How Marginal Tax Rates Affect Your Take-Home Pay as a Small Business Owner

How marginal tax rates affect your take-home pay as a small business owner comes down to how each extra dollar earned is taxed under the Australian income tax system. We know it can feel overwhelming when you just want to run your business and see more money in your bank account. Our goal is to turn the complex tax rules into simple, practical guidance you can use.

This matters because your taxable income, deductions, tax offsets and the Medicare levy all change how much tax you pay across the income year. When you understand how your tax payable is calculated, you can make better decisions about wages, salary, drawings and dividends. That means more control over your total income and fewer surprises at tax time.

What Are Marginal Tax Rates for Small Business Owners?

Marginal tax rates are the different tax rates that apply to each extra dollar earned in each bracket of taxable income. Australia uses a progressive tax system, which means taxpayers on higher incomes pay tax at higher rates on the income above each threshold, not on every dollar. You never pay the highest rate on your entire income, only on the excess above that bracket.

If you operate as a sole trader with an ABN, your business profit is added to any other income such as wages or dividends to form your assessable income. Tax is then calculated on that total based on the relevant tax rates, the tax-free threshold and any applicable tax offsets such as the low-income tax offset. Knowing this helps you answer the question “how much tax will I pay?” with far more confidence.

How Do Marginal Tax Rates Affect Take-Home Pay?

Marginal tax affects your take-home pay because each extra dollar earned can fall into a higher rate once your income passes a new threshold. This does not mean all of your income is taxed at that higher rate, but it does reduce how much of that extra pay you get to keep. Many small business owners feel the cost of moving into a higher bracket without understanding how the total tax is calculated.

For example, if your taxable income increases from $80,000 to $90,000, only that extra $10,000 is taxed at the higher rate for that bracket. Your income tax and Medicare levy are then added together to determine the total tax payable for the income year. Using a simple calculator or working closely with our accounting team can make these numbers much easier to understand.

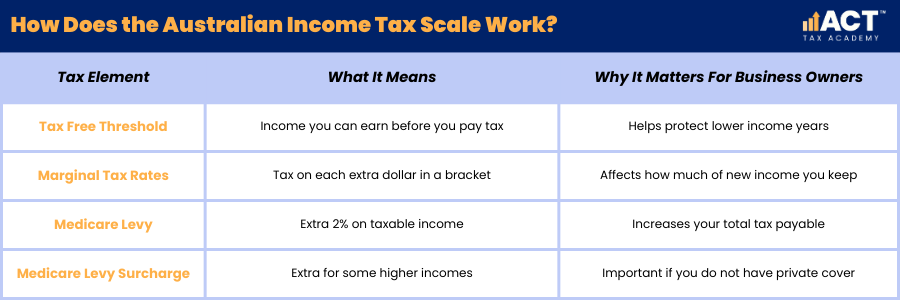

How Does the Australian Income Tax Scale Work?

The Australian income tax scale is based on a set of brackets that apply different rates to different levels of taxable income. Australian residents receive a tax free threshold at the bottom of the scale, which means they do not pay tax on a certain amount of income. As income rises, above rates apply to the extra income through higher brackets.

For individuals, the tax is calculated by applying each rate to the portion of income that sits within each bracket. On top of that, a Medicare levy of 2 per cent usually applies to most residents, and there may be a Medicare levy surcharge for some higher incomes without private health cover. Once these are added together, you see the total tax that applies to your total income.

How Do Business Structures Change the Tax You Pay?

Your business structure changes which tax rates apply and how your tax is calculated. As a sole trader or in a partnership, you pay income tax on your share of the assessable income using individual marginal tax rates. As a company, the business pays tax at a flat company rate, and you then pay tax only on the wages or dividends you receive.

When a company pays dividends, those payments may come with franking credits, which act like credits for tax already paid by the company. These credits can reduce the extra tax you would otherwise pay on that income as an individual. This means, for higher incomes, a company can sometimes lead to a lower average tax rate across the income year compared to staying as a sole trader.

How Does the Medicare Levy and Surcharge Affect Your Tax?

Most Australian residents pay the Medicare levy on top of their income tax to support the public health system. The standard levy is a Medicare levy of 2 per cent of taxable income, and it is added to the total tax payable after your income tax is calculated. For individuals earning over $101,000 (or families over $202,000) who do not hold appropriate private hospital cover, a Medicare levy surcharge of between 1% and 1.5% may also apply.

These amounts can be easy to overlook when you focus only on the main tax rates and brackets. For example, if your taxable income is $120,000, including compulsory super paid at the current Super Guarantee rate, the levy alone adds $2,400 to the cost of tax for that year. When we work with you, we make sure these amounts are included in your planning, so they do not surprise you as an extra debt.

How Do Deductions and Work-Related Expenses Help?

Deductions reduce your taxable income, which means less income falls into the higher brackets and you pay less tax on each dollar. Typical deductions for small business owners include work related expenses, tools, equipment, business vehicle costs, home office costs, and other business running costs. These amounts are subtracted before tax is calculated, so even a small change can have a real benefit.

For example, if you are on a higher rate and you claim an extra $5,000 in valid deductions, the tax saved on that amount can be significant. Good record keeping and simple accounting processes make it much easier to claim what you are entitled to without stress. We help you identify applicable deductions so you can reduce your tax in a way that is both safe and effective.

How Do Capital Gains and Dividends Influence Taxable Income?

Capital gains arise when you sell an asset such as property, shares or business equipment for more than its cost base. For individuals, these gains are added to assessable income,although individuals who hold an asset for more than 12 months may be eligible for a 50% capital gains discount, meaning only half the gain is added to assessable income. Even after any discount, the remaining amount still increases your taxable income and may push more of your income into a higher bracket.

Dividends from companies, including your own business if traded through a company, are also included in your total income. When those dividends carry franking credits, you get a credit against the tax that would otherwise be payable on that income, effectively preventing the same profit from being taxed twice. The result is that your additional income from dividends can be taxed more fairly, avoiding double tax on the same dollar earned.

How Can You Estimate How Much Tax You Will Pay?

To estimate how much tax you will pay, start by adding up your total income, including wages, salary, business profit, capital gains and dividends. Subtract your deductions and other allowable costs to arrive at your taxable income, then apply the applicable tax rates across the different brackets. Finally, add the Medicare levy and take away any tax offsets and credits, such as franking credits, to see the final total tax payable.

While an online calculator can give a quick average estimate, it may not capture all the details of your situation. Things like dependants, specific offsets, timing of income and special rules for certain types of income can all change the result. Our team can apply the rules correctly and show you a clear, easy-to-follow breakdown on a single page, so you know where every dollar goes.

What Is Bracket Creep and Why Does It Matter?

Bracket creep happens when your income slowly rises over time, but the tax brackets and thresholds do not move by the same amount. This means more of your income slips into higher brackets, and you pay tax at a higher rate on a larger portion of your income, even if your real buying power does not feel any higher. Small business owners often see this when their business grows and they draw more pay without revisiting their tax plan.

Over several years, bracket creep can noticeably increase your total tax without you realising why your refund is smaller or your payable balance is larger. Keeping an eye on your projected income through the year lets you see when you are close to crossing a new threshold. At that point, we can look at options such as additional super contributions, bringing forward expenses or adjusting when you earn income to manage the impact.

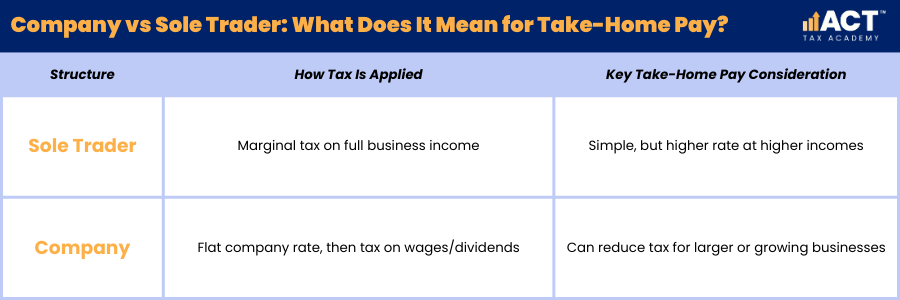

Company vs Sole Trader: What Does It Mean for Take-Home Pay?

As a sole trader, your business income is included directly in your taxable income, and the individual marginal tax rates apply to your full profit. As a company, the business pays tax at a flat rate of 25% (for base rate entities) or 30%, and then you decide how to pay money out to yourself through wages, salary or dividends. Those dividends may come with franking credits, which give you credits against your personal tax on that income.

For individuals on higher incomes, using a company structure can sometimes lead to less tax overall and more take-home pay once everything is added up. However, there are extra costs and responsibilities in running a company, so it is not always the right choice for everyone. We look at your income level, goals, family situation and long-term retirement targets such as how much super you might want by 40 before suggesting any change in structure.

What Practical Tips Help You Maximise Take-Home Pay?

There are practical steps you can take to protect and grow your take-home pay while staying fully compliant. First, keep good records so you can claim all applicable deductions and work related expenses without stress. Second, review your structure regularly to check that it still fits your income level and plans, rather than just sticking with what you started.

Third, look ahead before the end of each income year, not after, so you have time to apply strategies such as extra super contributions, timing of income and expenses, and making smart use of tax offsets. You can contribute up to $30,000 in concessional (before-tax) super contributions for 2025–26, including employer contributions, and these are taxed at just 15% inside the fund. Finally, do not be afraid to ask for help; talking through your numbers with a trusted advisor can often uncover simple tips and credits you did not know you could claim.