Updated Corporate Tax Rate Implications for Small Companies in FY2025

The corporate tax rate for small companies in FY2025 brings real opportunities to keep more of what your business earns. Under the Base Rate Entity rules, eligible small companies now access a lower company tax rate of 25%, compared to the standard rate of 30% that applies to other companies. Understanding how these changes affect your assessable income and total company tax can help you make smarter decisions about profit reinvestment, dividends, and business growth.

The tax rules reflect Australia’s commitment to supporting active, growing businesses like yours. When your company qualifies for the lower rate, that extra capital stays in your business—ready for staff bonuses, equipment upgrades, or strategic expansion. However, the eligibility requirements are strict, and many business owners find the rules confusing. We’re here to break down exactly how this works and what it means for your bottom line.

What Are the Corporate Tax Rate Rules for Small Companies in FY2025?

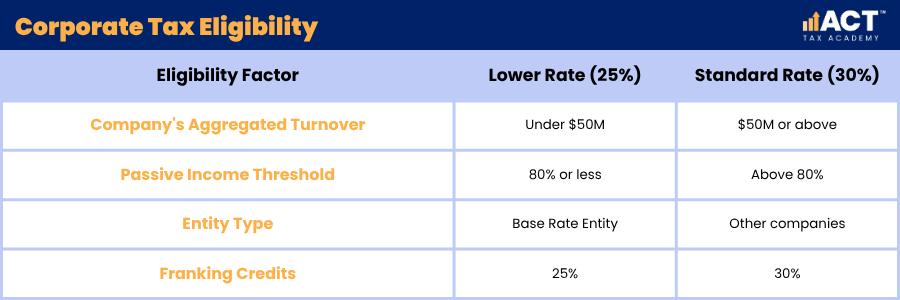

Your company qualifies for the 25% lower rate if it meets two key tests each year: you must have aggregated turnover under $50 million, and your passive income cannot exceed 80% of total assessable income. This is called Base Rate Entity status, and it’s the gateway to paying less company tax. The standard rate of 30% applies to all other companies, including those that exceed either threshold.

The income year deadline is critical—these tests are calculated annually, usually around June, and eligibility doesn’t carry over automatically. If your aggregated turnover creeps above $50 million, or if passive income (like interest income or rental income) suddenly climbs above 80%, you’ll lose access to the lower rate and pay the full company tax rate instead. This means staying organised with your bookkeeping and planning ahead throughout the year is essential.

Why Does the Company Tax Rate Matter for Your Business?

The difference between paying 25% and 30% company tax adds up quickly, especially when you multiply that saving across several years. A business earning $1 million in taxable income saves $50,000 annually under the lower rate—money you can reinvest, pay dividends, or use to expand. That’s not just a number; it’s the difference between modest growth and genuine business momentum.

Lower tax rates are one of the most direct ways government can support small business profitability. When you pay less tax on your profits, you have more capital to work with, more resources to hire skilled workers, and more flexibility to weather unexpected challenges. Your business becomes more resilient, more competitive, and better positioned to thrive in Australia’s economy.

What Counts as Passive Income Under These Rules?

Passive income includes money your company earns without active trading—interest income from bank accounts or loans, rental income from investment property, dividends from other investments, and royalty payments. When you calculate passive income, you add all these sources and divide by your total assessable income. If the result exceeds 80%, you lose the lower rate even if your revenue is well under $50 million.

This rule is designed to encourage active business operations rather than pure investment vehicles. A consulting firm with $3 million in revenue and only $50,000 in interest income easily qualifies (1.7% passive income). But a property holding company with the same revenue and $2.5 million in rental income would fall well above the 80% threshold. Understanding where your income comes from is critical to tax planning.

How Does Aggregated Turnover Work When You Have Multiple Entities?

Your company’s aggregated turnover is the combined revenue of your business plus any related entities you control. This means if you own two businesses, three rental properties through separate companies, or operate through related structures, you must add all their revenue together to test against the $50 million threshold. The ATO‘s definition of “related entities” is broad and catches most common ownership structures.

Many business owners are caught off guard by this rule. You might think your individual company is small and qualifies, but once you add in your spouse’s business, your investment company, or structures you set up for asset protection, the aggregated turnover suddenly exceeds $50 million. Planning your entity structure—especially across several years of growth—requires careful attention to these rules.

What Are the Income Inclusion Rule and Undertaxed Profits Rule?

Australia’s undertaxed profits rule and income inclusion rule represent a shift toward ensuring multinationals and large entities pay a minimum amount of tax. These rules apply mainly to large companies but understanding them matters because they signal the direction of tax policy. They’re designed so profits shifted to low-tax countries still contribute fairly to Australia’s tax base.

While these rules don’t directly impact most small companies qualifying for the 25% rate, they’re worth knowing about. They reflect government commitment to a level playing field where all businesses—large and small—contribute fairly. They also indicate that accessing lower rates means meeting strict eligibility rules and staying compliant with Australian tax laws.

What Happens to Franking Credits at the Lower Rate?

Franking credits work differently depending on your company tax rate. If your company qualifies for the 25% rate, dividends you pay carry a 25% franking credit. This means your shareholders receive clearer dividend income, and the franking credit offsets some of their personal tax. If you lose Base Rate Entity status and pay the 30% rate instead, dividends carry a 30% franking credit—potentially creating mismatches if your shareholders are used to lower franking.

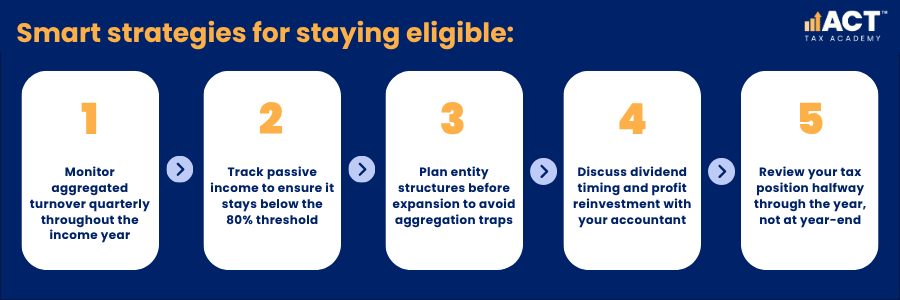

Dividend planning is essential when your tax rate might change. If you’re approaching the $50 million threshold or expecting fluctuations in passive income, timing dividend payments and calculating franking correctly prevents tax surprises. Many business owners consult quarterly to ensure their dividend strategy aligns with current tax rate eligibility.

Franking credit implications:

- Plan dividends carefully if your rate might change mid-year

- Lower rate (25%) = 25% franking on dividends

- Standard rate (30%) = 30% franking on dividends

- Mismatched franking can create tax issues for shareholders

How Can You Maximise the Benefits of the Lower Tax Rate?

Strategic planning throughout the income year helps you stay under the thresholds and lock in the 25% rate. Start by monitoring your company’s aggregated turnover quarterly—don’t wait until June to discover you’ve overshot $50 million. Track your passive income sources too. If interest income is climbing, consider reinvesting profits into business operations instead of letting cash sit in low-interest savings.

Entity structuring is another smart move. If you’re expanding your business empire, discuss with us how to set up new ventures in ways that don’t automatically trigger aggregated turnover issues. Asset protection strategies can also align with tax efficiency. We help business owners like you plan ahead, so you’re not scrambling at tax return time.

What Other Tax Changes Affect Small Companies in FY2025?

Beyond the corporate tax rate, several other changes impact your business. The Superannuation Guarantee rises to 12% from 1 July 2025, increasing payroll costs for every employer. Capital gains rules remain largely unchanged, but planning around capital gains—especially net capital gains—still matters for overall tax efficiency. Small business CGT concessions are still available if you meet the eligibility tests, offering significant savings on asset sales.

Interest income deductibility rules have shifted, making it harder to claim interest on loans used for passive investments. This is another reason to plan your financing carefully. These rules don’t affect every small company equally but understanding them helps you avoid costly mistakes.

Conclusion

The updated corporate tax rate rules in FY2025 create real savings for eligible small companies, but eligibility requires year-round attention. Staying under $50 million in aggregated turnover and keeping passive income at or below 80% of total assessable income are the keys to accessing the 25% rate and maximising profit retention.

Your tax strategy should start now, not at tax return time. We recommend reviewing your current structure, tracking your turnover and income mix quarterly, and discussing any planned expansion with us well in advance. Small decisions made early in the income year can mean thousands in tax savings by June.

If you’re unsure whether your company qualifies or wants to examine ways to maximise the lower rate, we’re here to help. At ACT Tax Academy, we work with growing businesses across the ACT to turn tax rules into practical strategies that protect your profit and support your growth. Get in touch today to discuss your FY2025 tax position and lock in the savings you deserve.