How to Build a Monthly Bookkeeping Workflow for Clients Caught by the Personal Services Income Rules

How to build a monthly bookkeeping workflow for clients caught by the personal services income rules starts with understanding that personal services income (PSI) is mainly a reward for an individual’s personal efforts or skills, rather than for using an income producing asset or selling goods. When the PSI rules apply, PSI received through a company, partnership or trust may need to be attributed to the individual who produced the income, and deduction rules may also be restricted. For sole traders, the income is already returned in the individual’s tax return, but the PSI deduction rules can still apply. Without a clear workflow, it is easy to mis‑code PSI amounts, miss certain deductions, and create problems when you go to report PSI in the income tax return.

What Makes Clients Caught by the Personal Services Income Rules?

Clients are caught by the personal services income rules when most of their income generated is a direct result of an individual’s personal efforts or skills, rather than from a business system or staff. If the PSI rules apply, the income tax treatment may require the PSI to be attributed to the individual who performed the work, particularly where it is earned through a company, partnership or trust. The rules apply even if the business structure is a company, trust or partnership.

A person can earn PSI in almost any business, but it is especially common where one client or a small number of clients pay for the individual’s time or expertise. When PSI rules apply to a personal services entity, there are limits on claim deductions, and special labels may be needed in the tax return. Knowing early that PSI may apply is the first step in building a useful monthly process.

Why Does a Tailored Monthly Bookkeeping Workflow Matter Under PSI?

Once the PSI rules apply, your client may not be able to claim the same range of deductions that a typical small business claims under the normal tax rules. For example, residential rent, mortgage interest, rates and land tax, along with payments to associates for non-principal work such as minor administrative or secretarial duties, should be coded to a ‘PSI review’ category because they are generally not deductible against PSI when the PSI rules apply. Avoid broad references to ‘home office expenses’, as some running expenses may need separate analysis depending on the facts and how they fit within what you can claim as tax deductions. If the bookkeeping system mixes these with normal operating expenses, it becomes hard to untangle at year‑end.

A monthly workflow designed around PSI means you separate PSI from non-PSI income and separately track expenses that may be deductible, non-deductible, or require review under the PSI rules. It also helps you track whether 80% or more of PSI comes from one client and its associates, because that affects whether the client can self-assess under some PSB tests. Over time, this structure reduces mistakes, supports accurate taxable income calculations and lowers the risk of unexpected tax liability.

How Should You Clarify PSI Status and Scope Before Setting Up the Workflow?

Before building any workflow, you should test individual’s PSI status by looking at each source of income. You ask whether the income produced by the contract comes from the individual’s efforts or from assets, employees or systems. If the income is mainly a reward for the individual’s personal efforts or skills, generally more than 50%, it will usually be PSI.

Next, work through the PSB tests. To self-assess as a PSB, the client must either meet the results test or meet one of the other PSB tests and also satisfy the 80% rule. If they meet one of these tests, they may be able to follow normal tax rules. Where they do not, you generally treat them as caught by PSI, unless a personal services business determination applies because unusual circumstances prevented them from meeting a test.

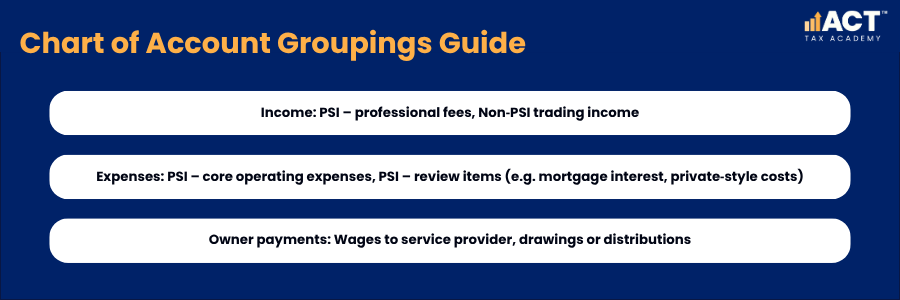

How Do You Structure the Chart of Accounts for PSI‑Affected Clients?

A PSI‑focused chart of accounts separates services income that is PSI income from other income produced by the same entity. You can create distinct income lines such as “PSI – consulting fees” and “Non‑PSI business sales” so that monthly reports clearly show how much of the income generated relates to personal services. This makes it easier to report PSI correctly and support the final income tax position.

On the expense side, set up separate accounts for operating expenses that are clearly linked to PSI, and for items that may not be fully deductible when PSI rules apply. For example, you might have accounts for “PSI – allowable deductions” and “PSI – review items” for costs like work-from-home and home office expenses or payments to associates. This layout lets you quickly identify certain deductions that could be limited under PSI.

What Monthly Data Should You Collect and Reconcile for PSI Clients?

Each month, collect full details of invoices, contracts and income received that relate to personal services. Make sure each transaction shows who the end client is, so you can see whether one client is providing most of the income produced. This level of detail also supports more frequent reporting, such as monthly BAS obligations for non-compliant businesses. This will help later when you check if the rules apply under the unrelated clients test or other PSB tests.

You should also gather and store supporting documents for expenses, with notes about how they relate to principal work and professional affairs. For example, mark which operating expenses relate directly to generating PSI and which relate to other parts of the business. This allows you to refine which deductions you can claim each month instead of guessing at year‑end.

How Can You Monitor the PSI Tests Throughout the Year?

The key PSB tests rely on patterns over the full income year, so waiting until year‑end to check them can be risky. Your monthly reports should highlight how much PSI comes from one client versus unrelated clients, and whether the arrangements look more like only salaries than a broader business operation. This helps you see early if PSI is likely to apply.

You can also review whether the client may meet the employment test by checking the ATO’s specific criteria and documenting worker usage carefully. For the business premises test, you track whether the client uses separate business premises that are used mainly for generating PSI and are not just a home office. As part of this, ensure payroll data is accurate and timely so you avoid STP non-compliance penalties. Documenting these points as part of your monthly routine makes it easier to decide if the client can still be treated as a personal services business.

How Do PSI Rules Change Deduction Treatment in Monthly Coding?

When PSI rules apply, the Australian Taxation Office often limits deductions to those that would be available to an ordinary worker earning personal income. This means certain deductions that look like business costs, such as retaining profits in an entity or claiming large home office expenses, may not be allowed against PSI. Your coding system needs to separate these items so you can review them before finalising the tax return.

For example, costs like mortgage interest, rent, rates or payments to family for minor admin can sit in a “PSI review” category until you decide whether they relate to other income produced or must be adjusted. Clear separation also helps show that you have treated PSI carefully and are not trying to gain a tax benefit from shifting PSI away from the individual. Over time, this reduces the risk of errors in taxable income and tax liability.

How Should Payroll, PAYG and Super Be Handled in the Workflow?

For clients using a personal services entity, the workflow should consider whether the PSI must be attributed to the individual and whether the entity has additional PAYG withholding obligations. Salary or wages already paid to the individual are taken into account in the attribution process. That means having a regular process to record and review these owner payments each month. If you treat them as wages, ensure they line up with other payroll and tax obligations, including how you calculate PAYG withholding for employees.

Your workflow should also review drawings or distributions carefully, because where the PSI rules apply, amounts may need to be reflected through the attribution rules rather than being treated as ordinary business profits available for discretionary distribution. If so, the PSI rules may require that these amounts be treated as if they were paid out as direct income to the individual. Recording these clearly in the books supports accurate income statement reporting and helps manage PAYG instalments to avoid tax surprises when it is time to prepare the income tax return.

How Do You Document PSI Decisions and Keep Records Ready for Review?

Good documentation is a central part of a PSI‑aware monthly workflow. For each client, create a short PSI file explaining why you think the rules apply or do not apply, including references to the PSB tests, unusual circumstances, and details of income generated. Update this file as circumstances change, such as winning new clients or taking on staff.

You should also keep a clear trail linking contracts, invoices and expense records to the PSI decisions you have made. When the time comes to report PSI and prepare the tax return, these notes will support your position. If the Australian Taxation Office later asks for further guidance or information, this documentation saves time and reduces stress.

When Should Clients Seek Professional Advice About PSI?

Because PSI can have a major impact on taxable income, the tax rate that applies and which deductions you can claim, clients should seek professional advice early. A tax professional can help self-assess whether the PSI rules apply, review the PSB tests and work out if a personal services business determination may be available in unusual circumstances. They can also assist with related obligations such as registering for PAYG withholding where entities pay salaries, and planning to maximise small business CGT concessions when business assets are sold. This guidance is especially helpful where such entities have mixed income from both personal services and other activities.

As the advisor, your role is to provide clear professional advice in plain language and help set up the monthly workflow that supports the agreed approach. If clients feel unsure or their work pattern changes, encourage them to ask for further guidance rather than guess how to treat PSI amounts. The earlier they talk to a tax professional, the easier it is to adjust the workflow and avoid surprises.

Conclusion

A strong monthly bookkeeping workflow for clients caught by the personal services income rules builds PSI thinking into everyday processes rather than leaving it to year‑end. By structuring the chart of accounts, coding rules and reports around personal services income PSI, you make it much simpler to test whether the rules apply, manage tax obligations and prepare a reliable income statement for the tax return. This approach helps clients understand the deductions you can claim and reduces the risk of a higher-than-expected tax liability.

When you combine clear systems with timely professional advice, you support clients who provide services in almost any industry, from information technology consultants to construction workers and medical practitioners. They gain confidence that their PSI is recognised, their tax position is sound, and their records are ready if questions arise. If you’d like to refine a PSI‑friendly workflow for your own client base, consider working closely with a trusted tax professional to tailor these steps to your practice.