Capital Gains Tax Basics for Australian Small Businesses: What Assets Are Affected and How to Calculate Your Liability

Capital Gains Tax Basics for Australian Small Businesses: What Assets Are Affected and How to Calculate Your Liability is all about understanding when you pay Capital Gains Tax and how much it may cost your business. Many small business owners only think about Capital Gains when they have already sold assets, such as an investment property or business equipment. The challenge is that your tax obligations arise in the same income year as the sale, and the Australian Taxation Office expects accurate reporting in your tax return.

What Assets are Affected by Capital Gains Tax for Small Businesses?

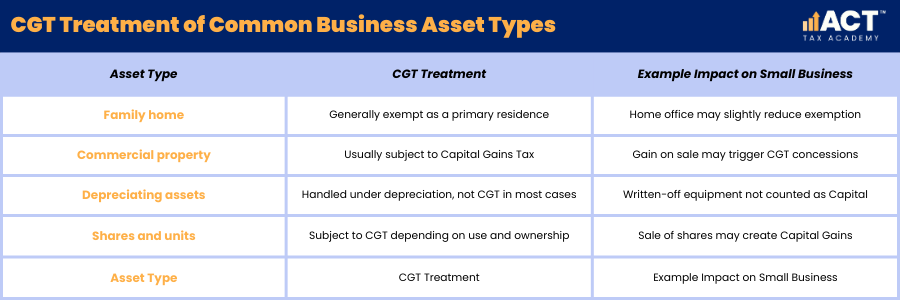

For Australian small businesses, Capital Gains Tax (CGT) generally applies when you sell or dispose of an asset for more money than its purchase price. Common business assets acquired that are subject to CGT include commercial property, business goodwill, shares, and some investments. If the market value at the time of sale is higher than your cost base, the difference is your Capital Gain or loss.

Which Assets are Exempt or Partly Exempt from CGT?

Not all assets acquired by your business are subject to gains tax, and some are fully or partly exempt. Your primary residence or family home is usually exempt from Capital Gains Tax, although business use may reduce this exemption. Certain personal-use assets below a threshold, and some assets acquired before the CGT start date, also fall outside the rules.

Depreciating business assets, such as tools or equipment where you claim a tax deduction through depreciation, are usually dealt with under other tax rules rather than CGT. Your primary residence may still attract a small taxable gain if a large part is used for business, so it is important to track how and when each asset is used. This is why we always encourage clients to seek expert advice before finalising a sale.

How Do You Calculate Capital Gains Tax Step by Step?

When calculating Capital Gains Tax, the basic formula is simple: Capital Gains amount equals sale proceeds minus the cost base. The cost base includes purchase price, certain fees, expenses, and incidental costs such as legal costs, stamp duty, and selling costs that relate directly to the asset. The remaining amount after subtracting the cost base from the sale proceeds is your Capital Gain before discounts and concessions.

What Is the Role of Net Capital Gain, Net Capital Loss, and Discounts?

Your net Capital Gain is the total of your Capital Gains for the financial year, minus any Capital losses, and then reduced by any applicable CGT discounts. This net Capital Gain is added to your taxable income and taxed at your normal tax rate as part of income tax. If your Capital losses exceed your Capital Gains, you will instead have a net Capital Loss that you can carry forward to offset gains in future years.

Where an asset has been owned for more than 12 months and you are an Australian resident individual or trust, you may be eligible for a 50 per cent CGT discount. Complying super funds receive a 33.33 per cent discount, while companies cannot access the CGT discount. Small businesses may also access further CGT discounts and concessions, which can greatly reduce or even remove the taxable gain. Foreign residents generally cannot access the 50 per cent CGT discount for assets acquired after 8 May 2012, though an apportioned discount may apply if there was a period of Australian residency. Residency is one of the key factors that affects your CGT outcome.

How Does CGT Apply to Business Property and Investment Property?

Many small businesses own property such as offices, warehouses, or an investment property used in the business. When these are sold, any profit over the purchase price (after adding related expenses) may trigger Capital Gains Tax. For rental properties, rent is generally income for tax purposes, while the gain when the property is sold is handled under CGT.

If the property has been held for more than a year, a CGT discount may apply, and some small business concessions may further reduce the remaining amount of Capital Gains that you must pay tax on. You may also be able to claim certain expenses as a tax deduction during ownership, which affects your account and tax planning but does not change the Capital Gains calculation itself. Keeping a clear record of purchase, costs, and improvements helps ensure the Capital Gains calculation is accurate.

How Do You Use a Capital Gains Tax Calculator Effectively?

A Capital Gains Tax calculator can be a helpful tool to estimate how much CGT you may need to pay when you sell an asset. These tools usually ask for the purchase price, sale price, cost base details, and ownership period to estimate your Capital Gains amount and potential tax. Remember that a calculator is only a guide and cannot fully adjust for all several factors, such as business concessions, complying super funds, or super funds and structures.

Many small business owners use online tools alongside the ATO website to support their planning and budgeting. At ACT Tax Academy, we often review calculator results and refine them with real figures and small business rules before including them in the tax return. This combination of tools and expert advice means you can make better informed decisions and avoid unexpected cash impacts.

How Do Small Business CGT Concessions Work in Practice?

Small business CGT concessions can significantly reduce the Capital Gains amount for eligible assets that are actively used in your trade or business. Depending on your turnover and the size of your business, these concessions can reduce your taxable gain, allow you to carry forward benefits into future years, or help you reinvest in new assets. They can even support your retirement planning by directing capital into complying super funds, with a lifetime CGT cap of $1,865,000 for the 15-year exemption and a $500,000 lifetime limit for the retirement exemption.

To access these concessions, your business must meet either the $2 million aggregated turnover test or the $6 million maximum net asset value test, plus satisfy the active asset test for the relevant asset. There are concessions that reduce the gain, allow you to defer it, or remove it entirely for tax purposes in certain situations. Because the rules are detailed and the taxation outcomes can vary depending on timing and structure, getting tailored support is essential.

What Is an Example of Calculating Capital Gains for a Small Business Asset?

Imagine a small Canberra business that acquired a piece of equipment for $60,000 including fees and incidental costs. Three years later, it is sold for $100,000, and there are $5,000 in selling expenses, bringing the effective sale proceeds to $95,000 after costs. In this case, the cost base is $60,000, and the Capital Gains amount before discounts is $35,000.

Because the asset has been owned for more than a year, the business owner, as an Australian resident, may qualify for a discount that reduces this Capital Gains figure for tax purposes. If they also have Capital losses from other investments in the same income year, these are applied before the discount to reduce the taxable gain. The result then flows into their taxable income and income tax at their standard tax rate, adjusting their final tax payable for that financial year.

How Do Residency and Super Funds Affect CGT?

Your status as an Australian resident or foreign resident affects how much CGT you may pay and whether you can claim certain CGT discounts. Foreign residents are subject to a 15 per cent withholding rate on property sales from 1 January 2025, which applies regardless of property value. This can influence your cash position at settlement. Residency also interacts with which income year the tax is assessed and how it appears in your tax return.

Some small business owners plan ahead by moving capital into complying super funds or other super funds as part of retirement plans. While super has its own rules, it can be a way to take advantage of small business CGT concessions and lower tax in future years. Because the outcome is shaped by several factors, including rules on inflation and tax rate changes, personalised planning is always recommended.

How Can ACT Tax Academy Help You Manage CGT?

Figuring out when you will pay Capital Gains Tax, how to work out your net Capital Gain, and how to use Capital losses and concessions is a lot to handle when you are running a business. Our team at ACT Tax Academy keeps the focus on clear explanations, real numbers, and simple steps so you know exactly how calculating Capital Gains Tax affects your income and tax obligations. We help you review each asset, check eligibility for discounts, and prepare your tax return correctly.

If you are planning to sell a business property, equipment, or other investments, now is the time to review your options, not after the CGT event happens. We can walk you through your records, work out your Capital Gains or net Capital Loss, and help you use the rules to your advantage without guesswork. Reach out to our friendly team so you can approach your next sale with confidence, clarity, and a plan that supports both your business and your long-term goals.