How to Use the Medicare Levy Calculator for Personal and Business Tax Planning

Using the Medicare levy calculator for personal tax planning, including planning for business owners, is about turning a simple online calculator into a practical way to estimate how much Medicare levy you may pay and plan ahead. For most taxpayers, the Medicare levy is 2% of taxable income, and if you do not hold an appropriate level of private patient hospital cover, the Medicare levy surcharge (MLS) may apply on top. When you understand how the ATO Medicare levy calculator works, you can make clearer decisions about health insurance, cash flow, and tax for the financial year.

What Is the Medicare Levy Calculator and Why Does It Matter?

The Medicare levy calculator is an online tool on the ATO website that helps you estimate your Medicare levy and whether MLS may apply, based on details such as your taxable income, spouse income, private patient hospital cover, Medicare exemption days, and whether you are entitled to the Seniors and Pensioners Tax Offset (SAPTO).

As currently published, the calculator estimates Medicare levy for income years from 2013–14 to 2024–25, so for 2025–26 planning you should also check the current ATO threshold pages and related calculators. Although it cannot tell you the final figure to the dollar, it gives an estimate you can use for guidance.

This is important because the levy and MLS are on top of your normal income tax, and the total pay depends on your personal circumstances and annual income. If you are not prepared, the levy and surcharge can feel like extra tax that suddenly appears on your notice of assessment. By running the calculator early, you can see how your circumstances may affect what you pay, and you can take steps to reduce stress and manage money better.

How Does the Medicare Levy Work in Australia?

The Medicare levy helps fund Australia’s public health system, including access to hospital services and rebates when you visit a doctor. Most taxpayers pay the levy at 2% of their taxable income, but there are threshold levels where the levy is reduced or you may be exempt. People on lower incomes or who meet special rules can avoid the full levy or pay a smaller amount.

If your income is below a certain threshold for the full financial year, you may not have to pay the levy at all. If your income is slightly above the base threshold, you may pay a partial levy that gradually increases until you reach the full rate. Your age, spouse income, and whether you have dependants or a child can also affect how much you pay or whether a reduction applies.

What Is the Medicare Levy Surcharge and How Does It Affect You?

The Medicare levy surcharge is an extra charge on top of the standard levy for people whose income for MLS purposes is above the relevant threshold and who do not hold an appropriate level of private patient hospital cover. It is designed to encourage higher-income earners to take out private hospital cover and reduce pressure on the public hospital system. For MLS purposes, the ATO uses a special income test and your family status to work out whether the surcharge applies.

If you do not have an appropriate level of private patient hospital cover and your income for MLS purposes is above the MLS thresholds, you may pay MLS at 1%, 1.25% or 1.5%. The MLS is separate from Lifetime Health Cover and is assessed each financial year. By understanding these thresholds and using the ATO Medicare levy calculator together with the relevant ATO income test or private health insurance rebate tools, you can judge whether taking out hospital cover might save you money.

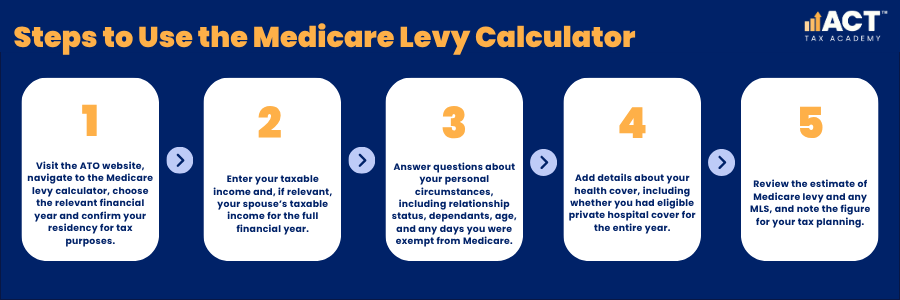

How Do You Use the Medicare Levy Calculator Step by Step?

To use the Medicare levy calculator, you first need basic information such as your taxable income, whether you had a spouse during the year, and whether you had dependants or dependent children. You also need to know if you had any exemption periods, for instance if you were not eligible for Medicare for a period in the year. Having your latest pay slips or a draft tax summary makes this easier.

How Can Individuals Use the Calculator for Personal Tax Planning?

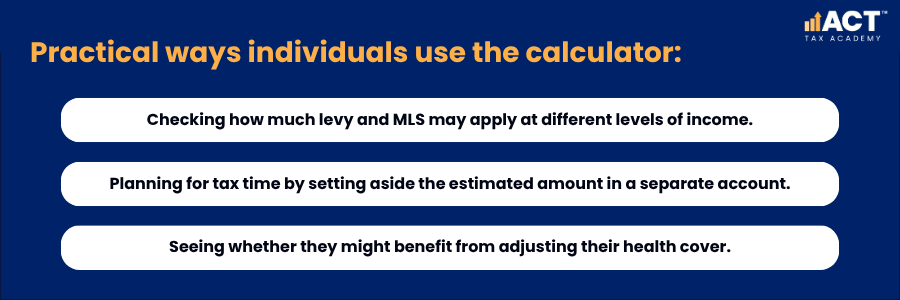

For individuals, the calculator is a simple way to forecast how much tax and levy you may pay based on your current or expected income. You can run different scenarios to see how extra overtime, bonuses, or investment income will affect your final position. This helps you avoid paying more than expected and gives you time to adjust your budget.

For example, you might increase your tax withheld through payroll if the calculator shows a higher levy or MLS for the year. You can also see how legitimate deductions might reduce your taxable income and Medicare Levy. However, salary sacrifice to super does not necessarily reduce MLS exposure, because reportable super contributions are included in income for MLS purposes. Single people, single-parent households, and couples with children can each use the tool to see how family structure impacts the outcome, especially when combined with strategies such as using PAYG instalments to avoid tax surprises.

How Can Business Owners Use the Calculator for Tax Planning?

Business owners and company directors can use the calculator as part of their personal tax planning once they have estimated their own taxable income from wages, dividends, trust distributions, and other sources. The calculator does not calculate business tax, but it can help an owner understand how their personal income profile affects Medicare levy and MLS exposure.

By modelling different personal income scenarios, business owners can test how higher or lower wages, dividends, or trust distributions may affect their personal levy position for the year. This can support cash-flow planning, decisions about how much to set aside for year-end tax, discussions with an accountant about the timing and mix of personal income, and how this fits alongside lodging your BAS as a business owner.

Useful actions for business owners:

- Modelling different personal income levels and checking the levy impact.

- Comparing scenarios where trust distributions, dividends, or wages change personal taxable income.

- Using the estimate to plan personal cash flow and avoid a large bill at tax time.

How Does Private Health Insurance Link to the Medicare Levy Surcharge?

The MLS is directly tied to whether you hold an appropriate level of private patient hospital cover for yourself, your spouse, and your dependants where required. If you or any relevant family member do not have that level of cover and your income for MLS purposes is above the threshold, you may pay this extra tax each year. Extras cover such as dental, optical, physiotherapy, or ambulance cover does not count as private patient hospital cover for MLS purposes.

By using the Medicare levy calculator and the ATO or PrivateHealth.gov.au tools for income tiers and rebate percentages, you can estimate whether the surcharge is likely to apply and how much it might cost. You can then compare that amount with the premium for an appropriate level of hospital cover. Private hospital cover may be more cost-effective in some cases, but the private health insurance rebate is income-tested and may be reduced or nil at higher income tiers, just as stricter rules also apply when you claim work-from-home tax deductions correctly.

How Does the Private Health Insurance Rebate and Lifetime Health Cover Affect Planning?

The private health insurance rebate is a government contribution towards the cost of eligible private health insurance premiums. The rebate percentage depends on your age and income, and because it is income-tested, some taxpayers may receive a reduced rebate or no rebate at all. This can affect whether holding hospital cover is cost-effective when compared with MLS.

Lifetime health cover is a separate rule that encourages people to take out hospital cover earlier in life. If you delay taking out hospital cover until after a certain age, a loading may apply to your premium for a long period. When you combine these rules with the levy and MLS, the timing of when you start or keep hospital cover can make a big difference over the years.

What Common Mistakes Should You Avoid When Using the Calculator?

Many users accidentally enter their gross income rather than their expected taxable income, which leads to an overestimate of how much levy they will pay. Others forget to include details about their spouse, dependants, or exemption periods, which can change the result. Some also overlook the need to select the correct financial year and end up using outdated thresholds, particularly when they are not working from a clear business tax return documents checklist or broader guidance on how to avoid common tax return mistakes.

Another common mistake is assuming that any health cover removes the MLS. In reality, you need an appropriate level of private patient hospital cover for MLS purposes, and extras cover alone does not count. It is also important to remember that the calculator is an estimate tool; the Australian Taxation Office (ATO) calculates your final tax and levy when you lodge your return.

What Are Your Next Steps with Medicare Levy Planning?

If you want to get more value from the Medicare levy calculator for personal and business tax planning, start by gathering your latest income, health insurance, and family details. Then visit the ATO website, run a few scenarios using the calculator, and note any areas where your levy or MLS might change. Pay attention to how your decisions around eligible hospital cover, private hospital insurance, and income levels can affect how much tax you pay.

From there, consider speaking with an accountant who understands both tax and health-related rules in Australia. With the right support, you can plan your tax, health, and business decisions together, including how you handle obligations such as BAS due dates for your business, what happens if you lodge BAS late, and your wider FBT lodgment obligations alongside Fringe Benefits Tax for employers, so they work in your favour across the full financial year, not just at tax time.