Future‑Proofing Your Chart of Accounts: How to Design a Private Company COA That Can Scale to Multiple Entities

Future‑proofing your chart of accounts: how to design a private company COA that can scale to multiple entities starts with building a clean, consistent structure that works for any business entity in your group. A scalable COA lets you add new proprietary companies, trusts or partnerships while still producing clear reports for directors, shareholders and advisers. When your ledger is designed to grow, your team can spend more time on profit and performance and less time tidying accounts.

Define What “Future‑Proof” Looks Like for Your Group

Future‑proofing your COA means designing it so you can add new companies, locations or divisions without rebuilding the structure each time. You are aiming for a framework that is simple at the individual legal entity level but detailed enough to meet reporting obligations and support future growth. This helps privately held companies stay flexible while keeping control over how results are reported.

Think about where your group is heading over the next three to five years. That might include acquisitions, new trading names, new service lines or moving from a single entity to a more complex group structure. When you define that growth path, it becomes easier to shape a COA that can handle it.

Use a Scalable COA as the Foundation for Private Groups

A scalable COA is the backbone of any group of private companies, from a small group structure to larger corporations managing several entities. As soon as you have more than one business owned by the same members, the need to compare performance and combine results appears. Without a common structure, consolidation quickly becomes manual and time‑consuming.

Unlike public companies listed on the Australian Securities Exchange, most privately held companies do not report to the general public. However, they still have obligations under the Corporations Act 2001, ATO record-keeping, Goods and Services Tax (GST), Business Activity Statement (BAS), Pay As You Go (PAYG) withholding, Single Touch Payroll (STP) and superannuation guarantee rules. A scalable COA gives you a foundation that supports these obligations without over‑complicating day‑to‑day bookkeeping.

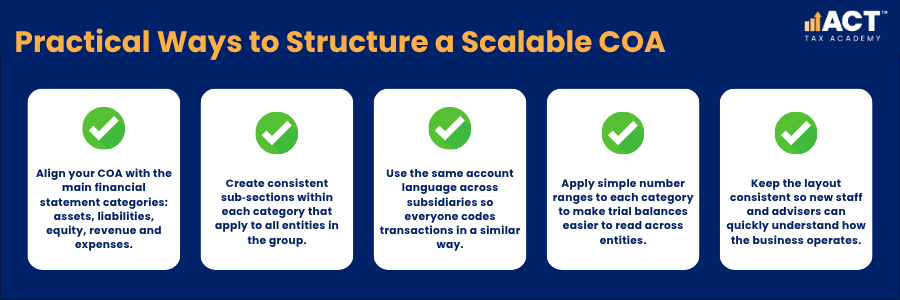

Structure Your COA in the Five Core Categories

A strong, scalable COA starts with the classic financial statement categories: assets, liabilities, equity, revenue and expenses. Within each category, you create consistent sub‑sections that every entity will use, such as current versus non‑current assets, and operating versus overhead expenses. This makes each trial balance easier to read and compare across the group.

Many Australian businesses then allocate simple number ranges to these categories so staff can navigate quickly. For example, assets might sit in the 1000 range, liabilities in the 2000 range, equity in the 3000 range, income in the 4000 range and expenses in the 5000 range. A shared pattern like this supports consistency when you add new entities or bring in new team members.

Standardise Names and Numbers Across All Entities

Standardisation is one of the most powerful tools in a multi‑entity COA. The same account number and name should mean the same thing in every company, regardless of which state or territory it operates in. This matters whether you have two entities or a broader network of private firms, including operations in the Northern Territory.

With standardisation, you can compare like‑for‑like figures quickly, without guessing what each account represents. It also makes reviews, audits and advisory conversations smoother because everyone is looking at the same structure. Over time, this reduces errors and speeds up monthly, quarterly and annual reporting.

Control New Accounts Instead of Letting Them Multiply

A future‑proof COA needs structure, not just freedom. Having clear rules about who can create new accounts and when they are allowed to do so stops the chart from becoming cluttered. Without these rules, ad‑hoc accounts creep in, making reporting and training more complicated.

A practical approach is to keep a core set of group accounts that are used everywhere and then allow a small, controlled band of entity‑specific accounts. New accounts should require approval and have a clear purpose that other accounts cannot meet. This protects your structure from unnecessary complexity.

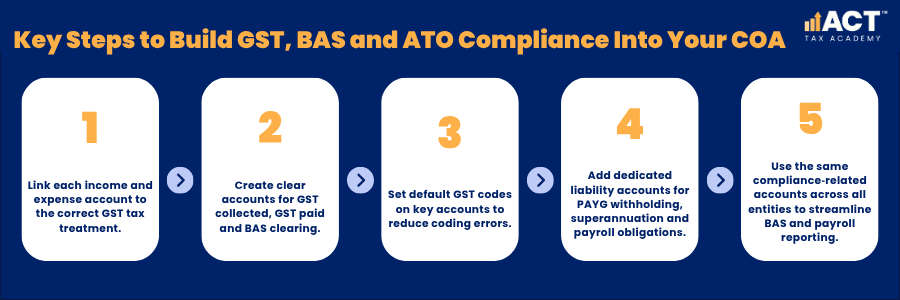

Build GST, BAS and ATO Requirements Into the COA

Your COA should support accurate GST and BAS record keeping from the start, rather than simply record figures after the fact. Each income and expense account should be linked to the correct GST treatment, whether the entity uses Simpler BAS, the GST instalment method or the full reporting method. Dedicated accounts for GST collected, GST credits and BAS clearing make it easier to reconcile amounts payable to, or refundable from, the ATO.

You also need clear liability accounts for PAYG withholding, superannuation guarantee and any other payroll obligations, supported by STP-enabled payroll reporting where required. These help you track PAYG withholding amounts payable to the ATO, wages or leave liabilities owed to employees, and superannuation guarantee contributions payable to super funds. When these accounts are consistent across entities, your BAS and payroll reporting becomes much easier to manage, especially when you understand how to calculate PAYG withholding for your business.

Separate Group‑Wide Accounts from Entity‑Specific Needs

A smart multi‑entity COA recognises that not every company will look exactly the same. The group master COA sets the standard for core income, expense, asset and liability accounts that all entities use. Around this, you can allow small ranges for entity‑specific accounts where there is a genuine need.

For example, a group might include one company focused on consulting services and another on product sales. Both use the same standard accounts for wages, rent and overheads, but each may have extra income and cost of sales accounts that reflect their different operations. This structure keeps your chart lean while still capturing important variation.

Make Consolidation Easier with Dedicated Intercompany Accounts

Consolidation becomes much more manageable when intercompany activity is clearly separated. Creating specific accounts for intercompany loans, management fees and recharges helps you identify these transactions quickly at month‑end or year‑end. That makes elimination entries more straightforward when preparing group‑level reports.

You also want your COA to map smoothly to the lines used in your group management reports and any general purpose financial statements. Even if you are not listed on a stock exchange, using a layout that mirrors standard financial statements makes it easier for lenders, potential investors and advisers to understand your numbers, including where structures involve bucket companies within a trust. That can be particularly valuable if you plan to raise capital or sell an interest in one entity.

Align Your COA With Australian Company Types and Rules

Different company types bring different expectations, even when they share similar day‑to‑day accounting needs. In Australia, the Corporations Act covers proprietary companies and public companies limited by shares, among others. Many ACT and regional clients operate as proprietary companies limited, which are a common form of private company.

Public companies and other entities that offer shares to the general public or list on the Australian Securities Exchange usually face stricter reporting requirements and more external scrutiny. They often need to prepare detailed annual reports for members and potential investors. While privately held companies do not have the same level of public reporting, taking inspiration from these standards can help you build a robust, investor‑ready COA.

Reflect Ownership and Control in the Way You Group Accounts

Ownership structure influences what your owners and directors want to see in the accounts. Private ownership usually means shares are held by a small group of members, such as family, partners or a handful of investors. Often, these companies cannot have more than 50 non‑employee shareholders, and shares are exchanged privately rather than traded on a public market.

Because a private company is a separate legal entity with its own assets and liabilities, the COA is the main record of how that entity uses its share capital and generates profit. Grouping accounts in a way that clearly shows core revenue streams, key costs and funding sources, and distinguishes assessable vs non‑assessable income, makes it easier for owners to understand performance. This helps them make decisions without needing to interpret complex accounting terms.

Use Cloud Accounting Tools to Push One COA Across Many Entities

Modern Australian cloud accounting systems make multi‑entity COA management much easier. Once you set up a master COA template, you can copy it into new entities as they are created. This avoids building each chart from scratch and helps maintain consistency across your group.

Most systems also offer tracking categories or classes that sit beside your COA. You can use these to track locations, cost centres or projects without constantly creating new accounts, and then feed that information smoothly into your BAS preparation and lodgment process. This approach gives you detailed reporting without overloading the chart with dozens of similar accounts.

Schedule Regular COA Reviews as Your Group Changes

A future‑proof COA is not a “set and forget” tool. Scheduling a review at least once a year helps you remove dormant accounts, merge duplicates and update descriptions that no longer reflect how the business operates. These reviews are particularly important when you add entities, move into new regions or change your service mix.

Regular reviews keep your COA aligned with your current business model and reporting obligations. TThey also give you a chance to check that GST, BAS, STP, PAYG withholding and superannuation guarantee accounts still reflect how transactions are processed in practice. Treating the COA as a living document keeps it useful and minimises confusion.

Avoid the Common Traps That Make Multi‑Entity COAs Hard to Use

There are a few traps that regularly undermine good COA design. Letting each entity create its own chart from scratch leads to inconsistent account names and numbers, making group reporting hard work. It also increases the risk of errors when people work across entities or move between roles, which can contribute to compliance issues such as being pushed into monthly BAS reporting for non‑compliant businesses.

Another trap is creating too many highly detailed accounts that only see occasional use. While these may feel helpful at the time, they can slow down coding and confuse staff who are not accountants. Focusing on accounts that support real decisions and compliance, rather than every possible variation, keeps your COA clear and efficient.

Use Your Future‑Proof COA as a Growth and Strategy Tool

A well‑designed, future‑proof COA is more than a compliance requirement; it is a tool for long‑term growth. It gives you a stable base as you add new entities, change ownership, reorganise structures or raise capital. Consistent accounts make these shifts easier to manage and easier to explain to stakeholders.

As your companies evolve, the COA helps you see which parts of the group drive profit, where costs are rising and how cash moves through the structure. That insight supports better decisions about investment, staffing and strategy. When your chart of accounts is built to scale, it grows with you instead of holding you back.