ATO Payment Plans: What You Need to Know About Interest, Fees, and Eligibility

ATO payment plans: what you need to know about interest, fees, and eligibility becomes very real when you are staring at an arrears letter or myGov inbox reminder about overdue tax. When you understand how a payment plan ATO arrangement works, what interest applies, and who is eligible, you can deal with tax debt without guessing.

Why Understanding ATO Payment Plans Matters

If you are experiencing financial difficulties, falling behind on an activity statement, income tax or other liabilities can quickly affect your cash flow and peace of mind, which is why using PAYG instalments to smooth tax liabilities can be an important part of your strategy. The ATO now expects most people to use ATO online services and normal business channels to manage their account, view current account balances, and set up a payment method that fits their circumstances. Knowing the quickest way to deal with recent amounts owed can help you save money, avoid extra interest, and protect your business.

According to current ATO practice, a payment plan can help you pay what you owe over time instead of in one lump sum. At the same time, general interest charges still accrue GIC on your balance, and that interest compounds daily until the debt is cleared, which makes the length of your plan important. That is why it is worth taking a moment to look at your income, expenses and other finance options before you lock in instalments.

What Is an ATO Payment Plan and How Does It Work?

An ATO payment plan is an agreement that lets you pay overdue tax in regular instalments over an agreed period. Depending on the accounts involved, you may need separate payment plans. The ATO currently states that income tax accounts and activity statement accounts require separate payment plans. As long as you make each instalment on time and keep future tax debts paid in full and on time, your plan is more likely to remain in place.

Many individuals and small businesses can set up a payment plan online through ATO online services, including online services linked through myGov for individuals and Online services for business. You will usually need your tax file number, Australian business number if you have one, and your bank details so the ATO can set up direct debit payments from your account. Once approved, you can see your plan, recent amounts, and current account balances in your online services and keep an eye on how much debt you still owe.

How Does Interest Apply to ATO Payment Plans?

For unpaid tax debts, General Interest Charge (GIC) generally continues to apply until the balance is paid, unless the ATO grants a remission or an interest-free arrangement applies. This interest compounds daily, which means each day’s interest is added to your account and can itself start to earn interest if the balance is not reduced. Over time, this can make a long plan more expensive than it first appears.

Because interest compounds daily, the shortest period you can realistically manage will usually cost less in total than stretching your plan for several years. It is helpful to look at your income, expenses and any other loan or finance options you might access to see whether using bank finance or another product might cost less than relying on GIC for a long time. A good payment history on other accounts can sometimes make it easier to obtain finance at a lower rate than ATO interest.

Are There Fees or Penalties on ATO Payment Plans?

The ATO does not generally charge a separate setup fee for a payment plan, although card payments can involve card-related restrictions or third-party processing considerations depending on how you pay. However, penalties for late lodgment or late payment may still apply if you have outstanding activity statement lodgments or overdue returns, and companies can also face ASIC late fees for missed corporate filing deadlines, especially when lodgment history shows repeated delays. Interest on your debt continues to run while you are in the plan, so it is still important to pay extra when you can.

If you miss instalments, your payment plan default can lead to the plan being cancelled and more direct collection action. This can include letters, phone calls, or other steps that put pressure on your business and personal account. To avoid this, choose instalments you can afford and adjust the plan early if your circumstances change.

Who Is Eligible for An ATO Payment Plan?

Many individuals, sole traders and small businesses with tax debt may be eligible to request a payment plan if they are experiencing difficulty paying and meet the ATO’s conditions. The ATO will look at your lodgment history, recent amounts owed, annual turnover for your business, and whether you have tried to manage your tax obligations in good faith. They usually expect you to pay your debt over the shortest period you can reasonably afford, based on your income and other expenses.

Eligibility also depends on having all outstanding activity statement lodgments and returns lodged before or very soon after your plan is set up. For larger debts, the ATO may want more detail about your business, including cash flow, access to credit, and whether you have made efforts to obtain finance through normal business channels. Having a tax agent who understands your business can help you present your circumstances clearly and improve your chances of an approved arrangement.

What Interest Free Payment Plans or Concessions Might Apply?

Some small businesses with overdue activity statement amounts may be eligible for an interest-free payment plan of up to 12 months. These arrangements can apply to specific business activity statement debts when conditions are met, such as a reasonable lodgment history and only short periods in arrears. Where an interest-free payment plan is approved for eligible overdue activity statement amounts, GIC does not accrue for the agreed term of that arrangement.

These interest free options are usually aimed at businesses that are otherwise compliant but are experiencing financial difficulties for a short period. You will often need to show that you can make the required instalments without further default and that your business remains viable after the plan. A tax agent can help check whether you are eligible and how to structure a plan that takes advantage of any interest free period.

How Do You Set Up a Payment Plan Online?

The simplest way to set up a payment plan is often through myGov or ATO online services, where you can see your current account balances and recent amounts owed. In many cases, the system will guide you through a set of questions where you choose how much you can pay now and how much you can pay in future instalments. You can usually choose direct debit as your payment method, which helps your plan continue automatically each month. Payment frequency is generally weekly, fortnightly or monthly.

To set up a payment, you will need your bank details, tax file number, and, if you run a business, your Australian business number. Once you submit your details, you may receive an on‑screen confirmation and a letter or message in your myGov inbox outlining your instalment dates and amounts. If the online system cannot approve your plan, it will give you options to call by phone or contact your tax agent for more assistance.

How Have Recent Changes Affected the Cost of ATO Debt?

ATO tax debt continues to attract daily compounding GIC, and for April–June 2026 the annual rate is 10.96%. Even when you have a plan, general interest charges still apply and compounds daily, so the longer your balance sits unpaid, the more interest you pay. For many clients, this makes it important to compare the cost of GIC against other finance, such as a business loan, overdraft, or other way to obtain finance.

More people are now treating the ATO as a serious creditor rather than a flexible line of credit. When you weigh up your choices, it can help to review your income, recent amounts coming in, and any tax credits or refunds that might reduce your debt. This matters even more because ATO interest charges incurred on or after 1 July 2025 are no longer income-tax deductible. A tax agent or accountant can help you compare different options and work out which approach saves the most money over time.

What Happens If You Default on A Payment Plan?

If you miss an instalment or a new overdue liability arises, your payment plan can move into arrears or default status and may be cancelled. This means the remaining balance becomes immediately overdue again, and you may receive another arrears letter or contact by phone. The ATO may then look at other actions, which can be stressful when you are already managing tight cash flow.

Defaulting can also affect whether the ATO will approve another plan on similar terms in future, as it becomes part of your lodgment history and payment record. If you know you cannot make an instalment by the due date, the quickest way to limit damage is to adjust the plan early by contacting the ATO or asking your tax agent to step in. Often, showing that you are managing your money honestly and proactively makes it easier to keep some form of plan in place.

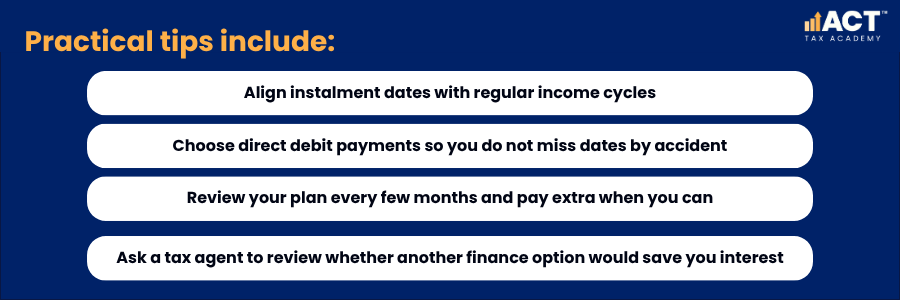

How Can You Make Your ATO Payment Plan Cash‑Flow Friendly?

The best plan is one you can stick to while keeping interest and stress down. This means setting instalments that reflect your income pattern, your expenses, and the other debts and liabilities you already manage. It can also mean paying a little extra when you have spare money, so you reduce the balance faster and save interest.

Before agreeing to a plan, it helps to prepare a simple budget so you know what you can truly afford each month without falling behind again. You might also look at whether to consolidate other debts, use a short‑term loan, or restructure parts of your business to meet superannuation due dates for employees, free up cash and improve your account balance over time. In some cases, applying any tax credits, refunds or future credits directly against your debt can also help you clear the plan sooner.

Conclusion

ATO payment plans can be a practical way to manage tax debt when you are experiencing financial difficulties, but they still come with interest and the risk of a payment plan default if instalments are missed. By using payment plan online tools, keeping your lodgments up to date, and choosing instalments that reflect your real income and expenses, you can stay on top of your obligations without losing control of your cash flow. Small steps like checking your myGov inbox regularly, keeping your bank details current, and using direct debit can make your plan run smoothly.

If you are worried about an arrears letter, recent amounts owed, or how general interest charges affect your balance, it may be time to get personal guidance. A trusted tax agent or accountant can help you understand your options, maximise allowable tax deductions to reduce future liabilities, talk to the ATO on your behalf, and design a plan that protects both your business and your peace of mind. Taking action early is often the quickest way to steady your account, save on interest, and get back to focusing on the work and life that matter most.