Taxable Income Explained: Is It Before or After Tax? A Guide for Australian Small Businesses

Taxable Income Explained: Is It Before or After Tax? A Guide for Australian Small Businesses is really about understanding how much tax your business is likely to pay in Australia in any given income year. Taxable income is the figure your income tax is calculated on, not your take home pay or profit after tax. When you know which numbers to use for tax purposes, you can plan for the tax you pay and avoid surprises at tax time.

What Does “Taxable Income” Actually Mean in Australia?

Taxable income is the amount the ATO uses to calculate the income tax you pay for the current financial year. It is generally your assessable income less any allowable deductions for business purposes. This amount of tax payable is then worked out by applying the relevant tax rates and any tax offsets or rebates that directly reduce the tax you pay.

Assessable income usually includes your gross income from business, other income such as capital gains from investments, and some government payments. Allowable deductions are business expenses incurred in earning that income, such as rent, wages, and operating costs. Think of taxable income as the starting point for every calculation of how much tax you can expect to pay.

Is Taxable Income Before or After Tax?

Taxable income is always a before tax figure. It is the amount your income tax is calculated on, not the money left after the tax you pay has been taken out. Once tax is worked out on your taxable income, you can see what is left as your after-tax profit or take home pay.

A simple way to think about it is: income first, then taxable income, then tax payable. You start with your income and other income, subtract your expenses and deductions, and what is left is taxable. Only after that is your tax calculated using the ATO tax rates and any relevant tax offsets.

How Do Gross Income, Net Profit and Taxable Income Differ?

Gross income is the total income your small business earns before any expenses, such as sales, fees, and other payments from customers. Net profit is the amount left after you subtract all business expenses incurred, such as wages, rent, and services. Taxable income adjusts this net result for tax purposes, by including assessable income and subtracting less any allowable deductions.

For example, some expenses may not be fully deductible in the income year you pay them, or some income may be treated differently, such as certain lump sum payments or capital gains. This means your net profit and taxable income can be different even if both start from the same gross income. Understanding these differences helps you read your accounts and estimate how much tax you are likely to pay.

What Counts as Assessable Income for Small Businesses?

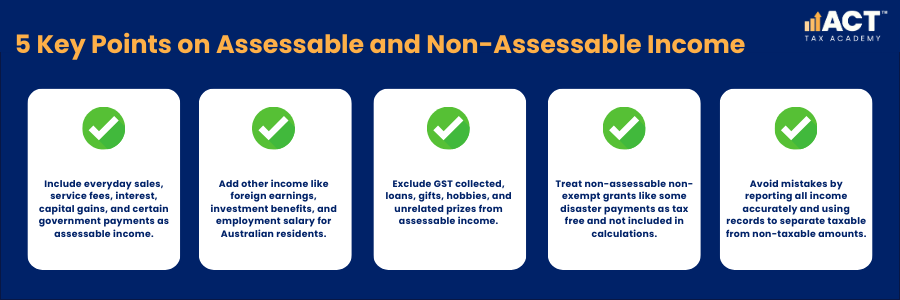

Assessable income covers most of the income your business earns during the financial year. This includes everyday sales, fees for services, interest from business bank accounts, and certain government payments received for business purposes. It also includes capital gains from selling business assets and some lump sum payments.

Some other income such as benefits from investments, foreign income, and payments from other work can also be assessable depending on your situation. For many small business owners who are Australian residents, employment salary from an employer and business income may both be included for tax purposes. This is why most taxpayers find it helpful to use an income tax calculator or tax calculator to estimate their total taxable income for the year. If you’re registered for GST, GST you collect isn’t part of your income for income tax, it’s reported separately via your BAS.

Which Amounts Are Not Taxable or Not Included?

Not every dollar that comes into your account is taxable. Some income can be tax free, such as certain government payments or other amounts that the rules say are exempt. If an amount is not assessable income, you generally don’t include it in your tax return, and it won’t form part of taxable income. Some payments are specifically treated as exempt or Non-Assessable Non-Exempt (NANE), so check the payment type to confirm treatment.

There are also items called non-assessable amounts which are not used for tax purposes. Even though these can affect your cash flow, they do not increase the amount of tax you pay. Knowing which payments are taxable and which are tax free helps you avoid paying too much tax and gives you a clearer picture of your money.

What Deductions Can a Small Business Claim Against Taxable Income?

Allowable deductions are expenses that you can claim to reduce your taxable income. These usually include expenses incurred for business purposes such as rent, utilities, wages, certain vehicle costs, and professional services like accounting. When you claim these deductions, they directly reduce the income figure used to calculate how much tax you pay.

Some deductions apply over time, such as depreciation of equipment, while others like charitable donations can reduce your taxable income in the income year you make them. You can only claim deductions for expenses that are genuinely related to earning assessable income and that do not exceed what is reasonable for your business. Keeping clear records of every dollar you spend on business expenses makes this part of the calculation much easier at tax time.

How Do Tax Rates Apply to Your Taxable Income?

Once your taxable income is calculated, the ATO applies tax rates that increase on a sliding scale for individuals, or flat rates for companies. For example, individuals and many other workers are taxed using income brackets, where a certain amount of income is tax free and higher amounts of income attract higher tax. Companies pay income tax at a flat rate, but the rate depends on the company. In Australia, companies generally pay 30%, or 25% if they qualify as a base rate entity.

On top of income tax, most Australian residents also pay a Medicare levy. If you (and your dependants) don’t have an appropriate level of private patient hospital cover, and your income for MLS purposes is above the thresholds, you may need to pay the Medicare levy surcharge. These amounts are added on to the income tax to reach the total tax payable for the year. Knowing where your taxable income sits within these brackets helps you estimate how much tax you will pay and whether any rebates, offsets or surcharges apply.

How Do the Tax-Free Threshold and Offsets Affect the Tax You Pay?

The tax-free threshold is the amount of income an individual can earn before they begin to pay income tax. For Australian residents, this threshold means that some income is tax free, and any income above that amount is taxed at the relevant tax rates. This concept is especially important if you run a small business as a sole trader or receive employment salary alongside business income.

Tax offsets and rebates directly reduce the tax you pay, rather than your taxable income. For example, certain tax offsets for low-income earners or small businesses can reduce the final tax payable by a certain amount of dollars. While offsets and the tax-free threshold can reduce how much tax you pay, they do not change the underlying taxable income figure that is used in the calculation.

How Do You Calculate Taxable Income Step-By-Step?

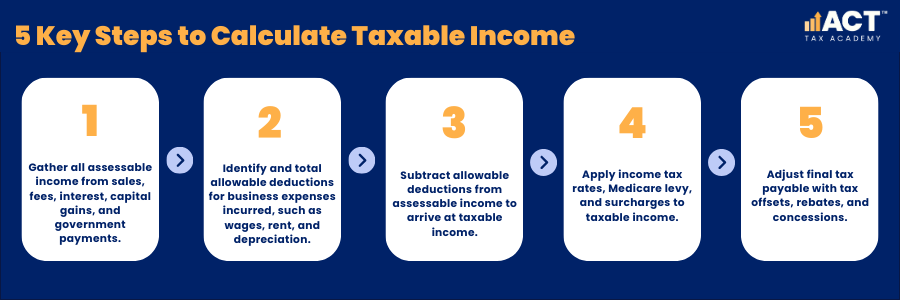

You can break the taxable income calculation into a few simple steps across the income year. This turns a complex topic into a repeatable process that you or your accountant can follow each financial year.

A basic step-by-step approach looks like this:

- The result is your taxable income, and your income tax and Medicare levy are then calculated on this amount, taking into account any offsets or rebates.

- Add up all assessable income for the year, including sales, fees, certain government payments, and other income such as interest or capital gains.

- Subtract allowable deductions, such as business expenses and depreciation, plus any other deductions you’re entitled to claim under the tax rules. For example, gifts are only deductible when they’re made to an eligible Deductible Gift Recipient (DGR) and you meet the conditions.

How Does Business Structure Change What “Taxable Income” Means?

Your business structure affects how taxable income is reported and who pays the tax. A sole trader includes business income with other income such as salary, and the total taxable income is taxed at individual rates. A company calculates its own taxable income and pays income tax as a separate entity.

Partnerships and trusts distribute income to partners or beneficiaries, who then include that share in their own tax return. In all cases, the basic idea is the same: assessable income less any allowable deductions gives taxable income, and the amount of tax is then calculated. Choosing the right structure can change the tax outcomes and also affect how profits, debt and benefits are shared or protected.

Practical Ways to Keep on Top of Your Taxable Income During the Year?

Keeping on top of taxable income is easier when you track it through the year instead of waiting until tax time. Simple tools, such as a basic tax calculator or income tax calculator, can help you estimate the tax you pay on your business income. Good records make every calculation faster and far more accurate.

Practical habits that help include:

- Talking to an accountant before 30 June to review deductions, lump sum payments, investments and other items that might affect your tax.

- Using bookkeeping software to track income, expenses and payments into and out of your business account.

- Reconciling your books monthly so you can see an estimate of taxable income and tax payable for the current financial year.

- Setting aside a certain amount regularly into a separate account to cover the tax you expect to pay on behalf of your business.

- Checking the ATO website for further information or using their calculator tools to test different income scenarios.

When Should You Seek Professional Advice About Taxable Income?

You should seek professional advice if you are unsure which payments to include as assessable income, which deductions you can claim, or how much tax you are likely to pay. This is especially important if your business has capital gains, multiple sources of income, or complex benefits such as private health insurance rebates or lump sum payments. A qualified adviser can walk through your numbers and help you use the rules in a way that suits your business.

Professional advice is also valuable if you want to make bigger decisions, such as changing your business structure, taking on debt, or investing in new equipment. In many cases, a short meeting can save you more money than it costs by helping you avoid errors and take up options you did not know about. You do not need to wait until tax time; advice mid‑year can be even more useful.

Conclusion: What Should Your Next Step Be?

Taxable income is the core figure that sits behind every amount of tax you pay, and it is always a before tax calculation built from your assessable income and deductions. Once you separate taxable income from gross income, net profit and take home pay, it becomes much easier to answer questions like “how much tax will I pay this year?”. With that clarity, you can use simple tools such as an income tax calculator and your own records to build a realistic estimate.

If you feel unsure about your own calculation or want to make sure you do not pay more tax than necessary, it is sensible to seek professional advice. Our team helps small business owners understand their taxable income, use deductions correctly, and plan ahead rather than react at tax time. With the right support, you can turn your tax calculation into a useful planning tool for your business instead of a yearly stress point.