Claiming All Your Business Deductions: A Checklist to Maximise Your Tax Return

Claiming All Your Business Deductions: A Checklist to Maximise Your Tax Return helps you reduce your taxable income, so you pay only the tax you need to, and no more. When you get your business deductions right, you lower your tax liability and often increase your tax refund, which can feel like getting money back for all your hard work. This can make a real difference to your cash flow and your financial decisions for the next income year.

Why Your Business Deductions Directly Affect Your Tax Refund

Many business owners wonder, “How much tax will I get back?” but the better starting point is to understand how your total income and expenses flow through your tax return. Your assessable business income (for example, your sales, wages to yourself, and other payments) forms part of your gross annual income, which is then reduced by deductions to arrive at your taxable income. From there, the Australian income tax system applies tax rates, your marginal tax rate, any tax offsets, the Medicare levy and possibly the Medicare levy surcharge to work out the total tax payable.

According to ATO research on the small business tax gap, around 25% of the combined small business gap is due to overclaimed deductions (48% for small companies and 20% for individuals in business), which shows how easy it is to get this wrong without good guidance. At the same time, many taxpayers focus on how much tax they paid or how much tax was withheld by an employer or through PAYG instalments but overlook smaller business expenses that could legitimately reduce their tax. With a clear checklist, you can approach each financial year calmly and make sure your return reflects your real position.

What Makes a Business Expense Deductible?

A business expense is generally deductible for tax purposes if it is directly related to earning your business income and is not private or capital in nature. In practice, that means being able to show a clear connection between the expense and your business activities, and that it was incurred in the relevant tax year. If there is a mix of private and business use, you normally claim only the reasonable business portion.

The amount of tax you save from each deduction depends on your marginal tax rate and your overall total income for the year. For example, a dollar of expenses will save more tax for a business owner in a higher rate than one in a lower rate, even though the deduction itself is the same. This is why your individual circumstances and other factors, such as whether you are an Australian resident for tax purposes, have private health insurance or salary sacrifice arrangements, all influence your final tax outcome.

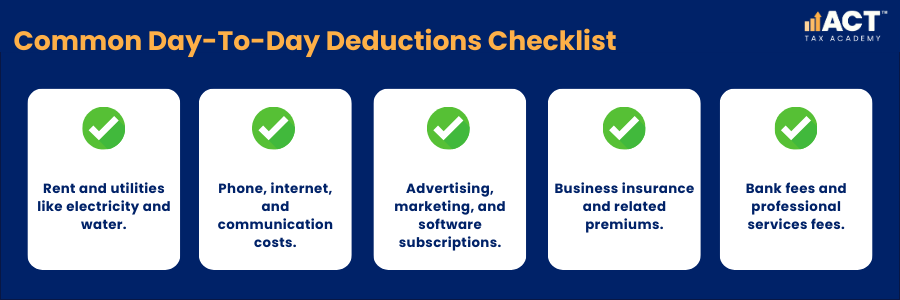

What is the Most Common Day‑To‑Day Business Deductions?

Day‑to‑day operating costs are usually the easiest deductions to identify and claim in your tax return. These include items like rent, electricity, insurance, phone, internet, advertising, bank fees, software, and professional services such as using a registered tax agent. Because these costs are directly tied to running your business, they often reduce your taxable income in a straightforward way.

If you keep your business income and expenses flowing through a separate account, it becomes much easier to check that everything has been captured. Looking at your account and bank statements across the financial year helps you see all the payments that relate to business, from small app subscriptions through to annual insurance. This directly affects your estimated tax, the amount of tax payable, and how much tax you may be entitled to as a refund once your total tax and tax withheld are compared.

How Should You Treat Motor Vehicle and Travel Costs?

Motor vehicle expenses are deductible when you use the car for genuine business travel, such as visiting clients, attending jobs, or collecting stock and supplies. You generally cannot use these rules to claim ordinary trips between home and a regular workplace, because those are usually treated as private. To claim correctly, you need to decide which method suits your situation, such as a logbook or a cents‑per‑kilometre approach, and keep records for the whole income year. For the 2024–25 and 2025–26 income years, the ATO cents-per-kilometre rate is 88 cents per business kilometre, with a maximum claim of 5,000 kilometres per year.

Your claim can include fuel, servicing, insurance, registration, interest on finance, and depreciation, limited to the business‑use percentage. Getting this percentage right matters because it has a direct impact on your tax payable and your final refund or amount of tax still to pay. When a business owner asks, “How much tax can I save from my car?” the honest answer is that it depends on total income, the method used, and how accurately the business use is calculated.

What Can You Claim for a Home‑Based or Hybrid Business?

If you run your business from home or regularly work from home, you may be able to claim a reasonable portion of home running costs. This can include electricity, gas, internet, phone, and sometimes occupancy costs such as rent or mortgage interest if you have a dedicated work area. For the 2024–25 year, the ATO’s fixed rate method is 70 cents per hour worked from home, which covers some running costs such as electricity, gas, internet, and phone. The key is to use a method that reflects your actual use and is supported by records, such as hours worked at home or floor‑area percentages.

These home‑based deductions reduce your taxable income just like any other business expense, which in turn affects your income tax and the amount of tax payable for the year. While you cannot make your entire home tax free, carefully working out the business component can make a meaningful difference to your tax refund or the total tax you owe. If you have private hospital cover, higher education loan program debts, or a trade support loan, your total income and deductions will also influence related amounts such as the Medicare levy surcharge and compulsory repayments.

How Do Depreciation and Asset Write‑Off Affect Your Tax?

Larger items that last for several years, like equipment, machinery, and vehicles, are usually claimed over time through depreciation instead of an immediate full deduction. Small businesses with turnover under $10 million may be able to use instant asset write‑off thresholds (now confirmed as law until 30 June 2026) so that eligible assets costing less than $20,000 and first used or installed ready for use can be claimed in full in the year they are first used. This can significantly change your estimated tax for the financial year if you buy multiple assets.

These rules help align your tax position with the way you use assets in your business, but they must still be handled carefully. Each asset has a cost, a start date, and a method used, and these details affect how much deduction you claim each tax year. When you see a tax calculator or tax return calculator ask about assets, it is usually trying to estimate how these items will reduce your taxable income and therefore your total tax.

How Should You Handle Staff, Contractors, and Super Costs?

Most genuine staff costs, such as wages, salary, bonuses, and employer super contributions, are deductible when they relate to your business activities. These payments also link to your PAYG obligations, where tax is withheld from employee wages during the year and sent to the ATO. At tax time, the total income your staff receive and the tax withheld appear in their own returns, while your business claims the wage and super costs as deductions.

Payments to contractors can also be deductible, but you need to be careful that the arrangement is correctly set up and reported. Mixing salary sacrifice, fringe benefits, or lump sum bonuses without proper records can lead to confusion for both tax and super. Aligning your payroll, super, and contractor payments with your BAS and your year‑end tax return gives you a clearer view of your ongoing tax obligations and future cash flow.

Which Business Expenses are Commonly Overlooked or Under‑Claimed?

Many owners focus on big‑ticket items and forget smaller expenses that quietly add up across the year. Commonly missed deductions include software subscriptions, professional memberships, industry journals, and certain bank and merchant fees. These might be small on their own, but when you add them across a full tax year, they can noticeably lower your taxable income.

Another area often missed is the interest portion of business loans and overdrafts, which is usually deductible when the borrowing is used for business purposes. Some owners also overlook prepaid expenses, such as a year of insurance or software paid upfront, where some or all of the amounts may be claimed earlier depending on your business size and method. When you next ask yourself, “How much tax can I save?”, checking these smaller items can be as valuable as focusing on the obvious ones.

What Can You Definitely Not Claim as a Business Deduction?

Just as important as knowing what you can claim is knowing what you cannot. Private costs such as everyday clothing, personal travel, and home groceries remain non‑deductible even if you sometimes talk about work while doing them. Fines, penalties, and certain government charges are also generally not deductible and cannot be used to reduce your total tax.

You also need to be careful with entertainment and some client hospitality, as these may not be deductible even when they relate to business relationships. Trying to claim purely private expenses can lead to adjustments, extra tax payable, interest, and possibly penalties. Remember that your claim has to make sense if you looked at it from the point of view of an independent reviewer, and it must be consistent with your records, your total income, and the way your business operates.

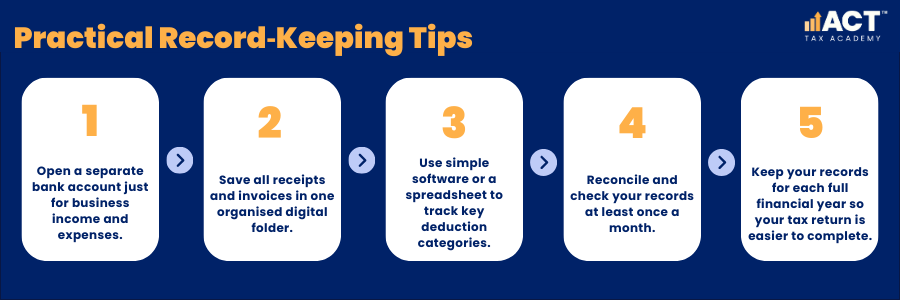

How Important Is Record Keeping for Maximising Deductions?

Good record keeping is at the heart of claiming all your business deductions and giving your tax agent accurate information. The ATO requires you to keep most business records for at least five years (though some records like employee records under Fair Work require seven years, and asset records must be kept until five years after disposal). Your invoices, receipts, contracts, bank statements, and payroll records tell the story of your income, expenses, tax paid, and tax withheld during the year. When those records are complete and organised, your tax return becomes a straightforward process rather than a stressful guessing game.

Digital systems make it much easier to keep track of your financial year as you go. For example, if you upload receipts when you pay bills and reconcile your account weekly, you do not need to rely on rough estimates later. Solid records also make it easier to check that your gross annual income, total income, and deductions line up with the information held by others, such as your employer or the ATO.tered tax agent is still the most reliable way to calculate your position and understand what you are truly entitled to claim.

How Can You Turn This into a Repeatable Tax‑Time Checklist?

Turning these ideas into a repeatable checklist helps you approach each income year with structure and calm. Before the end of each financial year, walk through your main deduction categories: day‑to‑day expenses, vehicles and travel, home‑based costs, assets and equipment, staff and contractors, and finance and insurance. This also makes it easier to use any online tax calculator or refund estimate tool, because you will know you have captured the main deductions before you look at calculator results.

Remember that any online calculator works on general Australian income tax rules and assumes some standard tax rates, offsets, and conditions. The estimate from a tax return calculator can be useful, but it will not fully reflect your individual circumstances, such as higher education loan program balances, trade support loan debts, private health insurance, or exemptions from Medicare levy surcharge. Your best result comes from combining a good checklist, accurate records, and personalised advice from a trusted, registered tax agent who understands your business.

Conclusion

By understanding which expenses are deductible, keeping clean records, and reviewing your position regularly, you can reduce your tax liability, stay on top of your tax obligations, and feel more confident about your financial decisions. If you would like help tailoring this checklist to your structure, tax system and goals, our team is ready to walk through the details with you and make tax one less thing you need to worry about.