Understanding Business Growth: When to Reassess Your Sole Trader vs Company Status in 2025

Understanding your sole trader vs company status becomes essential as your business grows, yet many Australian business owners miss the critical moment to make the switch. Growth sneaks up quietly, and the simplest business structure that worked beautifully at startup can suddenly become a liability holding you back. We want to help you recognise the right time to reassess your business structure so you can protect what you’ve built and position yourself for success.

Key Differences of Company vs Sole Trader

The most fundamental difference lies in how your business operates in the eyes of the law and the ATO. A sole trader business structure means you and your business are legally one and the same, with no separation between personal and business assets. When you operate as a sole trader, all your business income flows into your personal tax return, and you’re personally liable for every business debt and obligation your business incurs.

In contrast, a company structure creates a separate legal entity with its own Australian Business Number (ABN) and Australian Company Number (ACN). Your company exists independently of you, meaning the business can own separate business assets and incur company debts in its own name. This separation is crucial—it means your personal assets and business assets remain distinct, offering you crucial protection that sole traders simply don’t have.

How Much Personal Risk Do You Face as a Sole Trader?

When you operate as a sole trader, you face unlimited personal liability for all business debts and financial or tax debts your business creates. If a customer sues your business, if suppliers remain unpaid, or if tax debts accumulate, your home, savings, and personal assets can be used to settle those debts. This unlimited personal liability means a single significant business problem could threaten your personal financial security and everything you’ve worked to build.

The reality hits hardest when you’re personally responsible for situations completely beyond your control—a client dispute, a missed payment from another business, or unexpectedly complex tax obligations. As your business grows and takes on more clients, larger contracts, and more complex operations, the potential financial exposure grows with it. Many business owners don’t realise how vulnerable they are until something goes wrong, at which point protection becomes impossible.

Common scenarios where personal liability becomes critical:

- A major contract fails and leaves you with significant financial obligations

- A customer suffers loss or injury and sues for compensation

- Your business cannot cover its operating expenses and owes suppliers significant amounts

- The ATO identifies tax debts or compliance issues requiring immediate payment

- Business partners or employees cause financial or legal harm the business must address

- Your business requires workers compensation insurance, but the claim exceeds coverage

When Does Your Business Income Trigger a Structure Reassessment?

Many business owners use a revenue threshold to guide their decision, and there’s solid reasoning behind this. Once your business income consistently exceeds roughly $120,000 annually, the tax differences between operating as a sole trader and establishing a company structure become impossible to ignore. At this income level, the tax you pay can differ by thousands of dollars depending on your structure.

As a sole trader, you pay personal income tax rates on all your business income, which can climb to 37% plus the 2% Medicare Levy at higher income levels. A company structure allows you to pay a flatter corporate tax rate of 25%, creating a substantial tax saving that grows larger with every dollar of additional business income you earn. The maths becomes increasingly compelling as your profits climb, making structure reassessment a genuine financial priority rather than just a “nice to have” consideration.

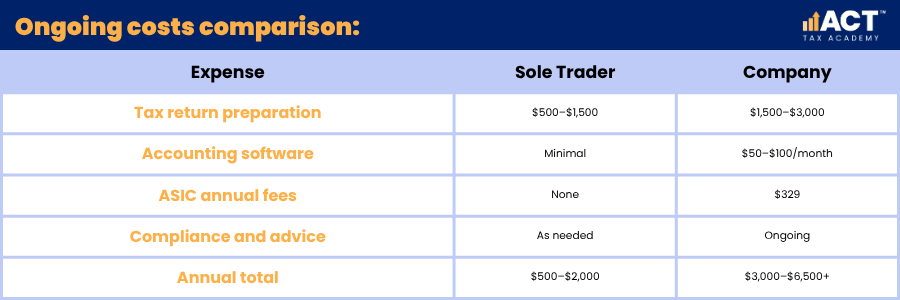

What Ongoing Costs Come With Each Structure?

Sole traders enjoy a significant advantage in simplicity and cost—your ongoing costs remain minimal because you file a personal tax return and handle relatively straightforward administration. Most sole traders work with an accountant or business advisor during tax time, and that’s often the extent of their professional costs beyond their accountant’s annual fee. Your separate business bank account requires standard banking fees, but nothing complex or unusual.

Companies face substantially higher ongoing costs because they must lodge an annual company tax return, maintain detailed financial records, and pay annual compliance fees to regulatory bodies. You’ll need to pay ASIC an annual review fee to keep your company registration current, invest in more sophisticated accounting software or services, and ensure proper tax reporting and tax advice throughout the year. Many business owners find they spend $3,000 to $6,000 annually on accounting and compliance services just to keep a company running smoothly.

How Does Liability Protection Shape Your Decision?

Limited liability stands as perhaps the most compelling reason to transition from a sole trader business to a company structure. When you operate as a company, your liability is limited to the amount you’ve invested in the business. If something goes catastrophically wrong, your shareholders’ liability is limited—protecting personal assets from being seized to cover company debts.

This protection becomes increasingly valuable as your business grows and takes on more exposure through larger contracts, more employees, and greater financial obligations. Professional indemnity insurance and public liability insurance become easier to secure when you operate through a company structure, as many insurers view companies as lower-risk clients. Combined with limited liability protection, these insurance options create multiple layers of protection that sole traders simply cannot achieve.

Transition From Sole Trader to Company Business Structure

The transition process begins with company registration through the appropriate regulatory body, which typically takes just days and involves a one-time registration fee. You’ll establish your company structure with a proper Australian Company Number and apply for a new Australian Business Number for the company. Opening a separate business bank account for the company allows you to keep company finances distinct from your personal finances from day one.

An accountant or business advisor becomes invaluable during this transition because they help you transfer your existing business assets into the company in a tax-efficient way. The ATO provides rollover relief for certain business asset transfers, which means you can move business assets into your new company structure without triggering immediate tax consequences if you meet specific eligibility requirements. Proper planning during this phase prevents costly mistakes and ensures you take full advantage of available concessions.

What Tax and Superannuation Obligations Come With Company Operation?

Operating through a company structure fundamentally changes your tax reporting requirements and obligations. You’ll file a separate business tax return that reports your company’s income, expenses, and tax position independently. If your company pays dividends to shareholders or pays wages to director-employees, managing these distributions requires careful attention to tax rules and proper documentation.

Company directors face mandatory superannuation obligations if they employ themselves as employees—they must contribute at least 12% of wages to superannuation for themselves just like any employee. This differs from sole traders, who have discretionary superannuation contributions. Additionally, company structures involve more complex tax planning opportunities around income splitting, dividend timing, and profit retention, but these opportunities require proper tax advice to understand correctly.

Conclusion

The right time to reassess your business structure is now if your business income suggests a change would benefit you, or if you’re heading towards that threshold. Sole traders and companies are subject to different tax obligations: for instance, the company tax rate may be more favourable as profits grow, compared to personal income tax rates for sole traders.

Schedule a conversation with an accountant or business advisor who can model your specific situation and show you exactly what each structure would cost you in taxes and ongoing expenses. Your business structure isn’t a permanent decision—it’s a tool that should evolve as your business grows. What worked perfectly as a sole trader when you started might hold you back once your business reaches genuine scale.