How to Use Tax Return Estimates for Smarter Cash Flow Management

How to use tax return estimates for smarter cash flow management starts with using an income tax calculator or simple tax calculator to estimate tax return outcomes and build them into your budget. When you understand how much tax has been withheld from your income, what your taxable income is, and whether you are tracking towards an estimated tax refund or tax payable, you can plan your cash more confidently. Turning your tax return calculator results into a clear plan helps smooth out tight periods, reduce stress and avoid last‑minute scrambles to pay a tax bill.

Cash flow planning is easier when you treat your estimated tax, refund or amount of tax payable as part of your regular money cycle rather than a once‑a‑year event. By updating your estimate as your income, expenses and tax deductions change, you keep your plan aligned with your circumstances. This approach is especially helpful for a sole trader, anyone with other income such as investments or capital gains, or anyone repaying a higher education loan program or trade support loan.

What is a tax return estimate and how is it calculated?

A tax return estimate is a guide to whether you will receive a tax refund or need to pay tax when you lodge your tax return and receive your notice of assessment. It is based on your taxable income, tax rates for the year, tax paid or withheld by your employer, tax offsets, the medicare levy and, if it applies, the medicare levy surcharge. Online tools such as an income tax calculator, tax refund calculator or tax return calculator help you see an estimated tax refund or tax payable depending on your circumstances.

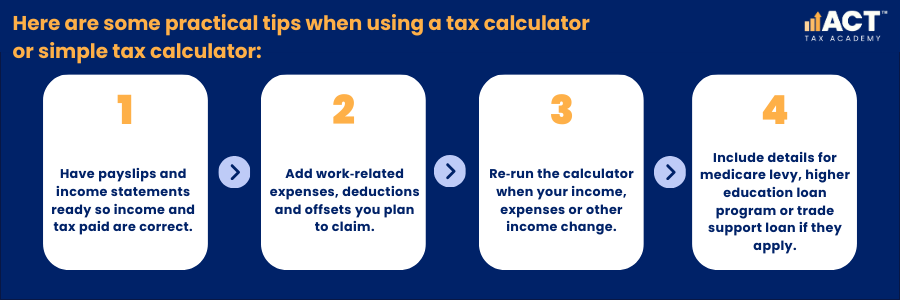

To estimate tax return outcomes, you usually enter income details, tax withheld, and expected deductions and offsets into a calculator. The calculator results show how much tax is likely payable or how much refund you may be entitled to, taking into account income tax, Medicare levy and other components such as higher education loan program repayments. Remember that the estimate can change if you add additional information later, so treat it as a planning tool and not a final result.

Why do Tax Return Estimates Matter for Cash Flow?

Tax return estimates matter because they tell you if money is likely to leave your account as tax payable or arrive as a refund, and roughly when. Knowing this in advance gives you time to adjust your regular payments, set aside funds, or plan how to use any refund. It also helps answer the common question of “how much tax will I pay or get back this year” without waiting until you lodge.

When you include your estimate in your cash flow plan, you can line up large payments such as rent, loan payments or business expenses around your expected tax outcome. For example, if the estimate suggests a higher rate of tax and a tax bill is likely, you can start moving smaller amounts into a separate account now. If an estimated tax refund is on the way, you can decide whether to use it to reduce debt, invest, or cover upcoming costs.

How to Use Calculators to Estimate Tax Return Outcomes

Most calculators ask for your income, tax withheld, deductions and any other income such as interest, dividends or capital gains. You may also be asked to add medicare levy surcharge details, higher education loan program or trade support loan amounts, and any tax offsets you can claim. Once you calculate, the tool will show an estimate of tax on your taxable income, tax paid so far and any refund or amount payable.

Estimated Tax Refund into a Planning Tool

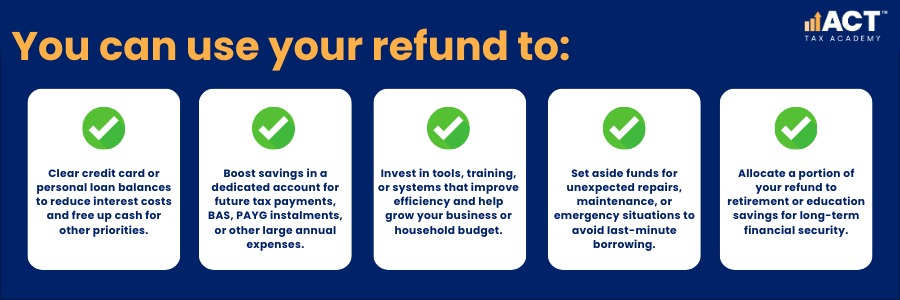

If the estimate shows a refund, resist the urge to treat it as a bonus and spend it straight away. Instead, build the estimated tax refund into your cash flow plan as a specific line item, with an expected amount and month, and only commit the funds once they land in your account. This helps you avoid over‑committing if the final refund is lower than expected.

When your Estimate Shows Tax Payable

If the calculator suggests tax payable, start planning for that tax bill as soon as possible. Break the estimated amount of tax into smaller regular transfers into a separate tax account so it is ready when you lodge your tax return. This approach works whether you are a sole trader with no employer withholding tax, or an employee with significant other income.

You can also check whether your employer is withholding enough from your pay and adjust if needed so the tax on your taxable income is closer to the final outcome. Where appropriate, discuss with a tax agent how to improve your deductions or structure so future tax bills are more manageable, always keeping things simple and clear. If cash is tight, asking for help early gives you more options than waiting until the notice arrives.

Building Tax into Your Ongoing Cash Flow Forecast

A good cash flow forecast shows all money going in and out of your account by week or month, including tax. Add your estimated tax refund or tax bill as a line in the month you expect to lodge your tax return and receive your refund or pay your bill. If you use budgeting software or a spreadsheet, label the entry clearly so you remember it relates to income tax.

Update your forecast whenever your estimate changes so your plan stays realistic. For example, if your income grows and the calculator shows a higher tax payable, you can increase the regular amounts you set aside. If a new deduction or tax offset reduces your estimated tax, you may decide to redirect part of the funds you had reserved.

Practical Examples of Using Estimates

A sole trader might run a tax calculator each quarter using details from their invoicing and expense records to estimate tax and medicare levy. They then set aside a percentage of each payment received into a separate tax account, based on the amount payable shown in the calculator results. When they lodge, the tax bill is covered and, if the estimate was conservative, any small refund becomes a bonus buffer.

An employee with a higher education loan program balance and some other income, such as a small capital gains event, might use a tax refund calculator to check the impact on their tax return. Seeing that the extra income pushes them into a higher rate band and reduces any refund, they may increase their pay‑as‑you‑go withholding through their employer to avoid a surprise. Simple steps like this make it easier to manage payments, claim the right deductions, and keep their account in good shape at tax time.

When to Ask a Tax Agent for Help

If your situation involves multiple sources of income, complex deductions or important life changes, a tax agent can help you interpret your estimate and plan your cash flow around it. They can also show you how to use a tax calculator or income tax calculator properly so your estimate tax result is as reliable as possible. This is especially useful if you run a business, have significant investments, or need to understand how future 2025 tax changes might affect you.

A registered agent can guide you through which expenses you can claim, what additional information is needed for tax purposes, and when to lodge your tax return. They can also help you adjust your planning if your notice of assessment is different to your estimate, or if you need to set up payments. For many people, this support turns tax from a once‑a‑year worry into a steady, manageable part of their financial routine.