First 90 Days After Incorporation: Bookkeeping Priorities for a New Pty Ltd Before You Worry About Tax Returns

First 90 Days After Incorporation: Bookkeeping Priorities for a New Pty Ltd Before You Worry About Tax Returns is about getting your systems right so your numbers stay clear and reliable from day one. In those early months, your bookkeeping should support your new company structure as a separate legal entity, instead of leaving you guessing at your business finances. When the basics are in place, future BAS and tax returns are simply reports of good data, not stressful clean‑up jobs.

What Should You Do in the First 90 Days After Incorporation?

In the first 90 days after incorporation, your core focus is building simple bookkeeping habits that match your new legal status as a proprietary company. That means separating business finances from personal assets, choosing a bookkeeping system, and recording every transaction as soon as company trading begins. If you do this well, you support the company’s separate legal status and the limited liability generally available to shareholders. Directors still need to manage tax, superannuation and solvency obligations carefully, because personal liability can arise for unpaid Pay As You Go (PAYG) withholding, Goods and Services Tax (GST) and Superannuation Guarantee Charge.

Your new Pty Ltd company is a separate legal entity with its own Australian company number, Australian business number and company name. From day one, it takes on its own obligations and needs proper records of income, business expenses, assets and other obligations. Getting this right now makes later reporting for the financial year much easier, especially compared with sole traders who mix business and personal in one account.

Why Is Separating Business and Personal Money Non‑Negotiable?

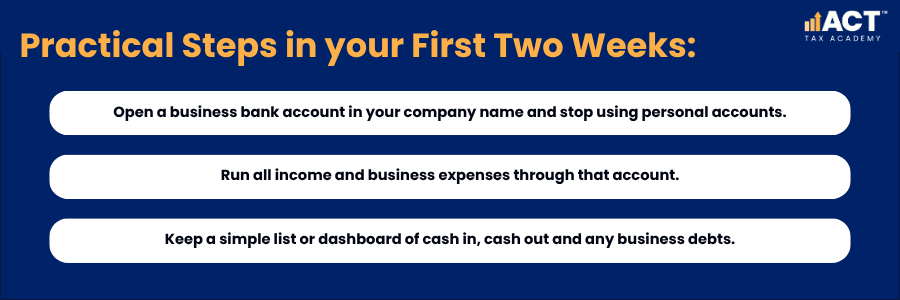

Separating business and personal money is critical because your new company is a separate legal entity. When you run all business finances through a dedicated account in the company’s name, it is easier to show that the company owns property, assets and debts in its own right. This supports the company’s separate legal status and helps preserve the limited liability generally available to shareholders. Directors should still manage tax, superannuation and company obligations carefully, because personal liability can arise in specific circumstances.

If you mix personal and business transactions, it becomes harder to show where the company ends, and you begin. That can create confusion about legal responsibility and financial responsibility, especially if there is ever a dispute about whether you are personally liable. Using one account for all company trading and business expenses makes it easier to track cash flow, pay suppliers and prove that the company is operating as its own legal entity.

How Do You Set Up Bookkeeping Software for a New Pty Ltd?

For a new proprietary limited company, cloud bookkeeping software is usually the best match for your business structure. It lets you record income, business expenses, assets, payroll and GST in one place and supports the legal requirements your company must meet under Australian laws. With a bank feed, you can easily match bank transactions to invoices and receipts, so your records stay current, and if you later add a trust with a bucket company, that same system can support the bookkeeping essentials for a bucket company as well.

Most small businesses and small proprietary companies benefit from simple features such as automatic bank feeds, easy invoicing, online payment options and basic reports. These tools give company directors clear visibility over share capital, cash flow and ongoing costs. They also make it easier to share information with your accountant or tax adviser so you can get tailored advice without digging through paperwork. When configuring your software:

- Create a small set of accounts for income, key business expenses and assets so reports stay readable.

- Turn on bank feeds for your company account so transactions flow in automatically.

- Set up invoices with your company name, Australian business number and payment terms.

What Record‑Keeping Does Your New Company Need from Day One?

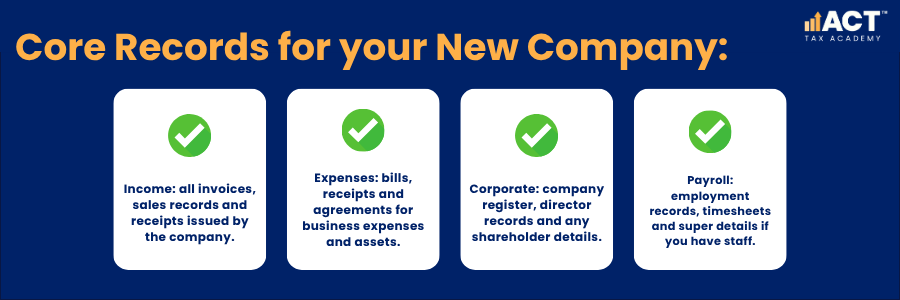

From the first day after incorporation, your proprietary limited company must keep records that explain its transactions, assets and obligations. For tax and superannuation purposes, most business records generally need to be kept for five years, and some records may need to be kept longer. These records support your compliance obligations under the Corporations Act 2001 and tax laws, and they help prove that the company is the legal entity carrying on the business. Proper records include invoices, receipts, bank statements, asset registers, agreements, Business Activity Statement (BAS records and reporting), GST records, payroll records, superannuation records, and contractor or supplier records where relevant, as well as the broader business tax return documents checklist you will need at year‑end.

Good record‑keeping is not just about avoiding penalties; it also shows that you, as a company director, are acting in the best interests of the company and meeting your legal responsibility. Clear records support decisions around ownership, transferring shares and raising capital in future. They also make it easier to show who owns what if your company owns property or other assets.

Why Does a Simple Compliance Calendar Matter More Than Early Tax Planning?

In the first 90 days, a simple compliance calendar should come before complex tax planning. Your company should still identify its tax, BAS, payroll and superannuation obligations from the start, so lodgements and payments are planned before they fall due, including how you would handle a late payment that triggers a Super Guarantee Charge (SGC) statement. Your new company has legal requirements to meet, including annual review fee payments, company updates, and tax‑related lodgements across the financial year. Missing these deadlines can create more stress than any early tax benefits you might gain.

A straightforward calendar that lines up with your company’s financial year helps you keep track of accounting, tax and corporate deadlines. It also respects your limited liability protection by supporting orderly management of the company’s obligations. When you know what is due and when, you are less likely to fall behind or overlook important filings that arise from your company’s legal status.

Key dates to map out early:

- Tax and BAS due dates based on your registration, reporting cycle and lodgement method.

- Company annual review due dates and any related fees.

- Regular payroll, PAYG withholding, superannuation and other recurring payments. From 1 July 2026, Payday Super will require employers to pay superannuation guarantee at the same time as salary and wages, so make sure your calendar reflects both superannuation due dates for employers and upcoming changes like the Super Guarantee rate increases through 2025.

How Should You Build a Weekly Bookkeeping Rhythm?

A simple weekly rhythm keeps your books in order and reduces the load at quarter‑end and year‑end. Even one focused hour a week can be enough for a small proprietary company in its early stages. That time allows you to reconcile bank transactions, send invoices, follow up unpaid amounts and file digital copies of receipts.

This habit supports your role as company director and helps you act in good faith as you manage the company’s money. It also helps you see whether the business is moving towards or away from its goals so you can make changes early. Compared with sole traders, who often try to catch up at year‑end, a Pty Ltd with a weekly habit tends to have more reliable reports and fewer surprises.ry to catch up at year‑end, a Pty Ltd with a weekly habit tends to have more reliable reports and fewer surprises.

How Does Your Company Structure Affect Your Liability and Finances?

Your choice of company structure has a direct impact on liability, ownership and how your bookkeeping works. A proprietary limited company is a separate legal entity, which means shareholders are generally protected by limited liability, and are not personally liable for the company’s debts beyond what they have agreed to contribute. This is a key difference from sole traders, who have full control but are fully liable for business debts and obligations.

Within company types, a proprietary company is the most common company type for small businesses, because it can have up to 50 non-employee shareholders and does not need to list on the Australian Stock Exchange. Small proprietary companies are usually simpler to run than large proprietary companies, which must meet extra reporting standards based on consolidated gross assets or consolidated revenue. There are other options, such as public companies, foreign companies and unlimited companies, but for most common business needs, a Pty Ltd is the most common type used.

Some key differences to keep in mind:

| Aspect | Proprietary Limited Company (Pty Ltd) | Sole Traders and Own Name |

|---|---|---|

| Legal Status | Separate legal entity | Individual person |

| Liability | Limited liability, generally protected | Personally liable |

| Ownership | Shareholders and share capital | One individual |

| Paperwork | More obligations but clear structure | Less paperwork, full control |

| Raising Funds | Can raise capital from shareholders | Limited to personal funds |

When Should You Actually Start Worrying About Tax Returns?

You should identify your first company tax return obligations from the start, even if detailed tax planning comes after your bookkeeping is consistent and your early lodgements are under control. Your focus in the first 90 days is on accurate records and smooth day‑to‑day operations. Once those are steady, you can look at how your numbers flow into the company income tax return and where genuine tax benefits may apply.

Most of your early tax outcomes depend on your profits, deductible business expenses and how money is paid to directors or shareholders, such as salary, dividends, reimbursements or loans. These choices should be reviewed before funds are taken from the company. With clean records and a clear view of the company’s position, you and your adviser can consider timing of purchases, funding decisions and other choices within the framework of the Corporations Act and tax rules. This approach respects both your legal requirements and your business goals.

What Next Steps Should a New Pty Ltd Take with ACT Tax Academy?

In your first 90 days, you do not need a complex structure or advanced strategies; you need steady, reliable systems. At ACT Tax Academy, we help small businesses choose and set up a company structure that suits their business needs and then build bookkeeping processes that match that structure. Our goal is to make sure your new Pty Ltd operates smoothly, meets its legal requirements and gives you clear, usable numbers.

We understand that different company types, from small proprietary companies to more complex structures, come with different obligations and ongoing costs. Our team can help you understand the key differences, keep your records in line with the Corporations Act 2001 and make day‑to‑day bookkeeping feel manageable. If you have just set up your proprietary limited company and want your first 90 days to support long‑term success, we would be glad to help you build a clear, practical plan.