, the worker must be paid to produce a result, provide the tools or equipment where required, and be liable for fixing defects at their own cost. Your team can reflect this in coding by clearly noting if a job is fixed-fee or hour-based and by linking invoices to the relevant job or project.

What Client and Contract Details Need To Be Captured for PSI?

The PSI rules look closely at how many clients a person has and whether the income mainly comes from one source. Bookkeepers should record which client is the real end user of the services, even if there is an agency in the middle. This helps later when checking if most income produced comes from one client or their associates.

Your checklist should prompt staff to confirm whether work was obtained from unrelated clients as a direct result of making offers to the public, such as advertising, maintaining a website, or tendering. Simply registering with an agency is not enough on its own. Where possible, attach the contract or engagement terms to the contact record so the tax team can later review how the services are provided. Clear links between income, clients, and agreements help show whether the unrelated clients test or other tests may be met and also support accurate reporting on forms such as the Instalment Activity Statement (IAS).

How Can Bookkeepers Help Evidence the Results Test?

The results test focuses on whether the worker is paid to provide services that deliver a set outcome, rather than just being paid like an employee. To satisfy the ATO results test, the worker must be paid for a result, provide the required tools or equipment where applicable, and be liable for rectifying defects at their own cost. Bookkeepers can support this by reflecting these features in the way they code transactions.

For example, they can set up separate income accounts for fixed-fee jobs and milestone-based work, and label invoice descriptions around results rather than hours. They can also link wages, contractor payments, software licence costs and other expenses to the job where the worker bears risk. Over time, this pattern of coding creates a clear picture that the worker is meeting the results test rather than just selling time and also supports accurate figures when lodging BAS for a business owner.

What Expense Questions Belong on a PSI Checklist?

When the PSI rules apply, deductions are generally limited to those that would be available to an employee, and some items are specifically denied, such as rent, mortgage interest, rates or land tax for a home, and payments to associates for non-principal work. Bookkeepers should ask if an expense is directly tied to earning PSI, or if it relates to a broader business setup. This matters because some deductions can be treated more like those of an employee when the rules apply, and understanding what can be claimed as a tax deduction helps frame those questions.

Your checklist might first ask whether the expense is clearly linked to the services being delivered, such as advertising, professional registration, account keeping fees or bank fees. It should also ask whether the payment is to an employee, contractor, or associate, because payments to associates for non-principal work are generally not deductible when the PSI rules apply. For larger items such as home occupancy costs, vehicles and equipment, bookkeepers can add a simple ‘PSI review’ note so the accountant can check whether ordinary deduction rules, PSI limits, or depreciation rules affect the claim.

How Do You Design Practical PSI Questions for Bookkeeping Staff?

To keep things simple, write each checklist prompt as an easy question that can be answered quickly while coding. For example: “Is this income mainly from one person’s personal efforts?”, “Does this contract pay for a result or for hours?”, or “Is this expense closely tied to income produced from personal services?”. Short, clear questions are easier for staff to use every day.

You can group these prompts under headings like Income Character, Client Spread, Contract Features, and Expense Flags. Under each heading, add three to five questions that help the bookkeeper decide if they should note “PSI risk” or request professional advice from the tax team. The goal is to support consistent decisions without overwhelming staff with long explanations.

What Might a Sample PSI Checklist for Income Look Like?

A simple PSI income checklist can be used whenever you take on a new client in almost any industry where services are the main offering. It can also be revisited each income year if the pattern of income received changes. This helps you review unusual circumstances early, rather than waiting until the income tax work has started and ensures the client is better prepared with a business tax return documents checklist.

What Might a Sample PSI Checklist for Expenses Look Like?

Your PSI expense checklist should help bookkeepers decide whether to flag an item for later review, rather than stop them from coding it. The questions should focus on whether the expense is directly linked to earning PSI and whether the worker is more like an employee or a personal services business. This keeps the focus on the link between cost and income.

Here are sample expense questions:

- Is this expense directly related to income generated from personal services (for example, advertising or listing fees)?

- Is the payment to a worker who assists with principal work and is paid on an arm’s length basis?

- Is this an overhead such as rent or vehicle running costs that might be treated differently if PSI rules apply?

- Is this a regular account keeping fee or bank fee linked to the account where PSI income is received?

- Should this expense be tagged for further guidance from the tax team before we claim deductions in the income tax return?

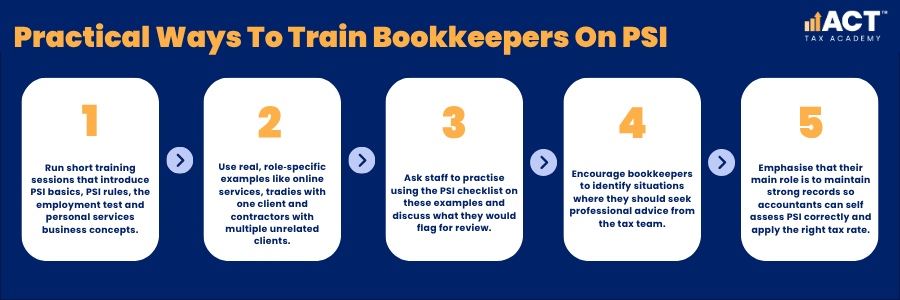

How Should You Train and Support Bookkeepers on PSI?

Introducing a checklist works best when it comes with training and space for questions. Many bookkeepers are comfortable with day-to-day coding but less familiar with PSI rules, employment test, or the idea of a personal services business. A short, practical session using real scenarios can build confidence without using heavy tax terms.

You might walk through examples of income produced from online services, tradies working for one client, and contractors with several unrelated clients. Ask staff to apply the checklist and talk through what they would flag for review or where they would seek professional advice. Reinforce that their role is to support good records so the accountant can self-assess correctly and help clients pay the right tax rate on their taxable income, building on basic bookkeeping foundations for small businesses.

How Can a PSI Checklist Reduce Risk and Support Better Outcomes?

A consistent PSI process shows that your practice takes tax and rules seriously without overcomplicating things for clients. When bookkeepers use the checklist, they create a trail of notes, tags and clear coding that supports the tax return position if questions arise. This becomes especially helpful where a PSB position or other decision has been taken in past years.

Capturing facts about clients, income, and expenses while jobs are fresh also helps the tax team review whether the client is a personal services business or simply has PSI income with limited deductions. In unusual circumstances where the pattern of income received changes, the checklist can prompt early conversations about how to report PSI. That means fewer surprises for clients and a smoother path to meeting their tax obligations.

Where Can You Find Tools and Guidance to Keep Your PSI Checklist Current?

The Australian Taxation Office provides detailed guidance on personal services income rules, along with examples and explanations that are written for small business and sole trader clients. Its online PSI decision tool can help you and your clients work through whether special tax rules may apply. You can refer staff to this tool for background while keeping your internal checklist short and practical, much like using a BAS lodgement checklist to systemise compliance tasks.

Professional bodies, tax educators and software providers also share examples and checklists on handling PSI across different industries. These resources can help you refine your own prompts about income received, services provided, and the deductions you can claim while avoiding common BAS lodgement mistakes that affect compliance. Refreshing your checklist occasionally ensures it reflects current thinking and gives your team confidence when they code and claim items that affect income tax.

Key Takeaways

A focused PSI checklist for bookkeeping staff turns complex personal services income concepts into simple questions about income, services and expenses. By thinking about personal efforts, one client versus unrelated clients, and key tests like the results test, your team can support accurate PSI reporting decisions. With good records, you can protect clients, reduce risk, and give clearer professional advice around tax, deductions, and the real impact of PSI rules on their taxable income.