Salary Sacrifice and Superannuation: Tax-Effective Strategies for Small Businesses

Salary Sacrifice and Superannuation: Tax-Effective Strategies for Small Businesses can help you use pre-tax salary in a way that reduces taxable income and boosts super contributions at the same time. When a salary sacrifice arrangement is set up properly, part of an employee’s gross salary is redirected to their superannuation fund before they pay income tax. This means employees can often pay less income tax overall while you, as the employer, provide more valuable employee benefits without a big jump in total remuneration packaging.

As of 1 July 2025, the super guarantee rate is 12% and the concessional contributions cap is $30,000 per year, so understanding these limits is essential when designing salary sacrifice arrangements. Note that for 2025-26, the maximum super contribution base is $62,500 per quarter (or $250,000 per year), which means you only calculate SG on earnings up to this amount.

What Is Salary Sacrifice into Super for Small Businesses?

Salary sacrifice is an arrangement where an employee agrees to receive a reduced salary and have the sacrificed amount paid as extra employer contributions into their super fund. Instead of being paid as after-tax income, part of the before tax salary goes directly into the employee’s superannuation contributions account. This can lead to less tax on that portion of income, provided the concessional contributions cap is not exceeded.

Under a salary sacrifice agreement, the sacrificed salary is treated as super contributions from the employer, not as employee contributions. The key is that the employee agrees in writing before the income is earned, and the employer offers to pay the sacrificed amount into a complying super fund. This simple step turns personal expenses for future retirement into a structured, long‑term savings plan using pre-tax dollars.

How Does Salary Sacrifice and Superannuation Reduce Tax?

To understand how does salary sacrifice work in practice, compare tax on normal salary with tax on salary sacrificed super contributions. When income is paid as salary, the full amount is included in assessable income and you pay income tax based on your marginal tax rate. When part of that income is paid as super contributions, it can be taxed at a lower rate inside the fund, which usually means less income tax overall.

This difference between the marginal tax rate on tax salary and the rate that applies to concessional contributions is where the tax effective benefit arises. For many people on middle to high incomes, moving a portion of their before tax salary into super means they pay less tax and end up with more invested for retirement than if they had simply taken the same amount as home pay. The net result is less income in the hand today but often more wealth over the long term.

What ATO Rules Apply to Salary Sacrifice Arrangements?

The Australian Taxation Office expects any salary sacrifice arrangement to be genuine, written and agreed before the income is earned. This means you cannot decide after the end of a financial year to reclassify income as sacrificed salary. The arrangement must clearly show how much salary will be given up and how much will be paid as super contributions or other benefits.

A critical rule is that you must calculate super guarantee on the employee’s original gross salary, not the reduced salary after salary sacrifice. Salary sacrificed super contributions are extra and do not replace the minimum super you must pay. You also need to make sure that the superannuation fund receiving the contributions is a complying super fund so that concessional tax treatment is available.

How Do Contribution Caps, Concessional Contributions and High Incomes Interact?

All employer contributions, including salary sacrificed super contributions and normal super guarantee, count towards the concessional contributions cap. If total concessional contributions in a financial year go over this limit, the excess can be added back to your assessable income and taxed at normal rates. This can remove the tax advantage and may create extra tax to pay.

People earning over $250,000 (including their income plus concessional contributions) also face Division 293 tax, which adds an extra 15% tax on top of the standard 15% contributions tax. Some employees may also be able to use unused concessional cap amounts from a previous financial year, which can allow them to contribute more in a later year without breaking the cap. This can be a helpful planning tool, but it should be checked carefully before committing to a large, sacrificed amount.

What Are the Practical Benefits for Small Business Employers?

Offering salary sacrifice shows that your business takes employee benefits and long‑term financial wellbeing seriously. It allows you to provide more value without simply increasing gross salary, which can help with recruitment and retention. Staff often see a clear link between offering salary sacrifice and feeling respected and supported in their financial goals.

For you as the employer, salary sacrifice can be easier to manage than some other benefits because payments go straight to a super fund rather than being used for many different personal expenses. There is usually no need to pay fringe benefits tax on salary sacrificed super contributions to a complying super fund. This can make salary sacrifice into super a simpler, lower risk option compared with other benefits that may create a taxable value for fringe benefits tax.

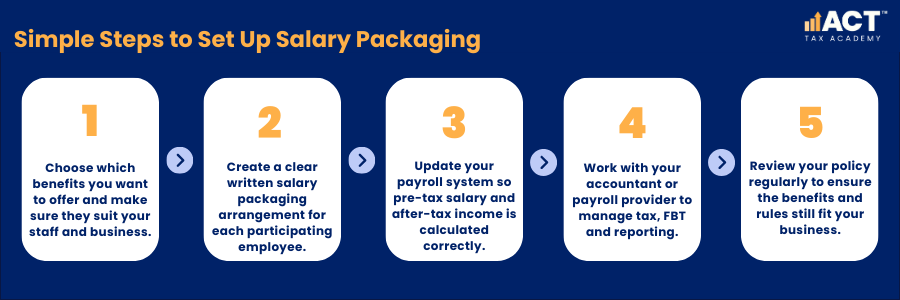

How Should Small Businesses Set Up Salary Sacrifice into Super?

When an employer offers salary sacrifice, the first step is to create a clear process and simple paperwork. This usually starts with a short salary sacrifice agreement or form where the employee agrees to a reduced salary and requests that a fixed dollar amount or percentage of pre tax salary be paid to a nominated super fund. The form should also explain that the arrangement will continue each financial year until changed in writing.

Your payroll system then needs to be set up so that the sacrificed amount is taken before tax is calculated. This means the sacrificed amount is removed from gross salary when working out income tax, but super guarantee must still be calculated on the original gross salary (including the amount sacrificed) and leave entitlements should typically be based on the pre-sacrifice salary unless your employment contracts specify otherwise. The sacrificed amount is then shown on payslips and in year‑end reports so employees can see how their reduced salary and super contributions interact.

What Salary Sacrifice and Superannuation Strategies Suit Different Employees?

Different strategies suit different income levels and personal situations, so it helps to match options to employee needs. For people on lower incomes, the benefit of paying less tax by using salary sacrifice may be smaller, and they might prioritise higher take home pay instead. For employees on higher marginal tax rates, using pre tax dollars for super contributions can create stronger tax savings.

Some employees prefer a simple percentage, such as 3–5% of their gross salary, while others choose a fixed figure each pay cycle. Staff who already manage school fees, childcare costs, loan repayments and other personal expenses may need to balance reduced salary against their current budget. This is where encouraging staff to seek professional advice can be helpful, so they can work out the right level of reduced salary without creating cash‑flow stress.

How Does Salary Packaging Compare with Other Benefits and Fringe Benefits Tax?

Salary packaging can include a range of benefits, such as novated lease arrangements, lease payments, certain benefits like work‑related devices and sometimes school fees or childcare costs, depending on the sector. Many of these benefits can create fringe benefits, which may require you to calculate a taxable value and possibly pay fringe benefits tax. In contrast, salary sacrificed super contributions to a complying super fund are usually exempt benefits for fringe benefits tax purposes.

If you pay fringe benefits tax on other benefits, this can reduce or remove the overall advantage of the arrangement. You also need to consider associated costs, such as administration fees or changes to leave entitlements when staff receive other benefits. For many small businesses, focusing first on salary sacrifice into super is a simpler way to offer tax effective benefits without needing to pay FBT or track complex personal benefits.

What Common Pitfalls Should Small Businesses Avoid?

One common pitfall is assuming salary sacrifice reduces the super guarantee you must pay. In reality, you still calculate SG on the employee’s original gross salary, even when there is a reduced salary being paid in cash. Another pitfall is not keeping track of total concessional contributions, which can lead to unplanned tax if contribution caps are exceeded.

A further risk arises when salary sacrifice is used for personal expenses like loan repayments, school fees or other personal expenses through broader salary packaging. In these cases, some or all of the benefits may not be exempt benefits and you may need to pay FBT, which can make the overall arrangement less tax effective. Poor record‑keeping, unclear communication and late payments to the super fund can also damage trust and create compliance issues.

How Can ACT Small Businesses Move Forward with Salary Sacrifice and Superannuation?

For ACT small businesses, offering salary sacrifice can be a simple way to add value to employees without huge changes to your payroll structure. Start by deciding which benefits to offer, with super contributions usually being the most straightforward and widely suitable. Then create standard documents and clear explanations so each employee understands how a reduced salary and sacrificed amount will affect their income, tax and home pay.

From there, you can gradually expand your approach if it suits your team, such as considering limited salary packaging for other benefits where it makes sense and does not create a need to pay FBT. The key is to keep the process transparent, track contribution caps and ensure all superannuation contributions are sent to the correct super fund on time. Taking this structured approach helps you manage tax implications, support your staff and keep your business on the right side of the rules.