Bookkeeping and Payroll Implications for Foreign Workers and Tax Residency

Bookkeeping and payroll implications for foreign workers and tax residency have never been more complex as Australian businesses increasingly hire international talent. Understanding tax obligations, compliance requirements, and reporting responsibilities can feel overwhelming, especially when visa conditions, residency status, and employment arrangements all influence your business’s obligations.

Understanding Tax Residency and Its Impact on Payroll Obligations

Tax residency determination forms the foundation of all payroll and bookkeeping obligations for foreign workers in Australia. The Australian Taxation Office uses four distinct tests to determine residency status, and the outcome directly affects how you calculate wages, withhold taxes, and report earnings.

How Tax Residency Tests Work

The primary test, known as the resides test, considers factors such as physical presence intention purpose family business, employment ties maintenance, and your usual home. Unlike visa status, tax residency focuses on the substance of an individual’s connection to Australia rather than their legal right to remain in the country.

The 183 day test creates additional complexity for short-term arrangements. Workers physically present in Australia for more than half the income year generally qualify as tax residents, unless their usual home remains overseas with no intention of taking up Australian residence.

Why Residency Status Matters for Your Business

Understanding whether someone is a foreign resident or Australian resident for tax directly impacts your payroll setup, withholding calculations, and reporting obligations. Getting this determination wrong can result in incorrect tax withholding and compliance issues.

The 183 day test applies when other residency tests don’t clearly establish someone’s status. It’s one of three statutory tests used alongside the resides test and the domicile test to determine your residency situation.

Australian Residents for Tax Purposes

When foreign workers qualify as Australian resident for tax purposes, they benefit from the tax free threshold of $18,200, meaning they don’t pay income tax on the first portion of their earnings. These employees must declare worldwide income, including foreign income, though they may claim tax offset for taxes paid overseas.

For payroll purposes, employees who are Australian resident for tax require Pay As You Go withholding on all income, Single Touch Payroll reporting for every pay event, and inclusion in activity statements. They’re also entitled to Superannuation Guarantee contributions at the current rate of 12%, regardless of their visa status.

Residents are generally subject to the 2% Medicare levy, but some temporary residents can claim an exemption if they were not entitled to Medicare benefits (requires a Medicare Entitlement Statement). PAYG tax tables (including levy adjustments) handle this in withholding.

Foreign Residents for Tax Purposes

Foreign residents face different obligations and limitations. They don’t receive the tax free threshold, meaning tax applies from the first dollar earned. They’re only taxed on Australian sourced income, which includes employment income, rental income from Australian properties, and capital gains on taxable Australian property.

Foreign residents are exempt from the Medicare levy and don’t need to declare Australian sourced interest, dividends, or royalties where tax has already been withheld. However, they still require Pay As You Go withholding on Australian employment income, though at resident rates that differ from Australian residents.

Compliance Requirements for Bookkeeping and Payroll Systems

Modern payroll compliance extends far beyond simple wage calculations, particularly when managing foreign workers with varying residency status. The introduction of Single Touch Payroll has fundamentally changed how businesses report employment information to the Australian Taxation Office, creating real-time visibility over payroll accuracy and compliance.

Understanding Your Reporting Obligations

Understanding your obligations requires careful consideration of each worker’s tax situation. Whether someone is resident for tax purposes or a foreign resident determines not only withholding tax provisions but also what information you must report and when.

The test applies differently depending on work location and duration. Australian government employees working overseas have specific reporting requirements that differ from private sector arrangements.

Single Touch Payroll Reporting Rules

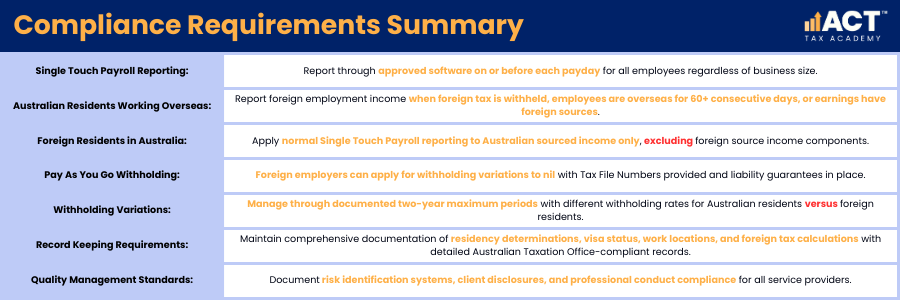

All Australian employers must report through Single Touch Payroll-enabled software on or before each payday, regardless of business size. For foreign workers, this creates specific challenges around income classification and reporting requirements that vary based on residency status and work location.

Reporting for Australian Residents Working Overseas

Employees who are Australian resident for tax working overseas require foreign employment income reporting through Single Touch Payroll when the employer has withheld foreign tax, the employee is in any foreign country for at least 60 consecutive days, or the earnings have a foreign source. This reporting can occur through pay events during the year, update events, or as part of the year-end finalisation process.

Reporting for Foreign Residents in Australia

Foreign residents present additional complexity. If they’re working in Australia, normal Single Touch Payroll reporting applies to their Australian sourced income. However, businesses must configure their payroll software to exclude foreign residents from reporting for any foreign source income components.

Pay As You Go Withholding Management

Foreign employers with employees working in Australia may apply for Pay As You Go withholding variations to nil, reducing administrative burden while ensuring compliance. These variations require the foreign employer to provide Tax File Numbers for all relevant employees and undertake to settle any Australian tax liability if employees default on their obligations.

Managing Withholding Variations

The variation process helps manage situations where employees remain on home country payrolls while working temporarily in Australia. However, these arrangements are now limited to two-year periods and require careful documentation and monitoring.

Withholding tax provisions vary significantly between Australian residents and foreign residents. Understanding these differences ensures you withhold the correct amount and avoid penalties for under-withholding.

Record Keeping and Documentation Standards

Businesses must maintain comprehensive records supporting all payroll decisions and classifications. This includes documentation of residency tests determinations, visa status verification, work location tracking, and foreign tax calculations. These records become crucial when employees prepare their tax return, as incorrect classifications can lead to complications during the lodgement process.

Professional service providers must now document their quality management systems and demonstrate proactive risk identification and mitigation strategies. This requirement extends to ensuring proper client disclosures, managing false and misleading statements, and providing competent services that meet professional conduct obligations.

Managing Superannuation Obligations for International Workers

Superannuation obligations for foreign workers depend heavily on both the employee’s residency status and the employer’s Australian connection. The Superannuation Guarantee applies to most employees aged 18 or older, including temporary residents such as backpackers and working holiday makers.

Understanding Your Superannuation Responsibilities

The Commonwealth Superannuation test can also affect certain government employees, though this primarily applies to Australian government employees working overseas or in specific arrangements. Understanding whether your business qualifies as resident or non-resident for tax purposes affects your superannuation obligations.

Employer Residency and Superannuation Guarantee Obligations

Australian resident employers must generally provide Superannuation Guarantee contributions for all eligible employees, regardless of where work is performed. This means continuing superannuation payments for employees who are Australian resident for tax working overseas and paying Superannuation Guarantee for foreign workers employed in Australia.

Managing Temporary Resident Arrangements

Australia maintains bilateral social security agreements with 24 countries to prevent double coverage issues. Employers can apply for certificates of coverage to exempt employees from paying into multiple superannuation systems simultaneously when working temporarily overseas.

Special Exemptions for Temporary Workers

A temporary resident may qualify for specific exemptions that reduce their superannuation obligations. However, these exemptions require careful documentation and ongoing monitoring of visa status and residency determination.

Departing Australia Superannuation Payments

International workers leaving Australia permanently can access their superannuation through the Departing Australia Superannuation Payment scheme. This process requires workers to have left Australia with expired or cancelled visas, creating administrative obligations for employers to provide necessary documentation and account details.

Tax Treatment of Departure Payments

Departing Australia Superannuation Payments are subject to final tax rates that vary based on the taxable and tax-free components of the superannuation payment. Employers should inform departing international workers about this option and provide required documentation to facilitate the process.

Fringe Benefits Tax Considerations for Foreign Workers

Fringe Benefits Tax applies to non-cash benefits provided to employees or their associates, creating additional compliance layers for businesses employing foreign workers. The interaction between Fringe Benefits Tax, employee residency status, and work location requires careful analysis to avoid unexpected tax liabilities.

How Employee Residency Affects Fringe Benefits

Whether someone is Australian resident or foreign resident affects both the benefits they can receive and your obligations as an employer. Understanding these differences helps you structure employment packages appropriately.

Fringe Benefits Tax Liability for Employers

Fringe Benefits Tax liability rests with employers, not employees, regardless of the employee’s residency status. Australian employers providing fringe benefits to employees face Fringe Benefits Tax at 47% of the taxable value, multiplied by appropriate gross-up factors. Foreign employers without sufficient connection to Australia may avoid Fringe Benefits Tax obligations on benefits provided to their employees. However, establishing insufficient connection requires careful analysis of factors including business operations, management location, and revenue sources.

Special Rules for Temporary Residents

A temporary resident receives significant Fringe Benefits Tax exemptions on benefits related to their temporary stay in Australia. These exemptions can cover housing allowances, relocation expenses, and other benefits directly connected to their temporary status. However, benefits unrelated to their temporary status remain subject to normal Fringe Benefits Tax rules.

Eligibility Requirements for Exemptions

The temporary resident exemption requires both the employee and their spouse to hold temporary visas and not be Australian residents under Social Security Act definitions. This status can change during employment, requiring ongoing monitoring and potential Fringe Benefits Tax liability adjustments.

Living Away From Home Allowances

Living Away From Home Allowances can provide Fringe Benefits Tax exemptions for employees required to work away from their usual home. For foreign workers, properly structured Living Away From Home Allowance arrangements can be exempt from Fringe Benefits Tax while remaining tax-free to employees, though concessions are generally limited to 12 months unless specific arrangements apply.

Structuring Allowances Properly

Living Away From Home Allowance eligibility requires employees to maintain their permanent home while working elsewhere for employment purposes. This creates opportunities for foreign workers on temporary assignments but requires careful structuring and documentation to access concessional treatment.

Tax treaties between Australia and other countries can also affect the treatment of certain benefits and allowances. Understanding these agreements helps improve employment packages while maintaining compliance.

Workers’ Compensation and Insurance Obligations

Workers’ compensation requirements for foreign workers involve complex considerations, particularly when employees work across state borders or internationally. Australian employers must understand their obligations and limitations when providing coverage for international team members.

Understanding Coverage Requirements

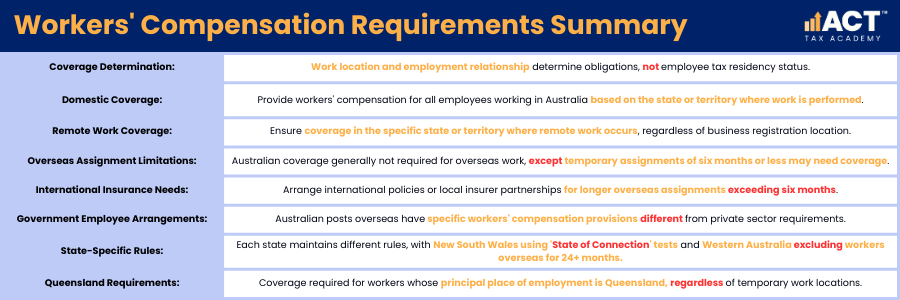

Your obligations don’t necessarily depend on whether someone is Australian resident for tax purposes or a foreign resident. Instead, they’re typically determined by work location and the nature of the employment arrangement.

Domestic Coverage Requirements

Australian employers must provide workers’ compensation coverage for all employees working within Australia, regardless of their residency status or visa type. Coverage requirements are determined by the state or territory where work is performed, not where the business is registered or the employee resides.

International Worker Coverage Limitations

Australian employers typically aren’t required to provide workers’ compensation for employees working overseas. However, temporary assignments of six months or less may still require Australian coverage, depending on the jurisdiction and specific circumstances.

Managing Overseas Assignments

International insurance policies or partnerships with local insurers in destination countries often become necessary for longer overseas assignments. Employers must carefully assess their obligations under both Australian law and destination country requirements, particularly considering the employee’s ongoing Australian residency status.

Australian posts overseas arrangements for government employees have specific workers’ compensation provisions that differ from private sector arrangements. Understanding these differences ensures appropriate coverage and compliance.

State-Specific Requirements and Exemptions

Each Australian state and territory maintain different workers’ compensation rules for cross-border and international workers. New South Wales uses a ‘State of Connection’ test to determine coverage requirements, while Western Australia provides specific exclusions for workers overseas for more than 24 months.

Queensland requires coverage for workers whose principal place of employment is in Queensland, regardless of temporary work elsewhere. These differences require careful analysis and often professional advice to ensure appropriate coverage and compliance.

Understanding how residency tests interact with state-based workers’ compensation requirements helps ensure you meet all obligations while avoiding unnecessary coverage costs.

Conclusion

Successfully managing bookkeeping and payroll implications for foreign workers requires a comprehensive understanding of tax residency rules, compliance obligations, and practical management strategies. Whether someone is Australian resident for tax purposes or a foreign resident affects every aspect of your payroll obligations, from withholding calculations to superannuation contributions and reporting requirements.

Getting the residency determination right means you’ll withhold the correct amount of tax, apply the right superannuation rates, and avoid situations where employees have paid tax incorrectly. This protects both your business from penalties and your employees from unexpected tax bills or refund delays.

Take action today by reviewing your current foreign worker arrangements, verifying your payroll software capabilities, and establishing the professional advisory relationships you need. Your international team members deserve proper support, and your business deserves the peace of mind that comes from knowing you’re fully compliant with all obligations.