Non-Concessional Super Contributions and The Bring Forward Rule: Avoiding Common Errors

Bookkeeping for Non-Concessional Super Contributions can feel overwhelming when dealing with complex contribution caps, reporting requirements, and the potential for costly penalties if mistakes occur. Many Australian business owners and individuals struggle with accurately recording and managing these after-tax contributions, often discovering errors only when the Australian Taxation Office issues penalty notices or during audit processes.

Understanding Non-Concessional Super Contributions and Their Impact

Managing non concessional contributions requires understanding both their nature and the strict regulatory framework surrounding them. These after-tax contributions form a crucial part of retirement planning but come with specific bookkeeping requirements that, when neglected, can result in severe financial consequences.

What Are Non-Concessional Contributions?

Non concessional contributions are payments made to your super fund using money that has already been taxed from your after tax income. These contributions include personal contributions, spouse contributions, and certain transfers from overseas superannuation funds. Unlike concessional contributions, these don’t reduce your taxable income and aren’t subject to the 15% contributions tax within the super fund.

The current non concessional contributions cap stands at $120,000 per financial year for 2025-26. However, eligible individuals can access the bring forward arrangement, allowing them to contribute up to three years worth of non concessional contributions in a single year, potentially reaching $360,000. Your eligibility to use the bring forward depends on your age and total super balance on 30 June of the previous financial year.

If your super balance is under $1.66 million, you can trigger the bring forward rule and contribute the maximum amount over a three year period. Those with balances between $1.66 million and $1.78 million have partial access to the bring forward provision, while those with $1.9 million or more cannot make non concessional contributions.

The High Cost of Bookkeeping Errors

Poor bookkeeping practices around non concessional contributions can trigger significant financial penalties and compliance issues. When you exceed the non-concessional cap, you must pay extra tax on the excess amount. The Australian Taxation Office offers two options: withdraw the excess non concessional contributions and 85% of associated earnings (with earnings taxed at your marginal tax rate), or leave the excess in superannuation where it faces additional tax of 47%.

This means a $50,000 excess contribution could result in $23,500 in extra tax if not withdrawn. Beyond immediate penalties, bookkeeping errors can lead to Australian Taxation Office audits, which often uncover additional discrepancies in related areas such as payroll records and superannuation guarantee compliance.

Record-Keeping Requirements and Compliance

The Australian Taxation Office requires comprehensive documentation for all super contributions, with records maintained for a minimum of five years. For Self-Managed Superannuation Funds, trustees must keep detailed financial records that explain all transactions and the fund’s financial position. This includes contribution receipts, bank statements, member contribution statements, and documentation supporting the classification of each contribution type.

Most Common Bookkeeping Errors with Non-Concessional Contributions

Understanding the most frequent mistakes in bookkeeping for non-concessional contributions is essential for maintaining compliance and avoiding costly penalties. These errors often stem from misunderstanding contribution classifications, poor record maintenance, or inadequate monitoring systems.

Misclassifying Contribution Types

One of the most serious errors occurs when contributions are incorrectly classified between concessional and non-concessional categories. If you make a personal contribution intending to claim an income tax deduction but fail to provide the required notice to your super fund trustee, the contribution may be treated as non-concessional. This can result in the Australian Taxation Office counting the same contribution twice when assessing your caps, potentially triggering excess contribution penalties.

The tax deduction notice must be provided before the fund begins paying any pension based on the relevant contribution. This timing issue has caught many Self-Managed Superannuation Fund members who attempt to segregate taxable and tax-free components for estate planning purposes.

Inadequate Monitoring of Contribution Caps

Many individuals and businesses fail to implement proper systems for tracking contributions across multiple super accounts. If you have more than one super account, all non concessional contributions made to all funds during a financial year count towards your single annual cap. This aggregation requirement means that without comprehensive monitoring, you might unknowingly exceed your limits.

The bring forward arrangement adds complexity to monitoring requirements. Your eligibility and the amount you can bring forward depends on your total super balance on 30 June of the previous financial year and your age. If you accidentally trigger the bring forward rule without proper planning, you might use up future year caps when you didn’t intend to do so.

Poor Documentation and Record Storage

Insufficient documentation represents a fundamental bookkeeping error that can have far-reaching consequences. Many taxpayers fail to maintain adequate records of contribution sources, payment dates, and the intended treatment of each contribution. Without proper documentation, it becomes impossible to defend your position during Australian Taxation Office reviews or to correct misallocated contributions.

Self-Managed Superannuation Fund trustees are particularly vulnerable to documentation errors, as they must maintain records that demonstrate compliance with the sole purpose test and proper segregation of fund assets from personal assets. Missing or inadequate records can result in fund disqualification and significant tax consequences.

Failure to Account for Age-Based Restrictions

Age-related contribution rules create another common source of bookkeeping errors. Once you turn 75, you cannot make non concessional contributions, except under very specific circumstances. If you’re approaching this age threshold, your total super balance determines your eligibility to make final contributions.

Bookkeeping systems that don’t account for these age-based restrictions can result in ineligible contributions that must be returned within 30 days to avoid compliance breaches. The failure to implement age-monitoring controls has resulted in significant penalties for both individuals and Self-Managed Superannuation Fund trustees.

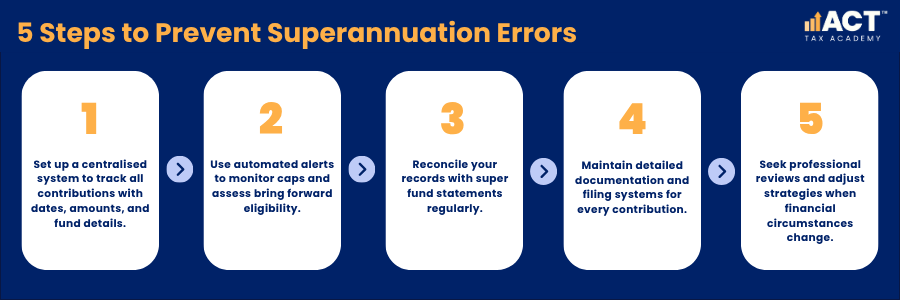

Practical Strategies to Prevent Common Bookkeeping Errors

Implementing robust bookkeeping practices and systems is crucial for avoiding costly mistakes that plague many superannuation contribution management processes. These strategies focus on creating systematic approaches to monitoring, documentation, and compliance verification.

Establishing Comprehensive Monitoring Systems

Create a centralised tracking system that monitors all contributions across all your super accounts. This system should include contribution dates, amounts, fund details, and classification for each payment. Use spreadsheets or specialised software to maintain running totals against the annual non concessional cap, including calculations for bring forward arrangements where applicable.

Set up automated alerts well before you approach contribution caps, allowing time to make informed decisions about additional contributions. Monitor your balance on 30 June each year to determine your remaining cap space and eligibility for the bring forward provision in the following financial year.

Regular reconciliation between your records and super fund statements helps identify discrepancies before they become compliance issues. Pay particular attention to how excess concessional contributions that haven’t been withdrawn are treated, as these automatically count towards your non concessional cap.

Implementing Proper Documentation Procedures

Develop standardised procedures for documenting all super contributions, ensuring every payment includes sufficient detail to support its classification and treatment. Maintain copies of all contribution confirmations, bank transfer records, and any correspondence with super funds regarding contribution treatment.

For personal contributions where you intend to claim a tax deduction, ensure the required notices are submitted promptly and confirmation of receipt is obtained. Create a filing system that organises records by financial year and contribution type, making them easily accessible for annual tax return preparation and potential Australian Taxation Office reviews.

Engaging Professional Support and Regular Reviews

Consider engaging qualified professionals who specialise in superannuation compliance to review your bookkeeping practices and identify potential issues before they become problems. Professional advice can help you understand complex scenarios such as the bring forward period rules, managing excess contributions, and improving your contribution strategy based on your financial situation.

Schedule regular reviews of your contribution strategy and bookkeeping practices, particularly when your circumstances change, such as salary increases, bonus payments, or approaching age thresholds. These reviews should assess your current position against contribution caps and evaluate the effectiveness of your monitoring systems.

Advanced Compliance Considerations and Error Prevention

Beyond basic bookkeeping practices, sophisticated compliance management requires understanding complex scenarios and implementing preventive measures that address the most challenging aspects of non-concessional contribution management.

Managing Complex Contribution Scenarios

Self-Managed Superannuation Fund trustees face additional complexity when managing in-specie contributions, property transfers, and international superannuation transfers. These transactions require careful valuation and documentation to ensure proper classification and compliance with contribution caps.

When dealing with excess concessional contributions that haven’t been withdrawn, understand that these automatically count towards your non concessional contribution cap. This interaction between contribution types requires careful monitoring to prevent inadvertent breaches of the non concessional cap during the year bring forward period.

Life insurance premiums paid by your super fund don’t count towards contribution caps but must be properly recorded to avoid confusion during Australian Taxation Office reviews. Fund fees and other administrative costs also require accurate recording to maintain clear separation between contributions and operational expenses.

Technology Solutions and Automation

Use technology to reduce manual errors and improve compliance monitoring. Modern systems can track your total super balance, monitor contribution caps, and alert you before you approach limits. However, these systems require regular maintenance and updates to reflect changing regulations and individual circumstances.

Consider platforms that integrate with your accounting software to provide real-time contribution monitoring and automated compliance reporting. These solutions can flag potential issues before they become breaches and maintain comprehensive audit trails for all transactions.

Preparing for Australian Taxation Office Reviews

Develop comprehensive audit preparation procedures that ensure all records are readily available and properly organised. Create summary reports that show contribution totals by type and financial year, making it easy to demonstrate compliance with caps and regulations.

Maintain detailed explanations for any unusual transactions or timing differences that might raise questions during reviews. Establish relationships with qualified professionals who can provide support during Australian Taxation Office interactions and help understand complex compliance issues.

Understanding your rights and options when dealing with excess contributions ensures you make informed decisions that minimise tax consequences. Familiarise yourself with the Australian Taxation Office determination process and the timeframes for responding to excess contribution notices.

Conclusion

Accurate bookkeeping for non-concessional super contributions requires systematic attention to detail, comprehensive monitoring systems, and proactive compliance management. When planning your superannuation strategy, remember that the general transfer balance cap affects your ability to move funds to pension phase, which impacts your overall contribution planning.

Understanding the interaction between before tax contributions and after-tax contributions ensures you maximise your total superannuation savings while staying within all applicable limits. The key to success lies in establishing clear documentation procedures and maintaining comprehensive contribution monitoring across all super accounts.

If you’ve used the bring forward non concessional arrangement, you must track this carefully to avoid making further non concessional contributions that exceed your available cap space. Take action today by reviewing your current bookkeeping practices and implementing the strategies outlined in this guide. Your future financial security depends on getting these fundamentals right, and the investment in proper systems and professional support will pay dividends in avoiding costly errors and maximising your retirement savings potential.