Main Residence Exemption for Capital Gains Tax: How It Works for Australian Small Business Owners

Main Residence Exemption for Capital Gains Tax: How It Works for Australian Small Business Owners is crucial if your home is also your workplace and you want to manage how much tax you pay when you eventually sell. Many property owners assume their main residence is always fully exempt from capital gains tax, but business use and rental income can change that. This article explains how the main residence exemption can apply in practice, especially where you run a business from home or use only part of the property to produce income.

What Is the Main Residence Exemption for Capital Gains Tax?

The main residence exemption is a rule that can make the capital gain on the sale of your home fully exempt from CGT if you meet certain conditions. In simple terms, if a dwelling is your main residence for most of the ownership period, is used mainly as your principal residence and is not used to produce income, you may not pay CGT when you sell. When you qualify for the main residence exemption, you may not even need to show the sale in your tax return.

To claim the main residence exemption, you usually need to be an Australian resident for tax purposes and actually live in the property as your main residence. Factors such as where your family live, where your personal belongings are kept and which address you use for important records can help show that a house is your principal place of residence. If you meet the eligibility conditions, the CGT event on sale may be fully exempt, and no net capital gain arises from that property.

How Does Using Your Home to Produce Income Change the Exemption?

Once you use your main residence to produce income, such as rent from a room or running a business from a dedicated area, the position changes. In many cases, only part of the main residence exemption will apply, and the property may only be partially exempt from CGT. This means you could pay tax on a proportion of the capital gain linked to the income‑producing use.

If you claim deductions for occupancy expenses, such as interest, rates or insurance for a room used as a place of business, that area is often treated differently for CGT purposes. In that case, you may move from a full main residence exemption to a partial exemption, and only part of the gain on that dwelling is exempt from CGT. Property owners who claim these deductions now need to understand what this might mean when they later sell the property and ensure they avoid common work-from-home deduction mistakes that could affect both their annual tax return and future CGT outcome.

How Does the Partial Main Residence Exemption Work in Practice?

A partial main residence exemption applies where only part of the property is treated as your main residence or where only part is used to produce income. The calculation usually looks at the proportion of the land or floor area used for income, the period it was used that way and the total ownership period. Only that proportion of the capital gain is subject to capital gains tax, with the balance covered by the main residence exemption.

For example, if you owned a house for ten years and used 20% of the floor area as a dedicated business space for five of those years, only part of the capital gain will be taxable, and you may also need to consider whether small business CGT concessions apply to the business-use portion. You would work out the gain from cost base to sale price, then apply the relevant proportion for business use over the ownership period. After that, you may apply any available CGT discount and capital loss to arrive at your net capital gain and the tax you will pay.

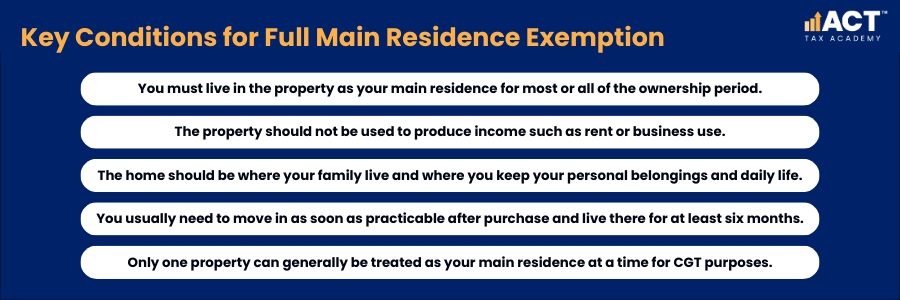

What Are the Eligibility Criteria for a Full Main Residence Exemption?

To qualify for the main residence exemption in full, you generally need to have lived in the property as your main residence for most or all of the ownership period. The property should not be used to produce income and should be the place where your family live, where your personal belongings are kept and where you carry on your day‑to‑day life. If these conditions are met and you sell, the capital gain may be fully exempt from CGT.

You usually need to move into the dwelling as soon as practicable after purchase and establish it as your principal residence. The rule applies differently where you own other property at the same time, because only one property can usually be treated as your main residence for CGT purposes. By checking the eligibility conditions early, you can decide whether the home is likely to attract a full exemption or only a partial exemption.

How Does the Six-Year Rule Help When You Move Out or Rent?

The six-year rule allows you to continue treating your former home as your main residence for up to six years after you stop living in it if it is used to produce income. This means you can move out, rent the house and still qualify for the main residence exemption when you sell, as long as you meet the conditions and the time limit. If the property is not used to produce income during your absence, you may continue treating it as your main residence indefinitely under the absence rules.

You cannot fully treat two properties as your main residence for the same period, so you may need to choose between your old home and your new home. The choice can affect how much CGT you pay on each property when you sell them. Getting advice when you start living in a new home or renting out the old home can help you use the six-year rule in a way that best fits your goals.

How Do You Work Out Capital Gain, Cost Base and Market Value?

When a CGT event happens, usually on the contract date of sale rather than the settlement date, you first work out your capital gain or capital loss, which in turn flows through to your business tax return and depends on whether you use accrual or cash accounting methods. You do this by comparing the sale price or market value against your cost base, which includes what you paid for the property plus buying costs and certain improvements. If the proceeds are higher than the cost base, you have a capital gain; if lower, you may have a capital loss.

For property, the cost base excludes amounts you have already claimed as tax deductions, such as capital works deductions, and this interacts with how depreciation schedules can drive tax deductions, which is an important detail for business owners and property investors. Once you know the capital gain, you apply any main residence exemption, partial main residence exemption, capital loss and CGT discount for property that you are eligible for. The result is your net capital gain, which is included in your assessable income and can affect how much tax you pay for that year, so understanding how capital gains tax works in Australia is essential for long‑term planning.

How Does the CGT Discount and Small Business Context Fit In?

If you are an individual and you have owned the property for more than 12 months, you may qualify for the 50% CGT discount on the taxable part of the gain. This discount applies after you have applied any main residence exemption or partial exemption and after offsetting any capital loss. For small business owners, this can significantly reduce the net capital gain and therefore the tax you pay, especially when combined with strategies for maximising small business CGT concessions.

Where the income‑producing area relates to your business, small business CGT concessions might apply in addition, but you still start with the main residence rules. Only the proportion of the dwelling used to produce income, and only for the relevant period, will be in the mix for those concessions. It is important to understand that the main residence exemption and small business relief are separate, and you should not assume you automatically get both.

What About Foreign Residents, Property Investors and Vacant Land?

Since 30 June 2020, foreign residents cannot claim the main residence exemption on Australian property unless they satisfy the life events test. This means foreign residents pay CGT on the full capital gain when they sell, with no residence exemption available. This can affect Australians who move overseas and later sell while treated as foreign residents for tax purposes, and it adds another layer to broader obligations such as fringe benefits tax (FBT) compliance and lodgment for those running businesses across borders.

Property investors who never live in the property generally cannot claim the main residence exemption and must pay CGT on any capital gain, subject to the general CGT discount rules and the way depreciation schedules for investment properties have been used to claim building and asset deductions over time. Vacant land may qualify in limited circumstances, usually where you build a new home and start living there within certain time frames. Understanding how these rules differ helps you see why your own residence and your investment property are treated differently for CGT purposes, and why some property investors may also need to consider how the GST margin scheme works when buying or selling certain types of real estate.

What Common Scenarios Affect Small Business Owners Working from Home?

Common scenarios include a sole trader using a study as an office, a consultant seeing clients at home or a tradesperson using part of the land for storage and admin. In these cases, only part of the property is used to produce income, so only part of any capital gain is likely to be taxable. The rest of the house and land, where you and your family live, may still qualify for the main residence exemption.

Another scenario is where you stop living in your old home, start living in a new home and rent the old home for a period, which may also bring GST obligations into focus if you run a business, making it important to understand GST calculation for Australian businesses. The six-year rule and the rule that only one property can be your main residence at a time become important here. Making the right choice about which property to treat as your main residence can change how much tax you pay CGT on when each property is eventually sold, and for some transactions you may also have to deal with GST residential withholding calculations at settlement.

How Can You Plan Ahead Before You Sell Your Home or Change Its Use?

Planning ahead means thinking about how current decisions will affect future tax outcomes when you sell your property. Before you claim business occupancy expenses, rent out a room or move to another dwelling, consider whether the lost main residence exemption is worth the extra deductions or income, and how it fits with your broader strategy for what to claim on your taxes. It can be better in some cases to keep the property fully exempt from CGT rather than claim every possible deduction now.

You should also keep clear records of when you start living in a home, when you stop living there, when you start using it to produce income and any changes to the way rooms are used, as well as how you manage PAYG instalments to avoid tax surprises linked to future capital gains. These details support your choice of main residence, your use of the six-year rule and how you work out the taxable proportion of any capital gain. With good records and early advice, you can often shape the outcome instead of being surprised by a tax bill later, including managing any GST withholding compliance obligations that arise on property sales linked to your business use of the home.

What Should Small Business Owners Do Next?

If your home is your main residence and you also use it for business, you are already dealing with rules that can affect your future CGT bill. Whether you are considering a sale, a move, new business use or renting out part of the property, the timing and the way you use the property will shape your access to the main residence exemption. It is easier to manage these issues before a CGT event happens than to fix them after the sale.

As a small business owner, your house, your business and your family plans are closely connected, so it makes sense to review them together. By understanding how the main residence exemption, partial exemption, CGT discount, six-year rule and eligibility criteria work, you can better protect the value you have built in your property. If you are thinking about selling, starting a home‑based business or changing how you use your property, now is the time to get tailored guidance so you only pay tax on the part you truly need to.