What Is the Minimum Tax Threshold in Australia? A Guide for Small Business Owners

What Is the Minimum Tax Threshold in Australia? A Guide for Small Business Owners is ultimately about understanding when your taxable income crosses the line where you start to pay tax and must lodge a tax return. For small business owners, this minimum tax threshold is not just one number but a combination of thresholds, tax brackets, and income tax rates that apply to different structures. If you run a business in Australia, knowing where you sit on these scales directly affects your tax payable, take-home pay, and cash flow.

The tax-free threshold for most Australian resident individuals is $18,200 per income year. For 2025–26, resident rates remain: 16% from $18,201–$45,000, 30% from $45,001–$135,000, 37% from $135,001–$190,000, and 45% above $190,000. For small business owners, these numbers interact with business profits, wages, salary, and other income to determine how much tax you actually pay.

What Is the Minimum Tax Threshold for Individuals in Australia?

For Australian residents, the minimum tax threshold starts with the tax-free threshold of 0 – 18,200 of taxable income in a full financial year. If your taxable income is $18,200 or less for the full year, your income tax is nil. The Medicare levy is separate, but this sentence should not imply it commonly applies below the tax-free threshold. This basic rule applies whether you earn wages, operate a business as a sole trader, or have a mix of sources.

Once your income moves above 18,200, you start to pay income tax using the resident tax rates tables that show how your tax is calculated for each bracket. The tax rate increases as you move through the tax brackets, so the same income can result in a different tax payable depending on how much you earn in total. Even if the tax-free threshold applies to part of your income, the above rates still affect every extra dollar you earn.

How Does the Minimum Tax Threshold Apply to Sole Traders and Freelancers?

If you operate a business as a sole trader or freelancer, your taxable business profit is added to your other income, such as wages, salary or benefits, to work out your total taxable income. That combined figure is then run through the same resident tax rates, so the minimum tax threshold still begins at 0 – 18,200. Even small jobs, wages from employment, or contract income earned under your own ABN can push your total taxable income above the threshold once all income is added together.

This means you might think you are under the threshold based on your business income alone but still need to pay income tax once your other income is included. Because taxable income tax is calculated on your total figure, separate bank account records for business and personal transactions make it easier to check where you stand. Keeping clean records also helps you claim the right tax deductions for costs genuinely connected with earning your income, and to choose between accrual and cash accounting methods that align with your reporting obligations.

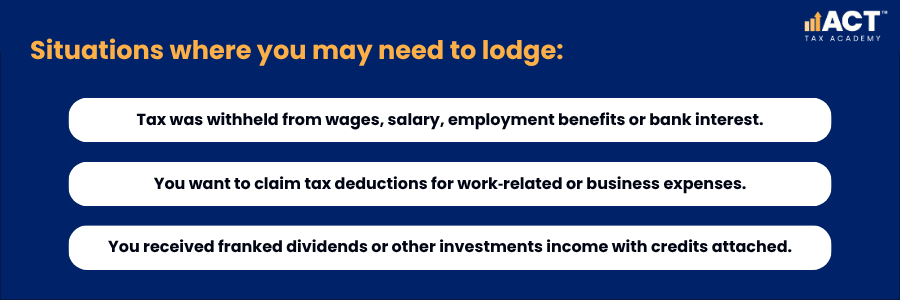

What Is the Minimum Income Before a Tax Return Must Be Lodged?

The minimum tax threshold and the minimum income for lodging a tax return are related but not always the same thing. For sole traders and other businesses, lodging is not determined only by the $18,200 threshold. If you carried on a business, you generally need to lodge a tax return even if the business made no income, and in many cases, you’ll also need to calculate and report Goods and Services Tax (GST) correctly. If you do not need to lodge, you should submit a non-lodgment advice.

There are also situations where you may be entitled to refunds, credits or benefits that only show up when you lodge. This can apply if you have contributions to superannuation you could claim, if you received allowances from your employer, or if you had investments and other income with tax already withheld, including franked dividends and attached franking credits. In these cases, not lodging a return can mean leaving money on the table.

How Do Company and Trust Thresholds Differ from Individual Thresholds?

Companies do not get the individual tax-free threshold. For 2025–26, base rate entities generally use 25%, and other companies use 30%. Trusts are different: the trustee lodges the return, but the trust itself generally doesn’t pay income tax; beneficiaries are usually assessed on their share, with the trustee paying in some cases.

This means that once your company earns profit, the business is subject to tax at the applicable rate regardless of whether your personal income is still under the individual threshold. Later, when that money is paid out to you as dividends, it interacts with your own resident tax rates and thresholds again. Getting professional advice can help you compare the overall tax payable between running as a sole trader and using a company or trust.

How Do Tax Brackets and Tax Cuts Impact the Minimum Threshold?

The minimum tax threshold sits within a broader system of tax brackets and tax cuts that shape how much tax you pay at different levels of income. From 1 July 2024, Australia moved to the current resident tax rates and thresholds. As at 25 March 2026, those rates still apply for 2025–26, but further legislated tax cuts begin on 1 July 2026, when the 16% rate drops to 15%, and again on 1 July 2027, when it drops to 14%. Replace ‘by June 2025’ with ‘before 30 June 2026’ if publishing now.

As a small business owner, these changes influence how extra income from your business is taxed, even though the minimum tax threshold stays the same. The above rates can reduce the average tax rate on the same income compared with earlier years, improving your take home pay. Keeping an eye on new laws coming in from 1 July and by June 2025 helps you plan how much tax to set aside and to time any asset sales so you can use small business CGT concessions effectively, including more advanced capital gains tax concession strategies when you exit or restructure your business.

How Do Medicare Levy and Medicare Levy Surcharge Fit In?

On top of income tax, Australian residents may also pay the Medicare levy, which is generally 2% of taxable income once you pass certain thresholds. Low-income earners may pay a reduced levy or none at all, especially if their income is around or below the minimum tax threshold. This means that even when income tax is nil, there may still be a small levy amount if the relevant threshold is exceeded, especially if you also claim work-from-home and home office deductions that interact with your final taxable income.

There is also the Medicare levy surcharge, which can apply to high income resident taxpayers who do not hold adequate private health insurance for themselves and their family. This surcharge is separate from the basic levy and uses its own income thresholds to decide who is subject to the extra amount. For many business owners, reviewing health insurance is part of managing total tax payable, not just medical cover.

How Can Small Business Owners Use Thresholds and Deductions to Reduce Tax Legally?

Understanding the minimum tax threshold and related thresholds allows you to plan your year rather than reacting after 30 June 2025 or another end date. For example, if your business is having a strong year and you can see your income moving into a higher bracket, you might bring forward some deduction opportunities. This could mean paying certain business expenses before July or making extra superannuation contributions where you are eligible to claim them.

At the same time, you can avoid overlooking smaller items that reduce taxable income, such as home‑based business costs, software subscriptions, and certain employment related tools you pay for yourself. By lowering your taxable income, you can reduce both income tax and associated levies, improving your overall take home pay, while keeping an eye on whether your wages push you over state and territory payroll tax thresholds. A balanced approach, supported by professional advice, helps ensure each deduction is justified and properly documented.

Why Does the Minimum Tax Threshold Still Matter If My Business Has Grown?

Even if your business has grown well beyond the minimum tax threshold, it remains a useful reference point for planning and decision making. In a slower year or during expansion, your taxable income could fall back close to the threshold, changing how much tax is payable and whether levies or surcharges apply. It also matters if family members working in the business have lower incomes, as they may be closer to the basic tax-free threshold.

Keeping an eye on these base levels helps with choices about salary versus dividends, the timing of bonuses, and how much to pay yourself in wages compared with retaining funds in the business. You may also need to factor in payroll tax obligations for growing small businesses as total wages increase. Understanding how the formula for tax is calculated at each bracket means you can see the impact of each dollar of extra income, rather than guessing. In short, the minimum tax threshold is a starting point that continues to influence your planning even as your business grows.

Conclusion

For small business owners in Australia, the minimum tax threshold is not just a single figure but part of a broader system of thresholds, brackets, levies and deductions that shape your taxable income tax outcome. Knowing how the 0 – 18,200 tax free threshold links to the higher brackets, Medicare levy and surcharge, and the way company and trust profits are taxed gives you a clearer view of your total tax picture. When you can see how everything fits together on one page, tax becomes less complex and more manageable.

The next practical step is to review your latest financial year figures, including business profit, wages, investments and other income, and map them against the current resident tax rates tables. From there, consider where targeted tax deductions and planning opportunities might reduce your tax payable without risking errors or excess claims. Working with a trusted tax professional ensures your approach is tailored to your situation, keeping you compliant while protecting more of your hard‑earned money.