Corporate Trustee vs Individual Trustee: Asset Protection for SMEs

Corporate trustee vs individual trustee decisions can make or break your asset protection strategy. Many Small and Medium-sized Entities (SMEs) struggle with liability concerns and worry about potentially putting their personal assets at risk through poor trustee structure choices. The wrong decision could leave your family home, investment properties, and years of hard work vulnerable to creditors and legal claims. Choosing the right trustee structure isn’t just about immediate costs—it’s about building a foundation that protects your wealth for generations.

Why Your Trustee Choice Determines Your Asset Protection Success

Understanding the fundamental differences between trustee structures is critical for any SME owner serious about protecting their wealth. Your trustee choice impacts every aspect of your asset protection strategy, from immediate liability exposure to long-term succession planning and ongoing compliance obligations.

The trustee becomes the legal owner of trust assets while managing them for one or more beneficiaries. This arrangement creates separation between your personal assets and business risks, but the effectiveness depends entirely on whether you choose an individual or corporate trustee structure.

The Growing Asset Protection Challenge for Australian SMEs

Australian SMEs face increasing liability risks that can quickly escalate beyond business operations to threaten personal wealth. Professional indemnity claims, employee disputes, creditor actions, and even family law proceedings can all target assets held in poorly structured arrangements.

Traditional business insurance often falls short of protecting personal assets from these diverse risks. Many business owners discover too late that personal guarantees, director liability, and inadequate trust structures leave their family assets exposed to business creditors.

The challenge becomes more complex as businesses grow and accumulate valuable assets. What starts as a simple family business can evolve into a multi-million-dollar operation with sophisticated asset holdings, making proper trustee structure selection essential for long-term wealth protection.

How Trustee Structures Create Legal Protection

Trust arrangements work by separating legal ownership from beneficial enjoyment of assets. The trustee holds legal ownership and manages trust assets according to the trust deed, while beneficiaries receive distributions and economic benefits without direct asset ownership.

This separation prevents creditors from directly accessing trust assets when pursuing claims against individual beneficiaries. However, the protection level varies significantly between individual and corporate trustees, with corporate trustee structure offering superior liability protection through separate legal entity status.

Understanding Individual Trustee Limitations and Risks

Individual trustees might seem straightforward and cost-effective, but they expose your entire asset protection strategy to significant personal liability risks. When natural persons act as trustees, they carry personal responsibility for all trust obligations and become personally liable for any trust-related debts or legal issues.

This personal liability extends far beyond the trust assets themselves, potentially exposing the individual trustee’s personal assets including their family home, personal investments, and other wealth accumulated outside the trust arrangement.

Personal Liability Creates Dangerous Asset Exposure

The most significant risk with individual trustees is unlimited personal liability for the trust’s obligations. If your trust faces legal action, incurs debts, or encounters financial difficulties, the individual trustee becomes personally responsible for these obligations.

This means creditors can pursue not only the trust assets but also the trustee’s personal property to satisfy trust debts. Your family home, personal bank accounts, investment portfolios, and other personal assets become vulnerable to trust-related creditor claims.

The risk becomes particularly acute in business contexts where trusts hold commercial property, enter supplier contracts, or employ staff. Any business-related legal disputes or creditor actions can potentially access the individual trustee’s personal assets, completely undermining your asset protection objectives.

Asset Separation Becomes Nearly Impossible

Individual trustees struggle to maintain clear separation between personal and trust assets, creating confusion in asset ownership records and weakening the entire trust structure. This blending of interests makes it difficult to defend the arrangement during legal proceedings or tax audits.

Courts may question whether assets are genuinely held on trust when the same person acts as trustee and beneficiary. Without clear institutional separation, creditors can argue that personal assets should be treated as trust property, or vice versa, depending on what serves their collection interests.

Proper trust administration becomes challenging when the trustee manages both personal finances and trust assets through the same systems and processes. This administrative overlap creates documentation problems that can prove costly during legal disputes or regulatory investigations.

Succession Planning Complications

Individual trustees create significant succession planning obstacles that can expose assets during transition periods. When individual trustees die, become incapacitated, or wish to retire, the trust assets must be transferred to a new trustee through complex legal processes.

These transitions often trigger stamp duty obligations on asset transfers, creating substantial costs that reduce the trust’s value. Capital Gains Tax (CGT) events may also crystallise during trustee changes, potentially eroding asset values through unnecessary tax liabilities.

The administrative complexity of changing individual trustees requires court applications, new trust deed preparations, or complex asset reassignment procedures. During these transition periods, determining legal ownership becomes unclear, potentially exposing assets to creditor claims or family disputes.

How Corporate Trustees Deliver Superior Asset Protection

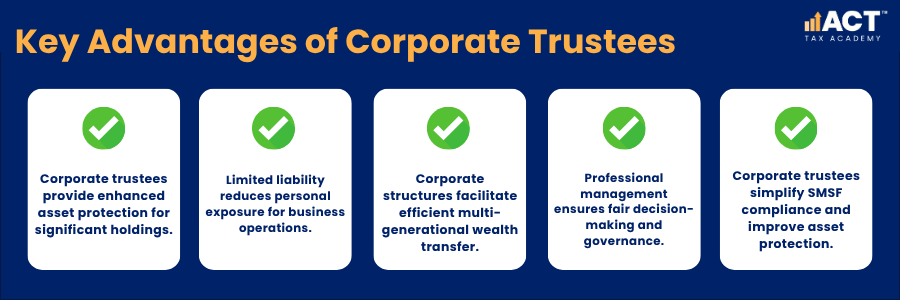

A corporate trustee provides fundamentally better asset protection by creating a separate legal entity to hold trust assets and manage trustee responsibilities. This approach involves establishing a company specifically established to act as trustee, with directors controlling day-to-day trust operations while shareholders maintain control.

The corporate entity creates institutional separation between trust management and personal interests, delivering limited liability protection that shields personal assets from trust-related risks. This separation strengthens the entire trust structure and provides operational flexibility that grows with your business needs.

Limited Liability Protection Shields Personal Assets

The primary advantage of a corporate trustee lies in its limited liability structure, which confines trust-related liability to corporate assets rather than personal wealth. The trustee company bears responsibility for trust debts and obligations, protecting directors’ and shareholders’ personal assets provided they fulfil their fiduciary duties.

This protection extends across various risk scenarios including contractual disputes, employee claims, professional indemnity issues, and general commercial liabilities. While directors can still face personal responsibility for deliberate wrongdoing or breach of duties, the corporate structure provides substantial protection for ordinary business risks.

Many corporate trustee companies operate with minimal assets specifically to limit exposure while maintaining their legal obligations. This approach ensures that even if the trustee company faces significant claims, the maximum exposure remains limited to the company’s assets rather than extending to personal wealth.

Professional Trust Management and Administration

Corporate trustee structure offers professional trust management through formal governance systems, documented decision-making processes, and institutional administrative procedures. This professional approach strengthens the trust’s legal validity and reduces risks associated with informal trust administration.

The corporate structure enables proper separation of trust management from personal interests, making it easier to maintain accurate asset ownership records and defend the trust arrangement during legal proceedings. This institutional approach demonstrates genuine trust arrangements to courts and regulatory authorities.

Professional trust administration through corporate trustees also facilitates compliance with legal and tax requirements, reduces reporting obligations compared to individual arrangements, and provides better documentation for audit or legal review purposes.

Simplified Succession Planning Through Corporate Continuity

Corporate trustees exist indefinitely, providing exceptional succession planning advantages that maintain asset protection across generations. Changes in trust control occur through standard company mechanisms rather than complex asset transfers.

Director changes can be implemented through simple Australian Securities and Investments Commission (ASIC) forms without transferring trust assets or triggering stamp duty obligations. Shareholder transfers allow control succession without creating CGT events on trust assets, maintaining tax efficiency during generational transitions.

This perpetual existence ensures that asset protection structures remain intact during family transitions, business changes, or generational wealth transfers. The corporate trustee remains constant while control mechanisms adapt to changing family circumstances through standard company procedures.

Making the Right Choice for Your Circumstances

Choosing between individual or corporate trustee requires careful consideration of your specific circumstances, risk tolerance, and long-term objectives. While individual trustees might appear simpler initially, most SMEs benefit from the superior protection and flexibility offered by corporate trustee arrangements.

Your decision should consider immediate setup costs against long-term benefits, compliance obligations, professional management requirements, and succession planning needs. The right choice aligns with your risk profile and provides adequate protection for your current and anticipated asset levels.

When Corporate Trustees Make Clear Sense

Corporate trustee structure offers clear advantages for most SME situations, particularly where significant assets require protection or business operations create liability exposure. The benefits become even more pronounced as asset values grow, or business risks increase.

Significant Asset Holdings and Business Operations

SMEs with valuable asset holdings benefit substantially from corporate trustee protection, especially where potential liability exposure exceeds the costs of establishing and maintaining the corporate structure. Business operations involving contracts, employees, or public liability risks create ongoing exposure that justifies corporate trustee investment.

The cost-benefit analysis strongly favours corporate trustees when trust assets exceed several hundred thousand dollars or when business operations generate substantial revenue streams. Professional management and limited liability protection become essential as asset complexity increases.

Family Succession and Multi-Generational Planning

Families planning to transfer wealth across generations find corporate trustees invaluable for maintaining asset protection while facilitating smooth succession processes. The ability to change control without asset transfers preserves tax efficiency and maintains protection integrity.

Multiple beneficiaries benefit from formal decision-making processes that corporate trustees provide, ensuring fair treatment and clear governance procedures. This becomes particularly important in complex family situations where relationships may change over time.

Self-Managed Super Fund (SMSF) Arrangements

SMSF trustees particularly benefit from corporate structures due to regulatory requirements and compliance advantages. Corporate trustees simplify member changes, reduce documentation requirements, and provide better protection for SMSF assets.

When Individual Trustees Might Work

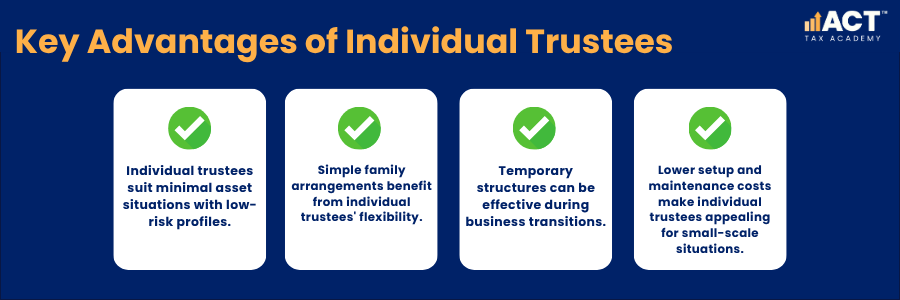

Individual trustees may suit very specific circumstances involving minimal assets, simple family arrangements, and cost-sensitive situations where basic protection suffices for the limited risks involved.

Limited Asset Exposure and Simple Arrangements

Arrangements involving minimal assets with low-risk profiles might justify individual trustee structures where potential liability exposure remains small and unlikely. Simple family situations with single beneficiaries and basic distribution needs may not require corporate complexity.

However, even in these situations, the benefits of limited liability protection and simplified succession planning often justify the modest additional costs of corporate trustee arrangements, particularly given the potential for asset growth over time.

Temporary or Transitional Structures

Individual trustees might serve temporary purposes during business establishment or transition periods, pending the development of more sophisticated structures. However, early establishment of corporate trustees often proves more cost-effective than later restructuring.

Professional Expertise and Ongoing Management

Both trustee structures require professional advice for proper establishment and ongoing management, with corporate trustees demanding more sophisticated expertise for company registration, trust deed preparation, and compliance management. Professional management costs for corporate trustees include Australian Securities and Investments Commission (ASIC) compliance, company administration, and more complex reporting obligations compared to individual arrangements.

While individual trustees might appear simpler and cheaper initially, corporate trustee structure offers substantially superior protection, operational flexibility, and succession planning benefits. For most Australian SMEs, the enhanced asset protection, limited liability benefits, and professional management capabilities of corporate trustees justify the additional setup and ongoing costs.

Take action to review your current trustee arrangements and consider whether they provide adequate protection for your circumstances. Consult with qualified professionals to assess your options and implement structures that truly safeguard your wealth.