FBT Exemptions Explained: What Counts as Minor and Infrequent Benefits?

Understanding Fringe Benefits Tax (FBT) exemptions can feel overwhelming when you’re trying to reward your team while managing compliance costs. The minor and infrequent FBT exemption is one of the most valuable tools available to Australian employers, allowing you to provide certain benefits to employees without triggering FBT liability.

Understanding the Minor Benefits Exemption Rules

The minor benefits exemption operates under specific criteria that determine whether small-value benefits escape Fringe Benefits Tax liability. Getting familiar with these rules helps you provide meaningful employee benefits without unexpected tax consequences that could impact your business cash flow.

The exemption applies when both conditions are met: the benefit must have a notional taxable value less than $300, and it must be unreasonable to treat the benefit as a fringe benefit. This creates a practical framework that recognises not every small benefit should trigger complex FBT calculations and compliance requirements for your business.

The $300 Value Threshold

The $300 threshold applies to each individual benefit’s notional taxable value, which represents what the benefit would be worth if it were subject to Income Tax. Each benefit is assessed separately even when provided together, meaning a $250 meal remains exempt when provided alongside a $200 taxi ride. Benefits to employee associates don’t count toward the $300 limit, and the GST inclusive value determines whether you meet the threshold. Multiple similar benefits can push you over the exemption limit even when individual items stay under $300.

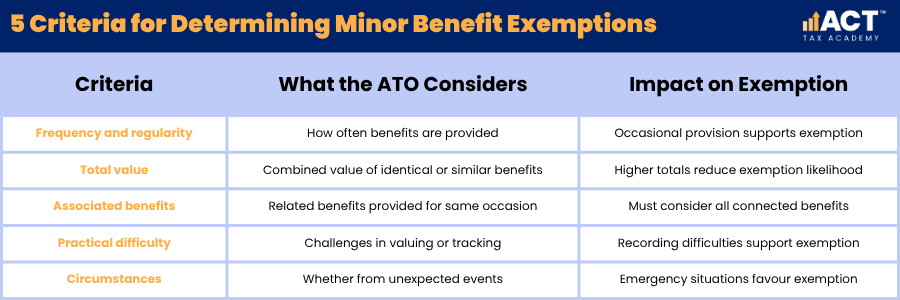

The “Unreasonable to Treat” Test

Meeting the $300 threshold alone doesn’t guarantee your minor benefit will be exempt from FBT. The ATO applies five specific criteria when determining if treating the benefit as a fringe benefit would be unreasonable:

How to Apply Minor Benefit Exemptions in Practice

Real-world examples help clarify how the minor benefits exemption applies across different workplace situations. These scenarios demonstrate practical approaches to determining which small benefits can be exempt from FBT while supporting your team effectively.

Understanding which benefits qualify helps you structure employee appreciation programs that deliver value without creating unnecessary FBT liability for your business.

Common Exempt Minor Benefits

The following benefits typically qualify for the minor benefits exemption when provided infrequently:

- Small tokens of appreciation for one-off achievements or milestones

- Welcome gifts for new employees under $300 in GST inclusive value

- Occasional meals provided three times or less during the FBT year

- Special occasion flowers for birthdays, births, or get-well wishes

- Christmas time gifts like wine or perfume given annually

- Emergency assistance during unexpected events or workplace incidents

Work-Related Benefits That Avoid FBT

Taxi travel expenses can qualify when provided occasionally and not part of a salary packaging arrangement. Multiple taxi payments during the year, each valued under $300 and not forming a regular pattern, would likely be exempt due to their small individual value and practical difficulty in recording detailed usage.

Emergency services for employees during unexpected events qualify when they’re genuine responses to unforeseen circumstances. Emergency accommodation, meals during transport strikes, or assistance during workplace incidents demonstrate the type of responsive benefits that qualify.

Protective clothing and computer software used primarily for work purposes receive complete FBT exemptions rather than falling under minor benefits rules. These work-related items are recognised as essential business tools rather than personal advantages.

Benefits That Don’t Qualify for Exemption

These types of benefits cannot use the minor benefits exemption:

- Entertainment expenses calculated using the 50/50 method

- Regular meal patterns like weekly staff lunches

- High-value entertainment benefits exceeding $300

- Systematic benefit rotations among different employees

- Benefits resembling salary or regular compensation

- Private use of company assets on a regular basis

Meal Entertainment and Special Occasion Exemptions

Food and drink provisions create specific FBT considerations that depend heavily on timing, location, and purpose. Understanding these nuances helps you provide appropriate workplace refreshments while managing your FBT obligations effectively.

The treatment of meal entertainment under FBT rules requires careful consideration of whether you’re using the actual method or 50/50 method for calculating your liability, as this affects which exemptions you can access.

On-Premises Food and Light Refreshments

Food provided on business premises follows specific exemption rules. Current employees can receive food and drink on working days without FBT, and business premises includes any location where work is performed. Light refreshments at staff meetings qualify for exemption, but employee associates don’t qualify and create FBT liability. Social functions like Christmas parties are treated as entertainment benefits subject to FBT rather than workplace refreshments.

Minor Benefits in Entertainment Context

Meal entertainment under $300 may qualify for the minor benefits exemption when provided infrequently and on an irregular basis. A one-off staff celebration lunch costing $250 per person could be an exempt minor benefit, provided it’s not part of a regular pattern.

Christmas parties demonstrate how minor benefits interact with entertainment expenses. If the per-person cost stays under $300 and parties occur infrequently, the minor benefits exemption may apply when you use the actual method of meal entertainment calculation.

However, if you’re using the 50/50 method for meal entertainment calculations, you can’t access the minor benefits exemption. This method treats 50% of all meal entertainment expenses as subject to FBT, regardless of individual benefit values or frequency.

Provide Gifts at Entertainment Events

Gift-giving at workplace events requires careful consideration and separate assessment from entertainment costs. Christmas time gifts can be exempt while party costs remain taxable, and small gifts under $300 typically qualify when given annually. Gift cards may be treated as entertainment rather than gifts, and the timing of gift provision affects exemption eligibility.

Making Smart Decisions About Employee Benefits

Strategic benefit planning allows you to reward employees effectively while minimising your FBT liability. Understanding how different exemptions interact helps you create comprehensive employee benefit programs that balance compliance requirements with team appreciation goals.

Taking a thoughtful approach to structuring benefits ensures you maximise the value delivered to your team while keeping unnecessary tax costs under control for your business.

Record Keeping and Documentation Requirements

Clear business purposes should be documented for all benefits claimed as exempt. Work-related items need evidence of primary work use, while minor benefits require documentation of their occasional, irregular nature for your necessary records.

Separate benefit tracking prevents exemption complications when FBT applies to some benefits but not others. Maintaining distinct records for different types of benefits helps demonstrate compliance with various exemption criteria and value thresholds.

Employee acknowledgments can support exemption claims by documenting the work-related nature of benefits and confirming they’re not provided as regular compensation or in lieu of an Income Tax deduction.

Planning Your FBT Strategy

To develop an effective FBT strategy for the upcoming year, consider establishing annual benefit budgets that help maintain exemption eligibility. Alternative benefit structures may provide better value than taxable benefits, while professional advice becomes valuable for complex benefit programs. Regular reviews ensure your approach remains compliant and effective, and employee communication helps staff understand benefit structures. Contingency planning addresses unexpected benefit situations that may arise throughout the FBT year.

Understanding FBT exemptions for minor and infrequent benefits empowers you to create meaningful employee appreciation programs while maintaining compliance with Australian tax obligations. The key lies in genuine infrequency, appropriate value thresholds, and clear business purposes that demonstrate why treating these benefits as fringe benefits would be unreasonable.