Private Health Insurance as a Tax Strategy: How to Legally Avoid the Medicare Levy Surcharge

Private Health Insurance as a Tax Strategy: How to Legally Avoid the Medicare Levy Surcharge is about using private health insurance to reduce extra tax and keep more of your money working for you. When your annual income rises above the MLS income threshold, you can often pay less tax by holding the right private hospital cover instead of simply paying the extra charge. This is a practical way for higher income earners in Australia to protect both their health and their finances.

Many Australian taxpayers are surprised at tax time when they see a separate Medicare Levy Surcharge amount added on top of the standard Medicare levy. This extra tax is calculated by the Australian Taxation Office on your tax return using your taxable income, your family income, your spouse status and whether you hold hospital cover for the full financial year. With clear guidance and the right hospital policy, you can avoid paying this surcharge and still support the public healthcare system through the normal levy.

What Is the Medicare Levy Surcharge and When Does It Apply?

The Medicare Levy Surcharge (MLS) is an additional tax that applies to higher income earners who do not hold appropriate hospital cover for MLS purposes. It is charged on top of the standard Medicare levy that most Australian taxpayers already pay as their contribution to the public system. The surcharge is designed to encourage individuals and families with higher incomes to take up health insurance and use private hospitals when they need private patient hospital cover.

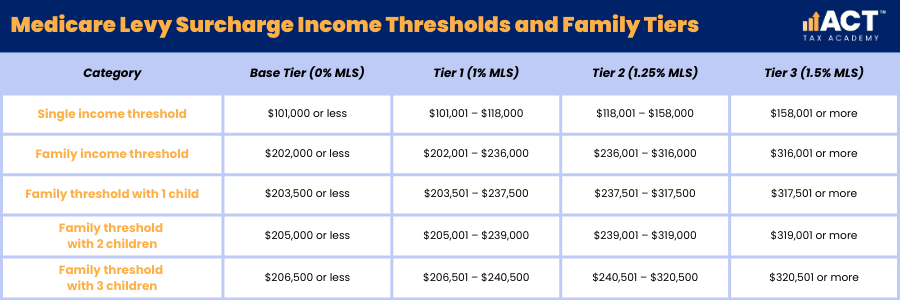

You become liable for the MLS when your income exceeds $101,000 for singles or $202,000 for families (2025–26 financial year), with higher surcharge rates applying at higher income tiers. These thresholds include your own income, your spouse’s income and, in many cases, your combined income as a family. If you are above the family threshold or the single threshold and you do not hold hospital cover for the full year, you can expect extra tax at tax time for surcharge purposes.

How Does Private Hospital Cover Help You Avoid the Medicare Levy Surcharge?

The main way to avoid the Medicare Levy Surcharge is to hold hospital cover that meets the appropriate level set for Medicare Levy Surcharge purposes. This means you need private hospital cover or private patient hospital cover, not just extras, with an Australian health insurer. When you hold hospital cover that meets the rules for the full financial year, you are usually exempt from paying the MLS.

If you only hold hospital cover for part of the year, the surcharge may still apply on a partial basis, which is sometimes called a partial exemption. In that case, the Australian Taxation Office works out how many days you held hospital cover and how many days you did not, then applies the surcharge to the uncovered days. To fully avoid paying the MLS, you generally need to hold hospital cover for the full year, or at least make sure it is in place before you cross the relevant income thresholds.

What are the Current Income Thresholds and Family Tiers for MLS?

MLS income thresholds are based on your taxable income, reportable fringe benefits, total net investment losses, reportable super contributions and your spouse’s income if applicable. There are separate thresholds for singles and families, and within those groups there are several family tiers based on how high your income goes. As your income rises, the surcharge rate usually increases, which means the extra tax you pay also increases.

For families, there is also a special definition of family income threshold that takes into account your spouse and each dependent child for surcharge purposes. The family threshold increases by $1,500 for each dependent child after the first child, which can slightly reduce the chance of paying the MLS for larger families. However, if your combined income continues to rise, you may still be subject to higher tiers of the surcharge.

When Is Private Health Insurance a Smart Way to Pay Less Tax?

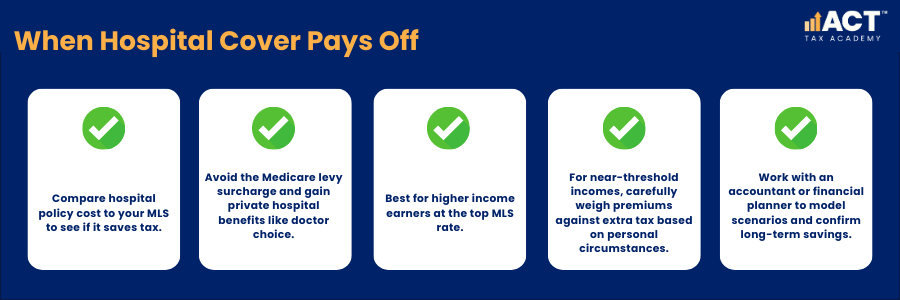

Private health insurance becomes a smart tax strategy when the cost of an appropriate hospital policy is similar to or lower than the MLS you would otherwise pay. In this situation, you can avoid the Medicare Levy Surcharge and still gain access to the benefits of private hospitals, such as more choice of doctor and shorter waiting times. This is especially relevant for higher income earners whose MLS rate is at the top end of the scale.

If your income is only just above the MLS income threshold, the numbers may be closer, and it is important to consider your personal circumstances. You need to weigh the cost of premiums against the extra tax you would pay if you did not hold hospital cover. Working with a trusted accountant or financial planner can help you model different scenarios and decide whether private cover will genuinely help you pay less tax over the long term.

What Type of Hospital Policy Do You Need for MLS Purposes?

Not every health insurance product will help you avoid the Medicare Levy Surcharge. For MLS purposes, you must hold hospital cover that provides at least a basic level of hospital treatment as an admitted patient, not just extras like dental or optical. The policy needs to meet the appropriate level rules, including maximum excess limits of $750 for singles and $1,500 for couples and families.

You do not always need a top-level policy to qualify for MLS exemption, but you should check that your chosen hospital policy is recognised as appropriate hospital cover for surcharge purposes. Many insurers offer relatively simple private cover aimed at helping Australian taxpayers avoid the MLS while still providing essential hospital benefits. Always keep your policy documents and provide them to your accountant at tax time so your MLS position is correctly recorded.

How Much Extra Tax Can You Avoid Paying with Private Hospital Cover?

The amount of extra tax you can avoid paying depends on your annual income, the MLS rate that applies to you and the cost of your hospital cover. For many higher income earners, the surcharge can add up to thousands of dollars over a full year if they are liable for the highest rate and do not hold hospital cover. In these cases, the premium for a suitable hospital policy is often lower than the extra tax that would otherwise be charged.

For example, if your income is well above the top MLS tier and you do not hold hospital cover, the surcharge can be a significant extra tax line in your tax account at the end of the financial year. By taking out a suitable hospital policy for the full year, you may be able to avoid the Medicare Levy Surcharge entirely and redirect that money into cover that supports your health. The key is to compare the cost of premiums with the surcharge you would otherwise pay.

How Does MLS Encourage People to Use the Private System?

The design of MLS is intended to encourage individuals and families with higher incomes to use the private system instead of relying only on the public system. By adding a surcharge to tax bills for those who do not hold hospital cover, the government aims at encouraging people who can afford private insurance to take out cover. This reduces pressure on the public healthcare system so that most Australian taxpayers can continue to access Medicare benefits and public hospital care when they need it.

When enough people hold private cover, some planned treatments and elective procedures move from public hospitals to private hospitals, freeing up public resources for urgent cases and those without insurance. In this way, MLS is not just an extra tax; it is also a tool used by the government to shape how healthcare is funded and delivered in Australia. Understanding this purpose can help you see why the rules are linked so closely to income and family structure.

What Family Rules, Children and Exemptions Should You Be Aware Of?

When you have a spouse or children, the MLS rules use family income and combined income instead of just your personal income. This keeps the system consistent across couples and families, including de facto couples, and recognises that more than one person may be contributing to household income. If you are in a relationship, it is important to look at your full situation together rather than just one person’s income.

The family threshold uses a base level, which is then increased for each child after the first for MLS purposes. A dependent child can change your MLS position because they expand your family unit under the rules and influence your family threshold for surcharge purposes. To be fully exempt from the MLS as a family, you and your spouse need to hold hospital cover that includes your first child and any additional child for the full year or for the periods when you are above the threshold.

How Does MLS Work with Emergency Ambulance, Extras and Other Cover Types?

Many people hold cover for emergency ambulance or extras, such as dental and physio, and assume this is enough to avoid the Medicare Levy Surcharge. In reality, these types of cover do not count as hospital cover for MLS purposes and will not exempt you from the surcharge. They can still be valuable for managing health costs, but they are not enough on their own to avoid the MLS.

If you want to avoid the MLS and still keep your existing extras and ambulance cover, you can usually add a basic hospital policy or upgrade to a combined product. This lets you keep the benefits you value while also holding hospital cover that meets the appropriate level for MLS. The important step is to confirm with your insurer that your product counts as hospital cover for exemption purposes.

How Can ACT Tax Academy Help You Use This Strategy Effectively?

At ACT Tax Academy, we help you look at your income, family structure and personal circumstances to decide whether private hospital cover is a sensible way to avoid the Medicare Levy Surcharge. We examine your taxable income, any spouse or family income and how these fit within the MLS income threshold for the current financial year. This helps you see clearly whether you are likely to be subject to the surcharge and how much extra tax you might pay without cover.

We then work with you and, where useful, your financial planner to compare the expected surcharge with the cost of different levels of hospital cover. Our aim is to help you avoid paying unnecessary extra tax while keeping your approach realistic and tailored to your situation. We also make sure that any decisions around health insurance are properly reflected in your tax return so that your MLS position is correctly calculated and you receive any exemption you are entitled to.

Conclusion: What Should You Do Before Your Next Tax Time?

Private Health Insurance as a Tax Strategy: How to Legally Avoid the Medicare Levy Surcharge can be a practical way to avoid extra tax, especially if your income or family income is above the current thresholds. By understanding how MLS is calculated and how hospital cover interacts with your tax, you can make a clear, informed choice that suits your health needs and your budget. This is not about chasing complicated schemes; it is about using simple, well-established rules in a way that works for you.

Before the next financial year is over, take time to review your income, your family structure and any cover you already hold. If you think you might be liable for MLS, talk with our team at ACT Tax Academy so we can help you assess your options and, where appropriate, set up hospital cover that avoids the surcharge. With the right plan, you can support both the public system and your own peace of mind while paying no more tax than you need to.