Salary Sacrifice vs. Fringe Benefits: Key Differences and Tax Implications for Australian Businesses

Salary Sacrifice Vs Fringe Benefits: Key Differences and Tax Implications for Australian Businesses matter because the way you structure benefits can change how much tax you, and your employees, pay. When you understand how salary sacrifice, Fringe Benefits Tax (FBT) and exempt benefits work together, you can design total remuneration packaging that supports your team without creating hidden costs. Done well, these strategies turn part of your salary into practical support, instead of extra tax.

What Is Salary Sacrifice and How Does It Work?

Salary sacrifice is a formal agreement where an employee agrees to give up part of future pre-tax salary or wages in return for non-cash benefits of similar value. Instead of taking that amount as cash, the employee receives benefits such as salary sacrificed super contributions, a portable electronic device, or even help with loan repayments. Because the employee receives reduced salary, their assessable income and taxable income are lower, so they may pay less income tax on their wages.

For an effective salary sacrifice arrangement, the employee agrees to the reduced salary before the work is performed and the terms are usually recorded in an employment or industrial agreement or a separate letter. The sacrificed salary must genuinely be replaced by benefits provided by the employer, and the employee cannot redirect that income back to themselves as cash later. If these conditions are not met, the ATO can treat the sacrificed amount as normal income, meaning the employee will simply pay tax on the full salary and the benefits may still affect FBT.

How Does Fringe Benefits Tax Work for Employers?

Fringe Benefits Tax is a separate tax that an employer pays when they provide certain non-cash benefits to employees or their associates in respect of employment. These fringe benefits can include a company car, health insurance, school fees, loan repayments, or other personal expenses paid by the employer. Instead of the employee paying income tax on these benefits, the employer may need to pay FBT based on the taxable value of the benefits.

To work out how much fringe benefits tax you must pay, you identify all benefits provided during the FBT year, calculate the taxable value for each, and add them up to a total taxable value. You then apply the relevant gross-up factor and FBT rate to this total to work out how much FBT the employer pays. The FBT rate for the 2025–26 FBT year is 47%, matching the top marginal income tax rate plus the Medicare levy. The Type 1 gross-up rate is 2.0802 for benefits with GST credits, and the Type 2 rate is 1.8868 for benefits without GST credits. While the employer can usually claim a tax deduction for both the cost of the benefits and the FBT itself, they still need to manage the cash flow and ensure FBT obligations are met on time.

Is Salary Sacrifice a Fringe Benefit for Tax Purposes?

A salary sacrifice arrangement is often the way a fringe benefit is funded rather than a different type of benefit. When an employee sacrifices salary for a benefit like a company car or school fees, the benefits provided are still fringe benefits for FBT purposes, even though the employee is on reduced salary. The employer may have to pay FBT on those benefits, while the employee enjoys less income tax on their remaining wages.

Some salary packaging options are not fringe benefits and do not trigger Fringe Benefits Tax. A key example is salary sacrificed super contributions paid to a complying super fund, which are treated as employer contributions rather than fringe benefits. Certain benefits can also be exempt benefits, such as specific types of portable electronic devices or protective clothing used mainly for work, so they do not increase FBT even though they form part of total remuneration packaging.

What Is the Difference Between Income Tax and Fringe Benefits Tax?

Income tax is paid by individuals on their assessable income, such as salary, wages, bonuses and other earnings from work and investments. When employees do not enter a salary packaging arrangement, they receive full salary and pay tax on their taxable income after any deductions and tax offsets. A salary sacrifice arrangement changes this by turning part of your salary into benefits, reducing assessable income and potentially leading to less income tax.

Fringe Benefits Tax, on the other hand, is a tax that employers pay when they provide certain benefits instead of, or in addition to, salary and wages. It is calculated on the taxable value of fringe benefits, not on the income of the employees. In many cases, however, high levels of benefits reported can still affect employees through a reportable fringe benefits amount on their income statement or payment summary, which may influence income-tested thresholds and government benefits even though they do not pay tax directly on that amount.

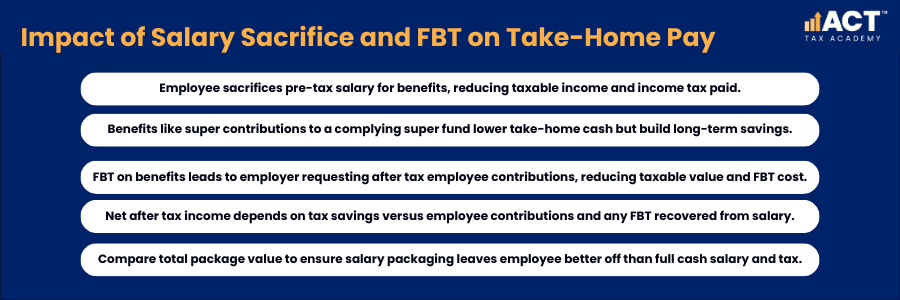

How Do Salary Sacrifice and FBT Affect Employee Take-Home Income?

When an employee uses a salary packaging arrangement, they swap pre-tax salary for benefits, which can result in less income tax and higher after-tax income in some situations. For example, sacrificing salary into super contributions paid to a complying super fund can reduce taxable income now and help build long-term savings, while still keeping the total remuneration packaging attractive. From 1 July 2025, the Super Guarantee rate is 12% of ordinary time earnings, completing the scheduled increases. Because the employer contributions go straight to the super fund, the employee may see less income in their bank account but more going towards future goals.

If the benefits attract FBT, the employer might increase the reduced salary, request employee contributions from after tax income, or adjust other parts of the package to keep overall cost under control. Employee contributions can lower the taxable value of benefits for FBT purposes, which reduces the FBT the employer pays, but they also reduce the employee’s after-tax income. The key question is whether the combination of reduced salary, benefits provided, any employee contributions and any FBT the employer pays leaves the employee in a better position than simply taking the cash and paying full tax.

Which Benefits Are Commonly Salary Packaged Or Treated As Fringe Benefits?

Popular salary packaging items include salary sacrificed super contributions, a company car under a novated lease, and work-related items such as a portable electronic device or protective clothing. These are often provided as part of total remuneration packaging so employees can tailor benefits to their needs. Some employers also allow salary packaging of health insurance, school fees, or loan repayments, although these typically have FBT implications unless a specific exemption applies.

Many of these benefits are fringe benefits for FBT purposes when provided in connection with employment, whether or not they are funded from sacrificed salary. Employer super contributions, including super guarantee contributions and additional contributions under a salary sacrifice arrangement, are treated differently and are generally not fringe benefits when paid to a complying super fund. This is why clearly defining which contributions are super guarantee contributions, which are extra employer contributions, and which are salary sacrifice contributions paid from reduced salary is so important.

How Should Employers Manage FBT Obligations and Reporting?

Employers need a clear process to identify all benefits provided to employees and associates throughout the FBT year and decide whether those benefits are taxable, exempt, or subject to concessions. For taxable benefits, you work out the taxable value, adjust for any employee contributions, and then calculate how much FBT you must pay. This ensures that FBT obligations are met without guesswork and that you do not accidentally pay Fringe Benefits Tax on exempt benefits.

You also need to manage reporting, especially where the total taxable value of certain fringe benefits for an employee exceeds $2,000 in an FBT year, the grossed-up amount (minimum $3,773) must be reported on their income statement. In that case, benefits reported appear as a reportable fringe benefits amount on the employee’s income statement. Accurate records of contributions paid to super, benefits provided, and any salary packaging arrangement help you support your position and make it easier to complete FBT calculations each year.

What Are Practical Examples of Salary Sacrifice Vs Fringe Benefits?

Imagine an employee earning a stable income who wants to boost retirement savings. They enter a salary sacrifice arrangement where part of their pre-tax salary is redirected into extra super contributions paid to a complying super fund. Their reduced salary means less income tax and less income reported as normal income, while the employer contributions to super are not fringe benefits and the employer may claim a tax deduction on the contributions. The concessional contributions cap for 2025–26 is $30,000, which includes employer super contributions, salary sacrificed super contributions, and any personal contributions claimed as a tax deduction.

In another example, an employee sacrifices salary for a company car that they use for both work and personal travel. The employee’s reduced salary means less income tax on wages, but the car and its associated costs are fringe benefits for FBT purposes, so the employer must calculate the taxable value and may need to pay FBT. To manage the cost, the employer might ask the employee to make after tax employee contributions, which reduce the taxable value and the FBT the employer pays, but also reduce the employee’s after-tax income.

These examples show why it is essential to look at income, tax, benefits and FBT together before setting up any arrangement. A considered approach weighs up whether you will pay FBT, how much less income tax your employees pay, and whether the benefits provided truly support your business goals. That way, salary sacrifice and fringe benefits become tools to help your team, not sources of surprise tax bills.

How Can You Use These Rules to Support Your Business?

Understanding the link between salary sacrifice, fringe benefits and income tax helps you design packages that attract and retain good people without wasting money. You can decide which benefits form part of your salary strategy, when to use total remuneration packaging, and where FBT cost is justified by the value of the benefits. Reviewing your current arrangements can also highlight where you might be paying FBT unnecessarily, or where employees could be better off with a different mix of salary and benefits.

If you are unsure whether your salary packaging arrangement or FBT processes are effective, it is worth getting tailored advice. A review can look at your benefits provided, contributions paid to super, total taxable value of benefits, and how benefits are reported to employees. With clear guidance, you can adjust packages, manage FBT obligations more confidently, and give your team benefits that genuinely work for them and for your business.