Bookkeeping for Trusts vs Companies: Key Differences You Need to Know

Bookkeeping for trusts vs companies presents unique challenges that can significantly impact your business compliance and tax obligations. Choosing the wrong approach to financial record-keeping could result in costly penalties, missed deductions, or serious compliance issues with the Australian Taxation Office (ATO) and Australian Securities and Investments Commission (ASIC). Understanding these critical differences will help you maintain accurate records, meet your legal obligations, and make informed decisions about your business structure.

Why Trust and Company Bookkeeping Requirements Differ

The fundamental differences in bookkeeping requirements between trusts and companies stem from their distinct legal structures and regulatory oversight. These structural differences create varying compliance obligations, record retention periods, and reporting requirements that directly impact your day-to-day bookkeeping practices.

Understanding Company Structure Basics

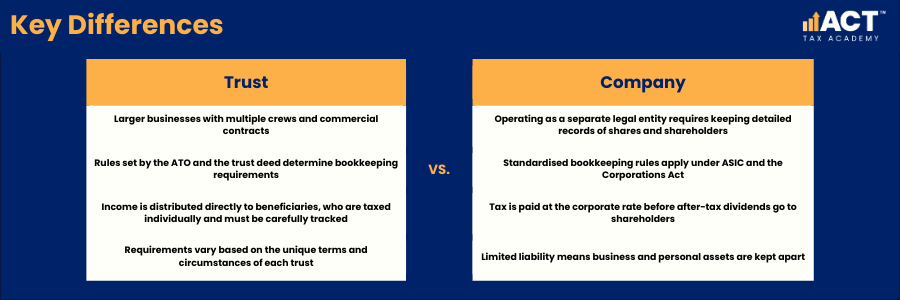

A company operates as a separate legal entity with its own right to hold assets, enter contracts, and conduct business on behalf of shareholders. This structure provides limited liability protection to investors and shareholders, meaning personal assets remain separate from business liabilities. The company structure offers perpetual existence, continuing regardless of changes in ownership or management.

Companies fall under ASIC regulation through the Corporations Act, requiring compliance with corporate governance standards, statutory reporting, and formal administrative procedures. This creates a more structured bookkeeping environment with standardised requirements across all company structures.

The company business structure must maintain detailed records of company shares, shareholders, and any holding company arrangements. Base rate entities may qualify for reduced corporate tax rates, requiring specific documentation to support their status and ensure compliance with income tax obligations.

Understanding Trust Structure Fundamentals

Trusts function differently as arrangements where trustees hold trust assets for beneficiaries. A discretionary trust allows trustees to exercise their powers in deciding how to distribute income among family members or other beneficiaries. Family trusts are particularly popular structures for small businesses seeking income distribution flexibility while maintaining asset protection for personal assets.

Trusts operate under different legal frameworks with primary oversight from the ATO for taxation purposes. The trust deed governs specific requirements, meaning bookkeeping obligations can vary significantly between different trust structures based on their individual legal documents and unique circumstances.

How Income Distribution Creates Different Requirements

The way each structure handles income creates fundamental differences in bookkeeping requirements. Companies retain profits at the corporate level and distribute dividends to shareholders. This approach means the entity pays tax at the corporate tax rate before distributing after-tax profits, creating straightforward recording procedures for dividends and capital distributions.

Trust structures distribute income directly to beneficiaries who pay tax at their individual income tax rates. This income distribution flexibility provides potential tax benefits by allowing trustees to distribute trust income to family members in lower tax brackets. However, it requires detailed tracking of beneficiary entitlements and comprehensive documentation of distribution decisions. When distributing capital gains or franked dividends, trustees can stream these amounts to specific beneficiaries if allowed by the trust deed and in compliance with ATO rules.

Discretionary trusts offer particular advantages for family businesses, allowing trustees to make key decisions about income allocation based on beneficiaries’ specific circumstances. Unit trusts operate differently, with fixed entitlements that simplify distribution calculations but reduce flexibility in tax planning.

Record-Keeping Requirements: Documentation and Retention

Understanding what records you must maintain and for how long represents a critical difference between trust and company bookkeeping. These requirements directly impact your storage systems, documentation processes, and compliance strategies.

Essential Trust Records and Documentation

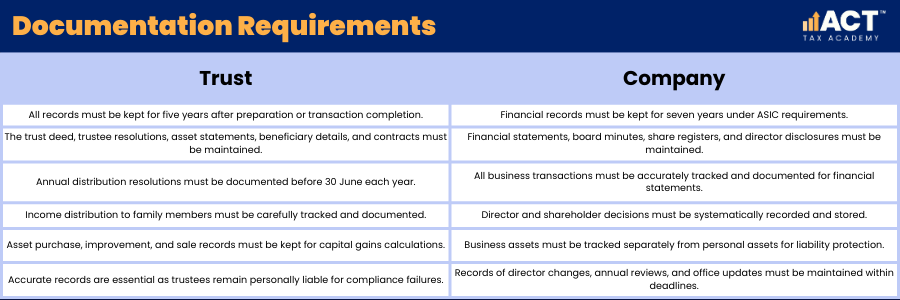

Trustees should maintain all trust records for at least five years after the tax return is lodged, and longer for records relating to asset acquisitions, improvements, or disposals to accurately calculate capital gains.

While the ATO does not require written resolutions unless specified in the trust deed, it is best practice to document all income distribution decisions before 30 June to establish beneficiary entitlements for the year.

Managing Family Trust and Beneficiary Records

Family trust bookkeeping must carefully track income distribution to family members, ensuring proper documentation of each beneficiary’s entitlement. The trustee bears responsibility for accurate record-keeping, as they remain personally liable for trust tax obligations and compliance failures.

Capital gains tax documentation requires particular attention for trust assets. Trustees must maintain detailed records of asset acquisitions, improvements, and disposals to calculate capital gains accurately. This documentation becomes crucial when beneficiaries receive distributions of capital gains, as proper streaming requires specific compliance with ATO requirements.

Company Record-Keeping Essentials

Companies must maintain financial records for at least seven years, but certain documents such as share registers, minutes of meetings, and company constitutions may need to be retained permanently. These records must accurately track transactions, explain the company’s financial position, and enable preparation of auditable financial statements.

ASIC compliance demands comprehensive documentation including financial statements, board meeting minutes, share registers, director disclosures, and significant contracts. Companies must also maintain records supporting annual reviews, director changes, and registered office updates within strict timeframes.

Maintaining Separate Legal Entity Status

Company bookkeeping must track business assets separately from personal assets, maintaining the separate legal entity status that provides limited liability protection. This separation requires careful documentation of all transactions between the company and its shareholders or directors to avoid potential legal complications.

The company structure requires systematic recording of key decisions made by directors and shareholders. Unlike trust resolutions that focus on income distribution, company resolutions cover broader governance matters including capital raising, dividend declarations, and strategic business decisions.

Digital Records and Modern Storage Solutions

Both companies and trusts can maintain electronic records. Companies typically handle more documentation for governance and compliance purposes, but both structures must ensure records are secure, complete, and accessible for audits or tax reviews.

Modern bookkeeping systems should accommodate the specific needs of each structure, whether tracking beneficiary distributions for trusts or maintaining corporate governance records for companies. Cloud-based solutions offer advantages for both structures, providing secure storage and easy access for compliance reporting.

Compliance Obligations and Reporting Differences

The compliance landscape varies significantly between trusts and companies, affecting your bookkeeping workload, reporting deadlines, and administrative complexity throughout the year.

Trust Tax Compliance and Annual Reporting

Trusts must lodge annual tax returns regardless of income levels, including detailed distribution statements showing how income was allocated to beneficiaries. The trust income schedule must document all distributions, with specific limits on the number of distributions that can be reported efficiently.

Distribution deadline management creates time-sensitive bookkeeping requirements. Trustees must resolve income distributions by 30 June, with specific streaming requirements for capital gains and franked dividends. Missing these deadlines results in the trustee paying tax at the highest marginal rate, significantly impacting the trust’s tax effectiveness.

Managing Trustee Responsibilities and Obligations

Family trusts require careful management of beneficiary records, ensuring all family members’ details remain current for tax reporting purposes. Corporate trustees may simplify some administrative aspects while maintaining the same fundamental compliance obligations for the trust structure.

The obligation imposed on trustees extends beyond simple tax compliance. Trustees must ensure proper asset protection measures are maintained, keeping trust assets separate from personal assets and maintaining the trust’s legal integrity.

Company Tax and ASIC Compliance Requirements

Companies face more extensive compliance obligations through both ASIC and ATO reporting. Annual ASIC reporting includes lodging annual statements, financial reports for applicable companies, and updating company details within prescribed timeframes.

The corporate tax rate applies to company profits, with base rate entities potentially qualifying for reduced rates based on their turnover and business activities. Proper documentation of eligibility criteria becomes essential for claiming these tax benefits and maintaining compliance with income tax obligations.

Additional Company Reporting Obligations

Companies with employees face additional compliance requirements including Pay As You Go (PAYG) withholding, superannuation obligations, and regular Business Activity Statement lodgements. This creates ongoing bookkeeping obligations throughout the year beyond annual compliance requirements.

While dividend payments are generally more straightforward than discretionary trust distributions, proper documentation of franking credits, shareholder notices, and compliance with corporate law remains essential.

Comparing Administrative Complexity

Trust administration focuses primarily on income distribution documentation and beneficiary management, with flexibility that can accommodate changing family circumstances and tax planning objectives. The discretionary nature of most family trusts allows for responsive tax planning but requires more detailed documentation of trustee decisions.

Companies require systematic governance documentation, regular statutory compliance, and formal meeting procedures that significantly increase bookkeeping complexity. However, the standardised nature of company compliance makes requirements more predictable and potentially easier to systematise for ongoing management.

Practical Considerations for Business Owners

Choosing between trust and company structures significantly impacts your daily bookkeeping operations, software requirements, and professional service needs. Understanding these practical implications helps you prepare for the ongoing administrative commitment each structure requires.

Trust Bookkeeping Software Requirements

Trust bookkeeping typically requires features for beneficiary management, distribution tracking, and resolution documentation. Your accounting software should accommodate multiple beneficiary records, distribution calculations, and tax reporting capabilities specific to trust structures.

The system should handle the complexity of income distribution flexibility, allowing for different allocation percentages among beneficiaries and proper tracking of capital versus income distributions. Integration with tax preparation software becomes particularly important for trusts due to their complex reporting requirements.

Company Bookkeeping System Features

Company bookkeeping demands comprehensive financial reporting capabilities, ASIC compliance features, and payroll management systems if the company has employees. Look for software that handles corporate governance documentation, director records, and statutory reporting requirements efficiently.

Trust Professional Service Needs

Trusts often require legal advice for trust deed interpretation, distribution strategy, and compliance matters. The complexity of trust law and varying deed requirements typically necessitate ongoing professional guidance, particularly when making key decisions about asset protection strategies or income distribution.

Understanding the trustee’s powers and limitations requires professional expertise, especially when dealing with complex family circumstances or significant business assets. Professional advisers can help understand the obligation imposed on trustees while maximising potential tax benefits.

Company Professional Service Requirements

Companies benefit from accounting and corporate secretarial services to manage ASIC compliance, governance requirements, and financial reporting obligations. The standardised nature of company compliance makes professional service relationships more predictable, though companies may require additional services for complex corporate structures or holding company arrangements.

Understanding Cost Implications for Trusts

Trust bookkeeping costs vary significantly based on the complexity of beneficiary structures and distribution strategies. Simple family trusts with few beneficiaries require minimal ongoing bookkeeping, while complex arrangements with multiple entities or sophisticated asset protection strategies demand extensive record-keeping.

The tax effective nature of trust structures can justify higher administration costs through tax savings achieved via income distribution flexibility. However, trustees must weigh these benefits against the ongoing compliance burden and potential risks of personal liability for trust obligations.

Evaluating Company Structure Costs

Company structures involve consistent annual costs for ASIC compliance, potential audit requirements, and ongoing governance documentation. However, standardised requirements make budgeting more predictable compared to trust structures, and the limited liability protection may justify these costs for many businesses.

The corporate tax rate and availability of franking credits can provide tax benefits for companies, particularly where profits are retained for business growth or distributed to shareholders in higher tax brackets. Companies qualifying as base rate entities (turnover under $50 million and less than 80% of income is passive) pay the lower 25% corporate tax rate instead of the standard 30%, provided documentation supports eligibility.

Making the Right Choice for Your Business

Understanding these bookkeeping differences empowers you to make informed decisions about your business structure and how to provide asset protection. It’s important to consider the level of compliance you are comfortable with, what record-keeping resources you have, and your long-term business plans before making a choice.

A trust structure can provide asset protection and flexibility, supporting families and those wanting to manage tax outcomes. Meanwhile, a company structure may be more suitable if you need formal governance, future investment, or consistent compliance processes.

Think about how these differences could affect your day-to-day business operations and future growth. Choosing the right approach now can help you stay on track with your obligations and achieve the asset protection your business needs.