Division 7A Compliance: Avoiding Common Record-Keeping Errors

Division 7A compliance is one of the key areas that business owners must get right to avoid adverse tax consequences. Many small to medium private companies unintentionally breach Division 7A because of poor record keeping. This can lead the Australian Taxation Office (ATO) to treat drawings or loans as unfranked dividends rather than legitimate complying loans.

Understanding Division 7A

Division 7A exists to prevent private companies from distributing company profits to shareholders or their associates in a way that escapes proper taxation. It covers loans, payments, and debt forgiveness made to shareholders or associates that may not have a genuine income producing purpose.

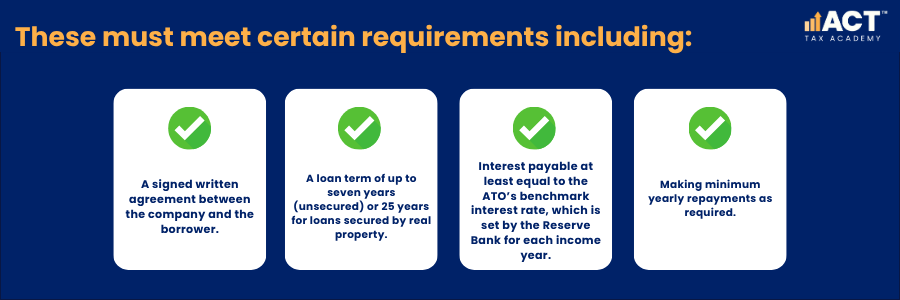

Under these tax rules, if a company makes a loan to a shareholder and doesn’t put a complying loan agreement in place before the lodgement date of the company’s tax return, the transaction may be treated as a deemed dividend. The key to avoiding this outcome is having accurate documentation and compliant loan agreements that follow the legal requirements.

The Role of Complying Loan Agreements

A complying loan agreement ensures that any funds provided to shareholders or interposed entities are formally recognised as Division 7A loans.

A compliant loan preserves the company’s tax position and ensures that distributions do not become unfranked dividends.

Why Record Keeping Matters

Poor record keeping is one of the most common risks under Division 7A. Every payment or loan amount made to a shareholder or associate must have clear evidence – showing when it was paid, why it was paid, the interest rate, and the repayment schedule. Take note of the following record keeping mistakes:

- Each minimum repayment must be supported by payment evidence like bank statements or receipts. Without these, the ATO can treat the loan balance as unpaid or incorrectly recorded.

- If a business owner pays for a personal expense from company assets, this is treated as a Division 7A loan. Without a proper loan agreement, the ATO can reclassify it as a deemed dividend.

- Loan agreements must be completed before the company’s tax return is lodged. A late or missing complying

- The Division 7A benchmark interest rate (also known as the Div 7A interest rate) changes each financial year. For example, if the minimum interest rate is not applied, the loan may be non-compliant.

How Inaccurate Records Impact Businesses

Failing to maintain proper records can lead to adverse tax consequences, where the ATO reclassifies Division 7A loans as unfranked dividends. This often results in paying additional income tax at the shareholder’s marginal rate, impacting cash flow and ongoing business operations.

Best Practices for Staying Compliant

Maintaining systematic and accurate records helps businesses prevent unnecessary issues and demonstrate compliance with Division 7A rules.

Maintain a Central Division 7A Register

Setting up a Division 7A register—whether digital or physical—helps track all 7A loans, repayments, and related details such as interest payable, loan amount, and due dates. This approach ensures that all complying loans are actively monitored throughout the financial year.

Prepare Loan Agreements Early

Draft and sign loan agreements well before the lodgement date of your company’s tax return. Clearly outline the loan term, interest rate, and repayment schedule. Agreements should reference the ATO’s benchmark interest rate and meet the legal standards under the Income Tax Assessment Act.

Record All Transactions Accurately

Every loan, repayment, and payment of interest should be clearly recorded and reconciled against the agreement. Regularly comparing payments to the required minimum yearly repayments ensures your Division 7A loan remains compliant.

Conduct Regular Reviews

Schedule quarterly or half-yearly reviews to check your loan balance, interest, and repayments. This helps to ensure businesses stay on schedule and allows time to make increased repayments if an error or shortfall occurs.

Involve a Chartered Accountant

Working with a chartered accountant experienced in Division 7A ensures that all loan agreements, repayments, and benchmark rates meet current requirements. They can also help identify issues such as unpaid present entitlements or incorrectly structured trust structures that could inadvertently breach Division 7A.

Managing Trust Structures and Interposed Entities

In certain circumstances, trust structures and interposed entities can fall under the scope of Division 7A. For example, unpaid present entitlements or loans via a bucket company may trigger Division 7A if the funds benefit shareholders or their associates. Proper documentation helps demonstrate the income producing purpose of such transactions and ensures compliance with the tax assessment act 1936.

Correcting Errors Under Division 7A

If you discover a breach, act quickly. The ATO allows corrections in certain circumstances, such as entering a complying loan agreement, making late minimum repayments, or applying for the Commissioner’s discretion. Addressing issues promptly demonstrates good intent and helps stay compliant while minimising penalties.

Using Technology to Simplify Record Keeping

Modern accounting systems like Xero and MYOB can automate entries, schedule minimum repayments, and calculate the Div 7A interest rate. These tools reduce manual errors and keep your Division 7A register current. However, automation doesn’t replace compliance—you must still ensure the loan agreement, interest payable, and loan term meet legal requirements.ing professional guidance ensures your trust remains compliant with the ATO’s compliance approach.

Conclusion

Division 7A is a complex area of taxation, but with effective systems and consistent attention to record keeping, compliance becomes manageable. Proper records, complying loan agreements, and regular reviews help your company avoid having loans treated as deemed dividends.

At ACT Tax Academy, we help Australian businesses manage Division 7A obligations with clarity and care. Our team of chartered accountants can guide you through complex tax rules, maintain compliance, and support your next steps. Taking the time to organise your Division 7A records today helps protect your tax position, supports better cash flow, and allows your business to focus on what it does best—managing successful business operations.