Recording Outcome-Based Fees in Your Accounting Software to Support PSI Results Test Evidence

Recording outcome-based fees in your accounting software to support PSI results test evidence helps you show that you are paid to produce a specific result, not just for hours worked. When your records clearly link income received to completed items and a specific outcome, it becomes much easier to show that the PSI rules apply in your favour. This gives you more confidence when you self-assess your position and explain it to the ATO if needed.

Why Does the PSI Results Test Matter for Your Business?

If you earn Personal Services Income (PSI) as a sole trader or through a personal services entity, you need to understand when that income is considered PSI and how the PSI tests work. The results test looks at whether, for at least 75% of the individual’s PSI for the income year, you are paid to produce a specific result, required to provide the equipment or tools needed to do the work where applicable, and required to fix mistakes or defective work at your own cost.

If you pass the results test for at least 75% of the individual’s PSI for the income year, you can generally self-assess as a Personal Services Business (PSB) for that income year. This may mean the PSI deduction limits do not apply, although ordinary deduction rules and anti-avoidance provisions can still be relevant.

What Is the PSI Results Test and Why Does Outcome-Based Billing Matter?

The PSI results test looks at whether, for at least 75% of the individual’s PSI for the income year, all three ATO conditions are met: payment is for a specific result, the required tools or equipment are provided where applicable, and mistakes or defects must be fixed at your own cost. To pass the results test, your business contracts and working arrangements should show that you are paid to achieve a contractually specified result, provide the tools or equipment necessary to do the work where applicable, and are liable for the cost of rectifying defects in the work performed. If you pass the results test for the income year, you can generally self-assess as a PSB for that income year.

Outcome-based billing matters because it supports the idea that you are paid to produce, not just to attend your client’s premises and log hours worked. When income earned is tied to completed items or specific outcomes, your accounting records match the story told in your business contracts. This has a significant impact on whether income is considered PSI and how the PSI rules apply.

How Do the Main PSI Tests Work Together for Your Business?

There are several tests that can help you show you run a PSB rather than being limited by the PSI rules. These include the results test, unrelated clients test, employment test and business premises test. If you do not pass the results test, you must also meet the 80% rule before you can self-assess under the unrelated clients, employment or business premises tests. Together, these PSI tests look at how you provide services, how you obtain work, where you work, and whether you use other people to help produce results.

For many professionals, the results test is the most direct pathway, because passing the results test generally means your business is a PSB for that income year. If you do not pass the results test, you may still meet another PSB test, such as the unrelated clients test, employment test or business premises test, provided the 80% rule is also satisfied. Each test has specific ATO conditions that need to be checked. Thinking about your business structure, business assets and business premises can help you see which test best fits your situation.

How Does the Results Test Look at Payment, Tools and Fixing Mistakes?

To pass the results test, the income received needs to show three main features for at least 75% of the individual’s PSI for the income year. First, you must be paid to produce a specific result, such as delivering a report, completing an installation, or finishing a project. Second, you must provide the tools or equipment necessary to do the work where applicable, rather than relying on your client’s tools or equipment for the main work. Third, you must be required to fix mistakes or fix defects in defective work at your own cost.

Many professionals feel this lines up well with how they already provide services in practice. However, if your business contracts mainly use an hourly or daily rate, it may be harder to satisfy the results test because those payments are generally not linked to producing a specific result. Making your contracts clear about specific outcomes, the tools you provide and your duty to fix mistakes helps your records reflect the real nature of your personal efforts and personal skills.

How Do Other PSI Tests Such as Unrelated Clients and Business Premises Help?

Even if you do not pass the results test, you may still be able to show you run a personal services business through other tests. The unrelated clients test looks at whether you earn PSI from two or more unrelated clients in the financial year and whether the work was obtained as a direct result of making offers or invitations to the public or a section of the public, such as through advertising. This helps show that you are running a business and not just working mainly for one client, but you must also meet the 80% rule to self-assess under this test.

The business premises test looks at whether, at all times during the income year, you maintained and used business premises that were used mainly to gain or produce PSI, used exclusively by you, physically separate from your private premises, and physically separate from your clients’ premises. Keeping medical equipment, tools needed for your trade, or other business assets at separate premises may support your position only if the premises meet all ATO business premises test conditions. The employment test checks whether employees, contractors or other entities perform at least 20% by market value of the principal work, or whether you have one or more apprentices for at least half the income year.

What Should Your Business Contracts Say to Support the PSI Results Test?

Your business contracts should clearly say that you are paid to produce a specific result rather than only by an hourly rate or daily rate. They should describe the services and specific outcome you will deliver, the completed items that trigger payment, and who is required to fix mistakes or defective work. Clear wording makes it easier to later show that your income received is tied to a direct result.

The contracts should also cover who will provide the equipment, tools, business assets and trade inputs needed to complete the work performed. If you are expected to provide services with your own tools and fix defects at your own cost, that strongly supports the PSI results test. When business contracts meet these key points, your accounting software entries can mirror this language and build a clean evidence trail.

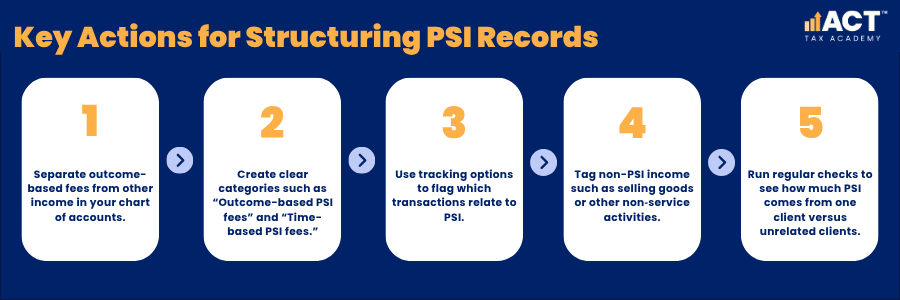

How Can You Structure Your Accounting Records for Outcome-Based PSI Income?

A good starting point is to separate outcome-based PSI fees from other income in your chart of accounts. For example, you might create income categories such as “Outcome-based PSI fees” and “Time-based PSI fees.” This makes it easier to assess the individual’s PSI and see what share of income earned relates to specific outcomes rather than an hourly or daily rate.

You can also set up tracking options that mark which transactions relate to PSI, and which are from selling goods or other business activities that are not considered PSI. Over time, this helps you self-assess whether you pass the results test or one of the other PSB tests, subject to the 80% rule where relevant. It also makes it easier to show what portion of your income comes from one client compared with unrelated clients.

How Should You Raise Invoices So They Support PSI Results Test Evidence?

When you raise invoices, focus on descriptions that show you produced a specific result or completed specific items, rather than just listing hours worked. For example, instead of “Consulting – 8 hours,” you might use “Fixed fee – completion of payroll setup” or “Stage 2 – system configuration completed.” This reinforces that you are paid to produce specific outcomes, not simply for time on site.

You should also link each line to the appropriate income category for personal services income. This allows you to clearly see which amounts relate to outcome-based fees. Over a financial year, your invoices will then form a clear pattern that supports your position if you pass the results test for at least 75% of the individual’s PSI.

How Do Reconciliations and Attachments Strengthen Your PSI Evidence?

Reconciling your bank transactions against the right invoices shows when you receive payment for outcome-based work. If your bank feed shows income received only after you deliver the specific result set out in the contract, that supports your PSI results test position. Clean reconciliations also make it easier to see which payments relate to outcome-based personal services and which relate to other parts of your business.

Most modern software gives you the option to attach documents to transactions or contacts. You can store signed contracts, project plans, and emails that confirm clients accepted your completed work. This is especially useful if there are unusual circumstances, variations or different outcomes compared to the original plan, because you can show how you managed those changes while still being required to fix mistakes or defects at your own cost.

How Can Your Reports Help You Self-Assess Your PSI Position?

Once your data is set up, your reports become a powerful way to self-assess whether the PSI rules apply and if you pass the results test. You can run income reports that show how much of your PSI is outcome-based versus time-based. You can also see how much you earned from one client and whether you have enough unrelated clients to meet that other test.

These reports help you understand whether you may need a PSB determination or further professional advice, especially if your situation is complex. They also support your deduction position because, if you are a PSB, the PSI deduction limits may not apply. Ordinary deduction, substantiation and reporting rules still need to be met.

What Do Practical Examples of Outcome-Based PSI Fee Recording Look Like?

Imagine a sole trader who provides services installing medical equipment for different clinics. Their contracts say they will install and test each unit for an agreed fixed fee, provide the necessary tools or equipment, and fix defects in their own work at their own cost. In their software, each invoice is raised on completion of each installation, showing the specific result and linking the payment to the outcome-based PSI income account.

Another example is a consultant who helps small business clients move to new accounting systems. They charge a fixed project fee split into milestones, such as “Data migration completed” and “Staff training delivered.” In this case, income earned is clearly tied to specific outcomes, not hours worked, and the consultant’s reports show that most income for the financial year comes from these outcome-based invoices rather than time-based billing.

How Does Good PSI Record-Keeping Support Your Long-Term Business?

Good record-keeping around PSI results test evidence does more than support ATO compliance. It helps you understand the market value of your services, review whether your pricing reflects the trade needed and tools needed and decide if your current business structure is right. It can also highlight when income splitting or working mainly for one client may create tax risk that needs professional advice.

By building strong systems, you reduce stress around compliance and free up time to focus on growing your business. Over time, this can strengthen your confidence when you self-assess, claim deductions, and explain your position if the ATO reviews how the PSI rules apply to your income.