Understanding Australian Marginal Tax Rates: A Visual Guide for Small Business Owners

Understanding Australian marginal tax rates: a visual guide for small business owners helps you make sense of how much tax you actually pay on every extra dollar you earn. Many small business owners in Australia feel confused when their taxable income grows, their income rises, and yet their total tax bill jumps more than expected. This guide explains how marginal tax rates work in a clear, practical way so you can plan ahead with confidence.

What Is a Marginal Tax Rate and Why Does It Matter?

A marginal tax rate is the percentage of tax you pay on your next dollar earned, not on every dollar of your taxable income. Under Australia’s progressive tax system, different marginal tax rates apply to different bands of income, so you only pay the higher rate on just the portion that falls in that band. This means your marginal rate is usually higher than your overall effective tax rate.

For small business owners, this matters because the marginal rate affects how much tax you pay when your income rises. If your business has a good year, your extra money may fall into a new bracket with a higher rate, but only that new portion is taxed at the higher rate. Understanding this difference helps you calculate the actual tax on your income and avoid worrying that all your income is suddenly taxed at the same rate.

How Do Australian Marginal Tax Brackets and Thresholds Work in 2024–25 and 2025–26?

For Australian residents, income tax rates for the 2024–25 and 2025–26 income year use the same key thresholds. The 0–18,200 band is the tax-free threshold, where you do not pay tax at all. From 18,201–45,000, the tax is 4,288 plus 30c for each 1 over 45,000 for certain brackets, and higher bands include amounts like 31,288 plus 37c and 51,638 plus 45c depending on the taxable income level and brackets such as 1 over 190,000.

What matters is that these above rates show how marginal tax rates work on slices of income within each band. When your income moves into a new bracket, you pay more tax only on the portion in that new bracket, not on all of your taxable income. This structure helps taxpayers see that marginal tax is about the last dollar, not every dollar.

How Do Marginal Tax Rates Affect Small Business Owners’ Personal Income?

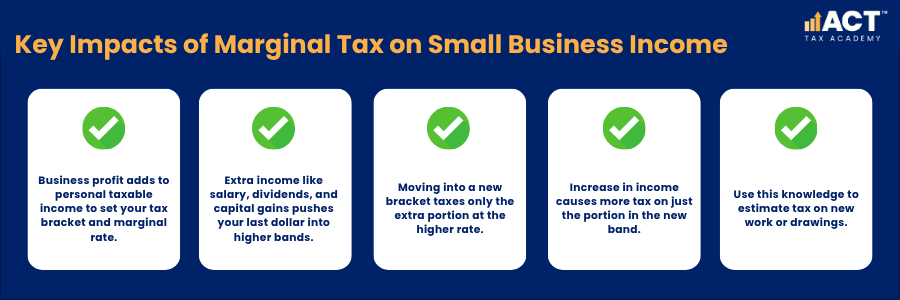

If you operate as a sole trader or partner, your business income is part of your personal taxable income for tax purposes. That means your business profit, salary from any job, dividends, and even capital gains from selling assets all sit together to determine your tax bracket and marginal rate. The more income you add, the more likely your last dollar earned will fall into a higher rate band.

For example, if your taxable income moves from the 18,201–45,000 band into the next band, your marginal rate increases, but your earlier income still benefits from the lower rates. This explains why an increase in income can cause more tax on the extra portion without changing the tax you already paid on the lower bands. Knowing this helps you estimate how much tax you will pay when you quote new work or consider increasing your drawings.

How Do Company Tax Rates and Individual Marginal Tax Interact?

Companies do not use marginal tax brackets; instead, they generally pay a flat company tax rate based on the type of entity, alongside separate obligations such as calculating and reporting GST. Many small companies that meet certain conditions pay tax at a lower base rate, while others pay at a higher standard rate. This means company profit is taxed differently from an individual’s progressive tax.

When you later take money out of the company as dividends, the tax paid by the company is often passed to you as franking credits on franked dividends. These credits can reduce the tax payable in your personal return, so your total tax outcome depends on both company tax and your individual marginal rate. This mix of company tax, franking credits, and personal marginal tax can be very effective for business owners once profits reach higher levels.

What Role Do the Medicare Levy and Medicare Levy Surcharge Play?

On top of income tax rates, most Australian residents pay a Medicare levy of 2 per cent of their taxable income once they earn above certain thresholds. The levy helps fund the public health system and is calculated separately from your marginal tax, though it increases your total tax. Some taxpayers on lower incomes receive reductions or may not pay the full levy.

If you do not have an appropriate level of private hospital cover and your income exceeds certain thresholds, you may also pay a Medicare levy surcharge. This extra charge can apply even if your main tax is modest, especially if your income rises due to a good business year or capital gains. Understanding how the levy and surcharge affect your total tax helps you calculate how much tax you pay overall, not just from the main brackets.

How Do Tax Offsets, Deductions and Entitlements Affect Your Actual Tax?

Tax offsets and tax deductions you can claim can have a big impact on your total tax, even if your marginal rate is high. Deductions, such as work-related expenses, business costs, and some types of super contributions, reduce your taxable income before tax rates are applied. Tax offsets reduce the tax payable after the rates are applied, which can lower your effective tax rate.

Common tax offsets include low-income tax offsets and other entitlements that apply to certain taxpayers. If you have children, investments, or particular types of income, you may have access to additional offsets or credits that change how much tax you pay. This is why two people with the same taxable income can still pay different total tax depending on their offsets, deductions, and entitlements.

How Does Timing Income and Deductions Help Manage Marginal Tax?

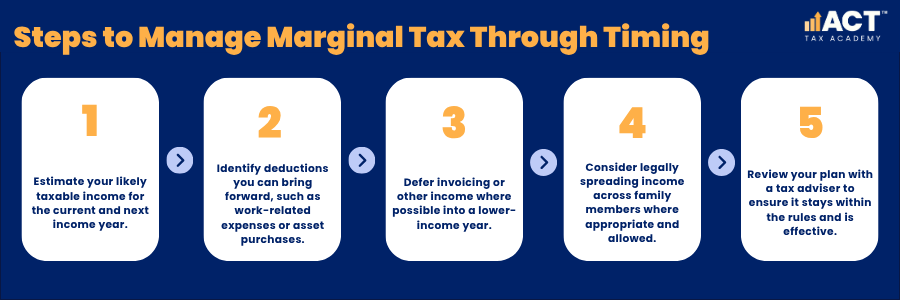

Because marginal tax rates apply to your last dollar, the timing of income and deductions and using PAYG instalments to smooth tax payments can make a real difference. If you expect your income to be much higher in the next income year, you might bring forward deductions, such as work-related expenses or small business asset purchases, to reduce this year’s taxable income. If you expect lower income next year, you might defer income where possible, so that extra amounts fall into a lower bracket later.

This approach is sometimes called managing or diverting income in a lawful way, such as delaying invoicing or spreading income across family members where the law allows. The key is to move income away from years where your marginal rate is high and towards years where your rate is lower, while always staying within the rules. Done properly with advice, this can reduce total tax without affecting the money your business receives over time.

How Do Marginal Tax Concepts Apply to Capital Gains and Investments?

Capital gains, such as profit from selling shares or property, are generally added to your other income for tax purposes, and understanding Capital Gains Tax in Australia is crucial when planning these transactions. This can push your last dollar into a higher tax bracket for the income year in which you sell the asset. However, if you hold certain assets for at least 12 months and you are an individual, you may receive a discount on the taxable portion of the gain.

Because capital gains are added on top of your other income, they can move you into a new bracket where you pay a higher rate on that portion. Planning the timing of large capital gains can help you avoid adding a gain in a year when your business income is already high. Managing the timing can reduce the effective tax rate on the gain and on your total income for that year.

How Do Residents and Foreign Residents Differ for Marginal Tax?

Australian residents and foreign residents do not always share the same rate structure or thresholds. For many brackets, residents benefit from the 0–18,200 tax free threshold, while foreign residents may start paying tax from the first dollar of income earned in Australia. This difference means residents often pay less tax on the same income level than foreign residents.

For business owners who move to or from Australia, or who have income from overseas, it is important to know which rules apply for tax purposes and to avoid common tax return mistakes when reporting this income. Different withholding rules, credits, and treaty rules can change the total tax on income from foreign sources. Getting advice early can help make sure you do not pay more tax than required when your situation changes.

How Can Small Business Owners Use Examples to Check Their Own Situation?

Using simple examples can help you calculate how marginal tax rates affect you in real life, especially when you compare different reporting methods such as accrual versus cash accounting. For instance, if your taxable income is 46,000, only the dollar over 45,000 sits in the higher tax bracket: the rest benefits from the lower band. That extra dollar earns plus 30c in tax for each 1 over that threshold, but the earlier bands still enjoy the lower rates.

Likewise, when you see amounts such as 31,288 plus 37c or 51,638 plus 45c in the tax tables, remember these describe how much tax applies to income above specific thresholds. The plus 37c or plus 45c parts show how much tax you pay on each 1 above those levels, not on every dollar. With this in mind, you can better estimate how a salary increases, a strong business year, or an unexpected capital gain will affect your tax and how rising wages might interact with state payroll tax thresholds.

Conclusion

Understanding how marginal tax rates work gives you a clear picture of how much tax is payable on your last dollar and your total income. When you know the tax-free threshold, how the brackets operate, and how the Medicare levy and offsets interact with your taxable income, you can make better decisions for your business and family. This includes deciding when to take income, how to structure your business, and which deductions and entitlements you may claim.

No two taxpayers are exactly the same, even if they sit in the same bracket, because credits, offsets, deductions, and structures all affect the final outcome. If you want practical guidance tailored to your own income, business, and children or family needs, it is worth seeking personal advice. With the right support, you can use Australia’s progressive tax system to manage your tax, support your goals, and keep more money working for your business.