How to Estimate Your Medicare Levy as an Australian Small Business Owner

How to estimate your Medicare Levy as an Australian small business owner starts with knowing that most Australian taxpayers pay the Medicare Levy as around 2% of their annual taxable income through their income tax return. As a small business owner, your levy is calculated on your total taxable income from all sources, regardless of whether you operate as a sole trader, company director, partner, or de facto couples running a family business. Understanding how the Medicare Levy is calculated, and when the Medicare Levy Surcharge (MLS) may apply, helps you plan how much tax to set aside so you are prepared at tax time.

The Medicare Levy helps fund Australia’s public health system and supports access to Medicare benefits when you or your family need medical care. The Australian Government, through the Australian Taxation Office, uses your income, family status and other personal circumstances to decide whether you pay the Medicare Levy in full, receive a Medicare Levy reduction, or qualify for a Medicare Levy exemption. Factoring the levy and any extra tax from the Medicare Levy Surcharge into your cash‑flow planning can make it easier to manage your tax bill without stress.

What Is the Medicare Levy and How Is It Calculated for Small Business Owners?

The Medicare Levy is a separate amount of tax that most Australian taxpayers pay on top of their normal income tax, and it is generally calculated as 2% of your annual taxable income. For small business owners, your annual taxable income usually includes business profit, wages includes any salary from a company, interest, dividends and other income, minus allowable deductions. The levy is worked out after you lodge your income tax return, but you can estimate it in advance by multiplying your expected annual taxable income by 0.02.

For example, if your annual taxable income as a single person is 90,000 AUD, your basic Medicare Levy estimate is 1,800 AUD for that financial year. If your income fluctuates, you can update this estimate during the year to reflect your current expected income, so you know how much tax to put aside. The key is to treat the Medicare Levy as a normal part of your tax, not an optional extra.

Why Does the Medicare Levy Matter for Your Cash Flow and Tax Planning?

If you are self‑employed, your employer withholds less tax or nothing at all from your business income, which means nobody is automatically setting aside money for the Medicare Levy. When your business is growing, this can lead to a nasty surprise if you only think about how much tax you owe and forget to include the levy and any Medicare Levy Surcharge. Planning for these amounts from the start of the financial year can help you avoid paying extra tax from savings or emergency funds at tax time.

This is especially important if you have a spouse’s income, combined income from more than one business, or family tiers for different dependants, because your family income can change how the rules apply. Treating the levy and any surcharge as part of your regular ATO savings habit makes it easier to keep your cash flow steady. Simple steps like transferring a set percentage of each invoice into a tax savings account can make a big difference.

How Do Income Thresholds and Family Circumstances Affect the Medicare Levy?

The Australian Government sets income thresholds each financial year to decide whether you pay the full Medicare Levy, get a Medicare Levy reduction, or may not have to pay at all. If your annual income is below a certain threshold for a single person or family income threshold, you may receive a reduction or full Medicare Levy exemption, depending on your personal circumstances. Above the upper income thresholds, most Australian taxpayers pay the full 2% rate.

Family income thresholds take into account your combined income with a spouse and any dependent child you support, so your family status directly influences how much levy you pay. The family income threshold increases for each dependent child, meaning larger families get extra room before paying the full levy. Seniors and pensioners tax concessions and the pensioners tax offset may also interact with these rules, so older small business owners should check how their certain income types are treated.

What Is the Medicare Levy Surcharge and When Might You Have to Pay It?

The Medicare Levy Surcharge is an extra tax that applies to certain higher‑income Australian taxpayers who do not hold hospital cover through an eligible private health insurance policy. Its purpose is to encourage individuals and families with higher incomes to take out private hospital cover and reduce pressure on the public system. If your income for MLS purposes is above the base income threshold and you, your spouse, or your family do not hold hospital cover for the full year, you may have to pay MLS on top of the standard levy.

The surcharge is worked out as a percentage of your income for MLS, which includes your taxable income plus some additional amounts used for surcharge purposes. Different family tiers and thresholds apply for a single person compared to couples and families, and these MLS income thresholds can change between financial years. That means your family income, including a spouse’s income and certain income from investments or business, may tip you into a tier where you have to pay MLS.

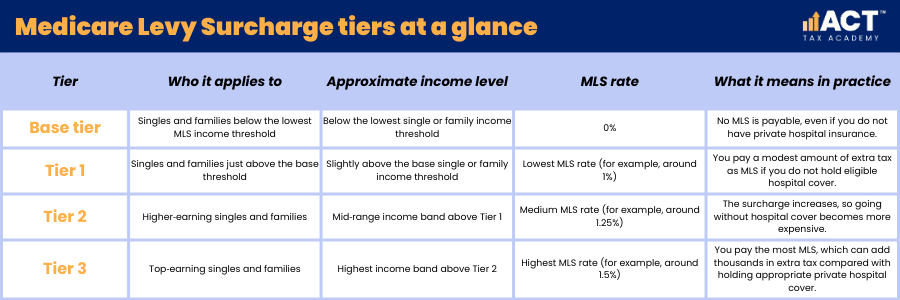

How Do the Medicare Levy Surcharge Tiers Compare for Different Incomes?

The Medicare Levy Surcharge uses tiers based on your annual income or your family income, depending on whether you are single or in a couple. At the base level, if your income is under the lowest MLS income threshold, you generally do not pay MLS, even if you do not have private hospital insurance. Once your income goes above the certain threshold, different family tiers and single thresholds apply with increasing MLS percentages.

At higher income tiers, you pay MLS at higher rates, which can add a noticeable amount of extra tax to your final bill. For a successful small business owner, this can mean paying several hundred or even several thousand dollars in surcharge, depending on annual taxable income and how much extra tax applies in your tier. Understanding which tier you are likely to fall into allows you to compare the true cost of MLS versus taking out appropriate private hospital cover.

How Can You Estimate Your Total Medicare Levy and Medicare Levy Surcharge?

To estimate your overall position, you first need to work out how much Medicare Levy you expect to pay based on your annual taxable income. That means adding up all income you expect to report in your income tax return, including business profit, wages, interest and dividends, then subtracting deductions to arrive at annual taxable income. Once you have this figure, you can apply the 2% rate, and then check whether low‑income rules, a Medicare Levy reduction, or partial exemption might apply.

Next, review whether you might pay MLS by calculating your income for MLS, which iincludes taxable income and some other components such as reportable super contributions (including both employer and personal deductible contributions). If you are above the MLS thresholds and do not hold private patient hospital cover for the full year, you can use a Medicare Levy Surcharge calculator to see how much extra tax might apply. Together, these two numbers give you a working estimate of the total health‑related tax you will face at tax time.

How Does Private Health Insurance Affect Whether You Pay the Medicare Levy Surcharge?

Having eligible private health insurance, specifically private hospital cover from a registered health insurer, is the main way to avoid paying the Medicare Levy Surcharge when your income is above the MLS thresholds. In general, you need to hold hospital cover, not just extras cover, and your private health insurance policy must meet certain criteria for MLS purposes. Basic hospital cover that meets the minimum standards can be enough for surcharge purposes, but it is important to confirm this with your insurer.

When you hold hospital cover for the full financial year, you can usually avoid paying MLS even if your income is high. You may also be entitled to a private health insurance rebate, sometimes called the Australian Government rebate, which is an amount the Australian Government contributes towards the cost of eligible health insurance. This can reduce the cost of private health cover and make it more attractive than paying the surcharge year after year.

Who Can Claim a Medicare Levy Exemption or Reduction, and What Does Exemption Mean?

You may qualify for a Medicare Levy exemption if you were a foreign resident for part or all of the financial year, or if certain medical requirements and residency rules apply. An exemption means you do not have to pay the Medicare Levy for the exempt period, even if you have taxable income above the usual thresholds. Some people need a Medicare Entitlement Statement from Services Australia to confirm they were not entitled to full Medicare benefits for that period.

Others may be eligible for a Medicare Levy reduction if their income is just above the lower threshold, or if their family income is low relative to the family income threshold. In those cases, you pay less tax by way of levy than the full 2%, according to your income and family status. Seniors and pensioners tax rules, such as the seniors and pensioners tax offset, can also affect how reductions and exemptions apply to older business owners.

What Practical Steps Can Small Business Owners Take to Plan for the Medicare Levy and MLS?

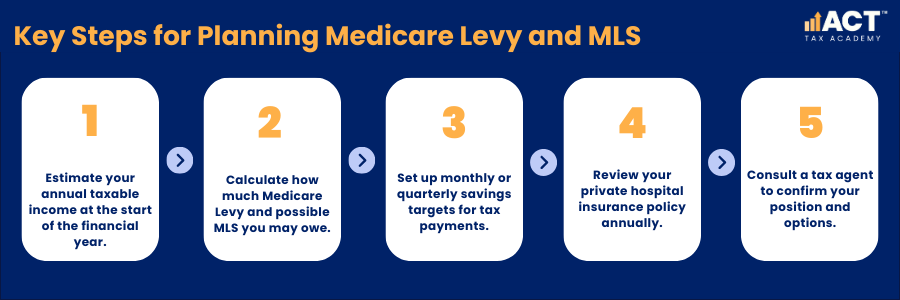

A simple starting point is to calculate your expected annual taxable income at the beginning of the financial year, then estimate how much tax, Medicare Levy, and possible Medicare Levy Surcharge will apply. You can break this down into a monthly or quarterly savings target, so you know exactly how much to transfer into a tax savings account as money comes in. This makes it easier to pay the Medicare Levy and any MLS without dipping into working capital.

It is also smart to review your health insurance annually and decide whether private hospital insurance is better value than paying MLS at your current income level. Checking your private health insurance policy wording ensures that you genuinely hold hospital cover that meets the criteria to avoid paying MLS. You can also speak with a tax agent who understands small business to confirm how the rules apply to your situation and to avoid paying more than necessary.

How Can a Tax Agent and Good Records Help at Tax Time?

Working with a tax agent who specialises in small business can give you clarity about how much extra tax you might owe from the levy and surcharge before the end of the year. A good adviser will look at all of your income sources, family income, and personal circumstances to estimate your income for MLS and your likely levy outcome. They can also show you how different choices, such as taking out private hospital insurance or changing drawings from your business, may reduce or avoid paying MLS.

Keeping accurate, up‑to‑date records of income, expenses, family changes and health insurance details throughout the financial year makes your final tax return more accurate and less stressful. When everything is organised, it is easier to understand how much tax you owe, how the Medicare Levy helps fund Australia’s public health system, and what you can do to manage your position fairly for the next year. Over time, this proactive approach supports both your financial goals and your access to quality care through Medicare and the broader health system.