Calculating Your Medicare Levy: A Step-by-Step Guide for Australian Small Business Owners

Calculating Your Medicare Levy: A Step-By-Step Guide for Australian Small Business Owners starts with knowing that the Medicare levy is 2% of your taxable income for most Australian taxpayers. This Medicare levy helps fund Australia’s public health system and is paid in addition to your normal income tax. As a small business owner, knowing how much Medicare levy you pay each financial year can make tax time far less stressful and easier to plan for.

Most Australian taxpayers also want to know how much tax they will pay overall when they lodge their income tax return. If you run a business, your income can move around, which means your levy, Medicare levy surcharge and income tax can change from year to year. When you understand how the levy is calculated, how income thresholds work and when you may have to pay the Medicare levy surcharge, you can make better choices about cash flow and private health insurance.

What Is the Medicare Levy for Australian Small Business Owners?

The Medicare levy is a charge most Australian taxpayers need to pay to support Medicare and the wider public system. In simple terms, the standard rate is 2 per cent of your taxable income if you are a resident for tax purposes and your income is above the relevant income thresholds.

If you are a sole trader, partner in a partnership or receive wages from your own company, the levy is calculated on your personal taxable income in your individual income tax return. It is not calculated on business profits retained inside a company or trust, but on what flows to you personally as taxable income, such as salary or wages, trust or partnership distributions, dividends and other assessable income.

- Some people qualify for a Medicare levy exemption or partial exemption based on personal circumstances.

- The levy applies to a single person, de facto couples and families where income is above a certain amount.

- Most Australian taxpayers who are residents and not exempt will pay the Medicare levy in the same way as other tax.

Why Does the Medicare Levy Matter So Much for Small Business Cash Flow?

The Medicare levy matters because it directly reduces how much income you keep after tax. If you underestimate how much Medicare levy you pay, your final tax bill at tax time can be higher than expected, especially in a strong business year.

As a small business owner, you might have business income, wages, and investment income all counted together. Your employer withholds tax from wages, and PAYG instalments may be taken from business income, but if these amounts are too low you will still need to pay the levy and possibly the Medicare levy surcharge when your income tax return is processed.

How Do You Work Out Your Taxable Income For Medicare Levy Purposes?

To work out how much Medicare levy you pay, you first need your taxable income. This starts with all income that is assessable, including business profits, wages, interest, dividends and rental income, and then subtracting allowable deductions.

For small business owners, taxable income can include salary from your own company, income from other employment, and net business profit if you operate as a sole trader. Once you have one figure for taxable income, that amount is used to calculate the levy and to check your position against the income thresholds.

Typical items that feed into taxable income:

- Net business income from your sole trader or partnership activities.

- Wages, interest, dividends, rent and certain capital gains.

- Less tax deductions such as business expenses, some super contributions and other eligible costs.

What Is the Key Medicare Levy Low-Income Thresholds?

The Medicare levy includes low-income thresholds so that people on lower incomes pay less or no levy. If your taxable income is below a certain amount, you may not need to pay the levy at all for that financial year.

There are different income thresholds for a single person, couples and families, and they also change when you are eligible for the seniors and pensioners tax offset. Families and de facto couples have combined income thresholds, which are increased for each dependent child or student. These thresholds are updated regularly, so it is important to check the current figures for the relevant financial year.

How Does the Shade-In (Reduced) Medicare Levy Work?

If you earn just above the low-income threshold, you do not jump straight into paying the full 2 per cent levy. Instead, there is a shade-in range where you pay a smaller amount that gradually increases as your income rises.

In this range, the levy is generally calculated at 10 cents for every dollar your income sits above the lower threshold, until the full 2 per cent rate applies. This keeps the change smooth so that a small increase in income does not cause a sudden large increase in the levy.

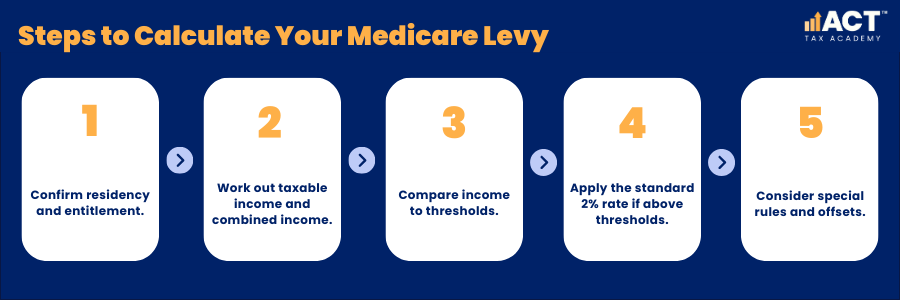

What Is the Step-By-Step Process to Calculate Your Medicare Levy?

You can break down the Medicare levy calculation into a simple step-by-step process. This makes it easier to estimate how much Medicare levy you pay before you lodge your tax return.

Step 1 – Confirm residency and entitlement

Check whether you are a resident for tax purposes and whether you are entitled to Medicare for the full year. If you are a foreign resident for part of the year, or you are not entitled to Medicare benefits for some or all of the year, you may be fully exempt or eligible for a partial exemption for those days.

Step 2 – Work out taxable income and combined income

Use your draft income tax return figures to find your taxable income. If you have a spouse, you will also need your spouse’s income because family thresholds and some calculations use combined income.

Step 3 – Compare income to thresholds

Compare your taxable income, or family combined income, to the relevant single or family income threshold for the current financial year. This will show whether you are exempt, pay a reduced levy or need to pay the full 2 per cent levy.

Step 4 – Apply the standard 2 per cent rate if above thresholds

If your income is above the upper threshold, multiply your taxable income by 2 per cent to find your levy. This amount is then added to your income tax in your final assessment.

Step 5 – Consider special rules and offsets

Review whether you qualify for a Medicare levy exemption, partial exemption or a higher threshold due to the pensioners tax offset or similar offsets. These rules depend on personal circumstances, age and other eligibility tests.

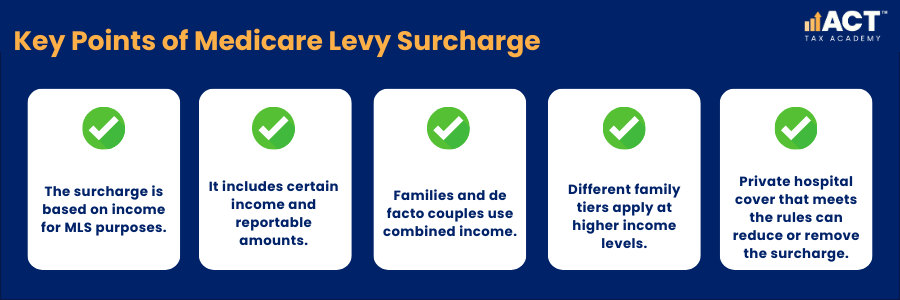

How Does the Medicare Levy Surcharge Interact with Small Business Income?

The Medicare levy surcharge is a separate charge that may apply if you and your family do not hold hospital cover at an appropriate level and your income is above the MLS income threshold. The surcharge is designed to encourage individuals and families to take out private hospital cover instead of relying only on the public system.

For surcharge purposes, there are family tiers and single tiers that use income for MLS purposes, which may be different from normal taxable income. If your income is over the relevant MLS income threshold and you do not hold eligible hospital cover with a registered health insurer, you will generally have to pay the Medicare Levy Surcharge (MLS) in addition to the standard levy.

How Do Private Health Insurance and Hospital Cover Affect What You Pay?

Private health insurance, and in particular private patient hospital cover, plays a key role in whether you need to pay the Medicare levy surcharge. If you hold hospital cover with a registered health insurer that meets the required standard, you can often avoid paying the surcharge even when your income is above the threshold.

Your private health insurance policy or private health cover may also give access to the private health insurance rebate, which reduces the premium you pay. This does not reduce the Medicare levy itself but can change your overall health insurance costs and help balance the decision to pay the MLS or take out private hospital insurance.

What Practical Strategies Help Small Business Owners Manage Levy and Surcharge?

For small business owners, a good strategy is to plan for the levy and surcharge at the same time as normal income tax. This means checking how much tax and levy you are likely to pay before the end of the financial year and making adjustments where possible.

You can look at the timing of income, such as large invoices or one-off gains, and how they affect your income thresholds. You can also check whether it makes sense to hold hospital cover, change your private health insurance policy or adjust the way you pay yourself from your business so that your income for MLS purposes stays within a certain band, within the rules.mple systems so that the required information flows smoothly into your calculations each week or month. This means your weekly estimate keeps pace with changes in your pay, business income, or family circumstances.

How Can Guidance from a Local Adviser Make This Easier?

Even though the main Medicare rules are consistent, every small business owner has different personal circumstances. Factors such as whether you are single, in a couple, have a dependent child, are eligible for an offset, or are exempt for part of the year will all affect what you need to pay.

A local adviser who understands small business, personal tax and Medicare can help you interpret the rules in a straightforward way. They can walk through your income, combined income if you have a spouse, and any exemptions to show exactly how the levy and Medicare levy surcharge are calculated for you.

When you work with a professional who follows guidance from the Australian Taxation Office and stays up to date with changes, you get clear answers instead of guesswork. That support can help you plan, avoid paying more than you need to pay, and feel confident that your tax, levy and health cover decisions are aligned with your goals.