How to Set Up a Partnership in Australia: Legal and Accounting Steps for Small Businesses

How to set up a partnership in Australia: legal and accounting steps for small businesses is a question many business partners ask when they decide to start a business venture together. A partnership structure is a simple, flexible business structure where two or more partners operate a business and agree how to share control, ownership, income, and the partnership’s profits. When you follow clear legal and accounting steps from the start, you reduce the risk of disputes, compliance errors and tax problems later. However, in a general partnership, each partner still has unlimited liability for the debts and obligations of the business.

What Is a Partnership Structure in Australia?

A partnership is a business structure made up of two or more people who carry on a business together with a view to profit and share the income between them. It is usually a general partnership, which means the partners jointly manage the business and are personally liable for partnership debts and obligations. The partnership is not a separate legal entity, so if the partnership cannot pay its debts, creditors can often seek payment from the personal assets of the partners.

There are other forms of partnership, such as a limited partnership and an incorporated limited partnership, which can offer limited liability to some partners in certain investment situations. In a limited partnership, limited partners invest money but do not take part in day-to-day management of the business, while general partners run the business and carry unlimited liability. Most small business partnership arrangements, including a typical family partnership, use a general partnership structure because it is easier and cheaper to establish and manage.

Why Does Choosing a Partnership Matter for Tax And Risk?

Choosing a partnership instead of a sole trader, company, or trust changes how you report income tax and who is responsible if things go wrong. Because the partnership is not a separate legal entity, the partners are usually equally responsible for the management of the business and may have unlimited liability for the debts and obligations of the partnership. This means one partner can create liability for the debts through decisions made on behalf of all the partners.

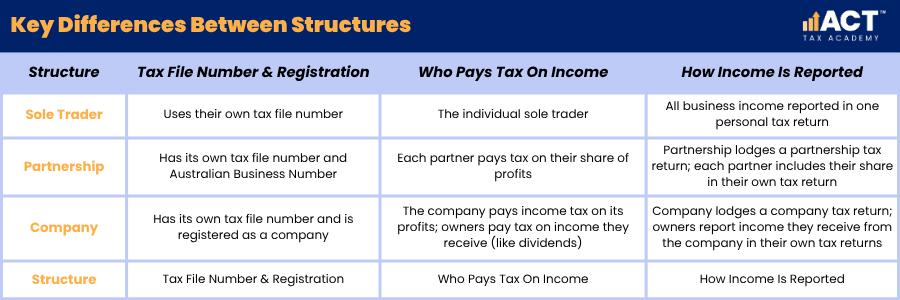

From a tax point of view, the partnership does not pay income tax on its profits in most cases. Instead, the partnership must lodge a partnership tax return that shows the income and expenses and how it will distribute income among the partners. Each partner pays tax on their share of the partnership’s profits by including it in their own tax return, along with any other income they earn.

How Does a Partnership Compare with Other Business Structures?

A partnership sits between a sole trader and a company in terms of cost, control, and risk. A sole trader runs the business alone and keeps full control, but also has full personal responsibility for all debts. A company is a separate legal entity, which can offer some limited liability protection, but it is more complex and more costly to set up and run.

In a partnership, partners share the management, responsibility, and profits, which can be helpful when the business needs different skills or a larger investment of money or assets. However, in a general partnership, all the partners can still be personally liable if the partnership cannot pay its debts. When deciding between a partnership and other business structures, it helps to consider your risk tolerance, long-term goals, and how you want to share control with other partners.

What Legal Steps Are Needed to Set Up a Partnership?

The first legal step is deciding who the business partners will be and what each person will bring to the business, such as money, assets, skills, or time. Partners should discuss and agree on core points like ownership percentages, decision-making processes, and how they will share the partnership’s profits and losses. It is also sensible to consider how you will bring in new partners or deal with a partner leaving before the business is fully established.

The Partnership Act in each state or territory sets out default rules about how partnerships operate, including how profits are shared and how decisions are made if there is no written partnership agreement. If you do not have a clear agreement, those default rules may apply even if they do not match what you thought was fair. Working with a lawyer to check your partnership agreement against the relevant Partnership Act helps ensure your arrangement is properly governed and reduces later disputes.

What Should Go in a Partnership Agreement?

A written partnership agreement is strongly recommended to set clear expectations and reduce the chance of conflict between partners. It should cover who owns what share of the business, how the partners will share income and losses, and who has authority to make which decisions. The agreement should also clarify how partners will handle day-to-day management, big spending decisions, and changes in the ownership of the partnership.

The agreement should explain how the partnership will distribute income, how much each partner can draw as regular payments, and how profits will be calculated at year end. It should also cover how to bring in new partners, what happens if a partner wants to leave, and how to deal with illness, death, or serious disagreements. Including clear rules on responsibility, control, and exit terms can help protect both the business and personal relationships.

How Do You Choose and Register a Business Name?

Partners must decide whether to trade under the partners’ personal names or use a separate business name. If you trade only under the partners personal names, you may not need to register a business name, but this can limit branding options. If you choose a business name that is not all partners’ personal names, it generally must be registered with ASIC so customers, suppliers and the public can identify the business name holder on the register.

Before registering, you should check that the business name is available and does not conflict with other registered names or trademarks. Registration is done online and usually requires the partnership’s Australian Business Number and details of all the partners. Once the name is registered, you can use it on your page, website, invoices, and other business documents so that the partnership looks consistent and professional.

What Tax Registrations and Numbers Does a Partnership Need?

A partnership must apply for its own tax file number rather than using the tax file number of one partner. It also needs an Australian Business Number if it is carrying on an enterprise in Australia, which helps you register for taxes and deal with suppliers and customers. If your business has GST turnover of $75,000 or more, you must register for Goods and Services Tax (GST).

In some cases, the partnership will also need to register for pay as you go withholding if it has employees and will be paying wages. While the partnership itself does not usually pay income tax on profits, it does need to lodge a partnership tax return each year to report income and expenses. Each partner then uses information from the partnership to complete their own tax return and pay tax on their share of the profits.

What Are the Ongoing Tax and Reporting Obligations?

Each year, the partnership must lodge a partnership tax return that shows the income, expenses, and how profits are shared. This return does not usually result in the partnership itself having to pay income tax, but it is still required so the Australian Taxation Office can see how much income needs to be passed to each partner. Each individual or entity partner then includes their share of the partnership’s profits in their own tax return and pays tax on that amount along with other income.

The partnership may also need to lodge regular activity statements to report goods and services tax and any pay as you go withholding on wages, and understanding BAS due dates and reporting requirements helps avoid late lodgement penalties. Good record-keeping makes it easier to track income, control spending, and manage cash needed to pay tax and other obligations. With clear records, timely lodgements, and targeted accounting and bookkeeping training, you can reduce the risk of penalties and keep your business running smoothly.

Key Tax Responsibilities

- Keep most business tax and super records for at least 5 years, and longer where the law requires.

- Lodge the annual partnership tax return by the due date.

- Ensure each partner includes their share of profits or losses in their own tax return.

- Report goods and services tax and pay it by the required deadlines.

- Meet pay as you go withholding and super obligations for employees.

How Should You Set Up Banking, Accounting, and Bookkeeping?

A partnership should open a separate bank account in the partnership’s name so that business money is not mixed with personal money. This helps you track income and spending clearly and shows the Australian Taxation Office that the partnership is run in an organised way. The bank account should be linked to the partnership’s Australian Business Number and used for all business income and expenses.

Using simple, cloud-based accounting software can make it easier to manage goods and services tax, choose between accrual and cash accounting methods, track who owes money, and prepare reports for partners. The accounting setup should reflect how the partners have agreed to distribute income, including drawings during the year and final profit shares after the accounts are prepared. Regular bookkeeping and review meetings, supported by a solid understanding of basic bookkeeping for small business, give partners better control over the management of the business and help them make informed decisions about investment and growth.

How Can Professional Advice Help You Set Up a Partnership the Right Way?

Working with a lawyer and an accountant makes it easier to set up a partnership that matches your goals and protects you as much as possible. A lawyer can prepare or review your partnership agreement, so it is clear, fair, and consistent with the Partnership Act and other relevant laws. An accountant can guide you on the best way to distribute income, minimise surprises at tax time, and meet your obligations to the Australian Taxation Office.

Professional advice also helps you compare a partnership with other business structures such as a company or trust. You can talk through how much control you want, how comfortable you are with risk, and what kind of growth or investment you expect in the future. With the right advice and a well-established structure, you can focus on running the business while knowing your responsibilities and obligations are under control.