Record-Keeping Tips for Trustees: Avoiding Costly Section 100A Mistakes

Record-keeping tips for trustees are essential for avoiding costly Section 100A mistakes that could expose your trust to significant tax penalties. When trustees fail to properly document trust distributions and beneficiary entitlements, they risk activating one of the Australian Taxation Office’s (ATO) most powerful anti-avoidance provisions. Section 100A of the Income Tax Assessment Act can see trustees taxed at the top marginal tax rate plus penalties and interest—making accurate record-keeping not only a compliance requirement but also a way to protect your trust from unnecessary financial loss.

Understanding Section 100A and Its Risks

Section 100A targets arrangements where a beneficiary becomes presently entitled to trust income, but another party—such as a parent, company, or different beneficiary—receives the actual benefit. This is what the ATO refers to as a reimbursement agreement.

The rule was designed to prevent situations where beneficiaries are used to achieve significantly less tax while the funds are retained or enjoyed by someone else.

Why the ATO Cares About Section 100A

The ATO has devoted strong compliance resources to identifying trust arrangements that do not align with ordinary family or commercial dealings. Ordinary dealings refer to genuine, arm’s-length family and business transactions—such as parents supporting children or reinvesting income for business growth.

When distribution arrangements fall outside these norms, the ATO may treat the income as if the trustee, not the beneficiary, received it. This means the trustee pays income tax at the top marginal tax rate.

When Section 100A Applies

Section 100A most often applies when:

- A beneficiary is made presently entitled to trust income but does not receive or control it.

- A different person benefits economically from the trust distribution.

- The arrangement cannot be shown to arise from family or commercial objectives supported by documentation.

Simply put, documentation must prove that every trust distribution is genuine—either part of ordinary family or commercial dealings, or supported by clear evidence that the beneficiary received the funds.

Legal and Financial Consequences

If the ATO decides Section 100A applies, the affected trust income becomes part of the trustee’s assessable income and is taxed at the top marginal tax rate. Penalties may range from 25% to 75% of the tax shortfall, plus interest.

To avoid this, good record-keeping and well-documented trustee resolutions are your strongest defence.

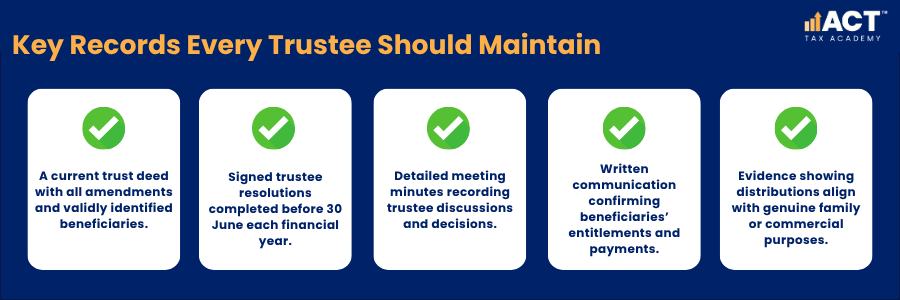

Essential Documents Every Trustee Should Keep

Keeping the right documents ensures your trust can establish the validity of its decisions and support its distributions during an ATO review.

Trust Deed and Amendments

It’s vital to review your trust deed regularly to ensure it’s up to date with any amendments, that all beneficiaries are validly identified, and that you fully understand how income and capital gains should be distributed. When trustees fail to follow the terms of their deed, distributions can breach the Income Tax Assessment Act and may be deemed invalid.

Trustee Resolutions and Minutes

Trustee resolutions record the formal decisions made about how trust income will be distributed. These resolutions must be prepared and signed before 30 June each financial year. To remain compliant, clearly state which beneficiaries are to receive distributions and the specific proportion or amount allocated to each. Avoid vague or last-minute resolutions, and keep detailed meeting minutes that record discussions, the reasoning behind decisions, and timing.

Beneficiary Communications

Trustees must also maintain evidence showing that beneficiaries were informed of their entitlements. The ATO views it negatively when beneficiaries are unaware of their rights or have not received their share. Keep copies of all distribution letters or emails, acknowledgements of receipt, and payment confirmations such as bank transfers or cheque records. For family group beneficiaries, ensure documentation shows how received funds were used to support family or household financial obligations, reinforcing that distributions were genuine and properly executed.

Clear Records for Financial Transactions

Financial documentation must support the trust’s income, expense, and distribution records. Maintaining accurate evidence is essential to show all activity aligns with reasonable commercial dealing circumstances.

Financial and Accounting Records

It’s important to maintain detailed and complete records such as bank statements, receipts, invoices, and accounting ledgers (whether in manual or software form). You should also keep clear records of all income sources, including interest, business income, or capital gains. These documents confirm that trust distributions come from legitimate income and that net income calculations in the tax return are accurate.

Documenting Retained Entitlements

When a distribution is retained by the trust instead of being immediately paid to a beneficiary, it creates an entitlement that must be properly documented and justified. The records should indicate whether the beneficiary requested to delay payment and confirm that unpaid amounts are recognised as liabilities. If a company is involved, any loan agreements must comply with Division 7A rules. Proper documentation helps prove that the trust operates within ordinary family or commercial dealing boundaries, rather than for tax avoidance purposes.

Corporate and Related Beneficiaries

If a company becomes presently entitled to trust income but does not receive the funds, the unpaid amount may be treated as a deemed loan to the trust. To remain compliant, ensure that formal loan agreements are in place, repayments and interest are recorded, and any demand payment clauses are documented. It’s also good practice to keep evidence of the company’s role in trust decisions or business operations, confirming that the entitlement is genuine and not simply a mechanism to reduce income tax.

Interpreting the ATO’s Risk Zones

The ATO uses risk zones outlined in Practical Compliance Guideline (PCG) 2022/2 to identify how much attention various trust arrangements attract.

Understanding where your trust sits within these zones helps you manage risk efficiently.

The Low-Risk Green Zone

Green zone scenarios attract minimal ATO scrutiny. These include arrangements where:

- Beneficiaries receive their entitlement within two years.

- Funds are used for their personal benefit or family living costs.

- The arrangement aligns with ordinary family or commercial dealing expectations.

For example, a trustee distributing trust income to family members for education, housing, or other living expenses generally falls into this low-risk category.

The High Risk Red Zone

Red zone scenarios draw ATO scrutiny and may trigger audits. These include:

- Adult children’s entitlements diverted to parents to repay historic expenses.

- Circular trust distributions between related entities.

- Distributions retained without a clear or documented purpose.

Trustees in this zone should seek professional advice and strengthen documentation immediately.

The Review or White Zone

White zone arrangements are uncommon but require clarification from the ATO through private rulings. Where trust entitlements arise in complex transactions or overlapping entities, obtaining professional guidance ensures your trust remains compliant with the ATO’s compliance approach.

Conclusion

Trustees play a vital role in managing trust distributions by ensuring each beneficiary’s present entitlement is genuine and supported by clear records. When the trust retains or controls funds representing a beneficiary’s share, trustees must document these amounts accurately and ensure they are used or repaid according to the trust deed and the beneficiary’s rights.

Maintaining accurate records of funds representing entitlements also helps trustees manage any repaid funds representing prior year distributions. Doing so ensures transparency about how trust income flows between beneficiaries and the trust, helping avoid misunderstandings or unintended tax implications.

Trustees should also document any beneficiary gifts or financial transfers carefully to show they are genuine and not linked to trust distributions. Good documentation protects against questions about whether these transactions involve real benefits or create legal or economic consequences under tax law.