Understanding the $18,200 Tax-Free Threshold: What It Means for Australian Small Business Owners

Understanding the $18,200 tax-free threshold helps you work out how much you can earn before you pay tax as a small business owner in Australia. It affects your taxable income; how much tax is withheld from your pay and how much tax you owe at tax time. When you get it right, you keep more money in your pocket and avoid an unexpected tax bill at the end of the financial year.

What Is The $18,200 Tax-Free Threshold?

The tax-free threshold is the amount most Australian residents can earn in a full year before they start paying income tax, currently set at $18,200. In simple terms, you pay no tax on this income if your taxable income for tax purposes stays at or below that level for the financial year. This applies whether your income comes from employment, your own small business or other income such as investments.

Once your taxable income goes above $18,200, you move into the first tax bracket and start paying tax only on the dollar amount above the threshold. Higher bands apply as your income rises, but the first $18,200 remains tax free, which reduces the average tax you pay on your total income. The result is that low-income earners and those in their first year of business can keep more of their take home pay while they get established.

- The tax-free threshold applies to your total taxable income, not to each job separately

- First $18,200 of taxable income: tax free

- Income above $18,200: taxed at the relevant tax rates for Australian residents

Why Does the Tax-Free Threshold Matter to Small Business Owners?

For small business owners, the tax-free threshold influences how much you should draw from your business and how much tax you need to set aside. If your combined income from your job, business and investments remains below $18,200, you may have no income tax payable, even if some tax was deducted along the way. If your income goes higher, the threshold still works in your favour by making the first part of your income tax free.

This threshold also shapes decisions about how to structure your pay, especially when you move from one job into running your own business or when you have multiple jobs. It affects how your payer or employer withholds tax during each pay period and whether you end up with a refund or tax debt when you lodge your tax return online or through an agent. For many owners, understanding these rules removes guesswork and helps them avoid surprise tax bills.

How Does The $18,200 Tax-Free Threshold Work In Practice?

In practice, the $18,200 tax‑free threshold means you can earn $350 per week, $700 per fortnight or $1,516.67 per month before income tax applies. Note that the Medicare levy has separate thresholds and may still apply even if your income is below $18,200. If you claim the tax-free threshold with your main payer using a TFN declaration, they will withhold less tax from your pay so that you benefit from the threshold across the full year. This usually happens through your employer’s payroll system when you start a new job or when you begin paying yourself through your own company.

At the end of the financial year, the Australian Taxation Office looks at your taxable income from all income sources, including employment, business income and investments. If the total tax withheld during the year was higher than the tax payable on this income, you receive a refund; if not enough was withheld, you may owe extra tax. That is why it is important to think about your income for the full year rather than just one pay period.

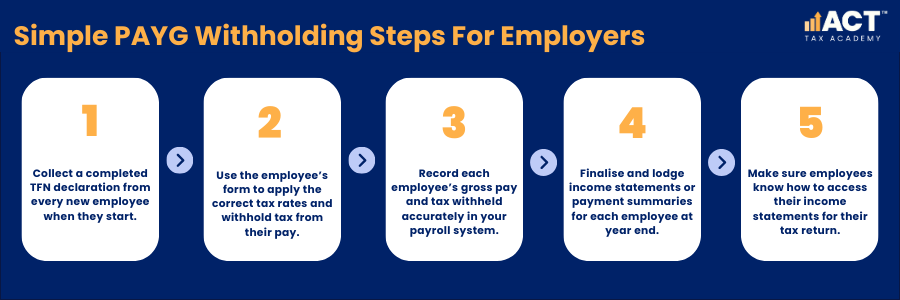

How Does The Tax-Free Threshold Affect Employees You Pay?

If you employ staff, each worker can choose whether to claim the tax free threshold from your business. Most cases involve the employee filling in a TFN declaration when they start, which tells you whether your business is their first job or one of their subsequent jobs. If they claim the threshold with you as their main employer, you withhold tax at a lower rate, which increases their take home pay each pay period.

Employees should generally claim the threshold from only one employer, otherwise less tax than required may be withheld from their combined income. If a worker claims the threshold from two or more jobs at the same time, they may face a tax debt when they lodge their tax return because not enough tax was deducted overall. As an employer, you simply follow their TFN declaration and the tax tables for Australian residents, but you can encourage them to check the ATO website if they are unsure. affects assets such as investment property, managed funds, plant, vehicles, and major office equipment.

What Happens If You Have Multiple Income Sources Or Jobs?

Many small business owners have multiple jobs or income sources, such as a part-time job, a growing side business and some investments. The tax-free threshold still only applies once to your total taxable income for tax purposes, not to each job separately. This means you need to think about your combined income for the full year, not just what you earn from your first job or from your business alone.

If you have more than one employer, you should claim the tax‑free threshold only from the employer who pays you the most, and not from any second or subsequent jobs. The second job and subsequent jobs then withhold tax at a higher percentage so that enough tax is collected overall, even though those individual amounts might seem small. This approach reduces the risk of a tax bill when your combined income is added up at tax time.

How Do Different Business Structures Change The Picture?

Your business structure changes how you get paid and how the tax-free threshold applies, but it still applies at the level of the individual taxpayer. As a sole trader, your business income is your own income, so the threshold applies to your net taxable income after deductions such as business expenses and superannuation contributions. As a company or trust owner, you may receive a mix of salary, director’s fees, distributions and dividends, each with its own tax treatment.

Whatever the structure, your personal tax return pulls together all your income and applies the tax-free threshold once. Choosing how to split income between wages and other payments can affect the tax bracket you fall into and how much tax is withheld during the year. Good planning helps you manage your tax obligations and still keep enough money in the business account to fund growth.

How Does the Tax-Free Threshold Interact with Medicare Levy and Other Levies?

The tax-free threshold works alongside other parts of the system, such as the Medicare levy, the Medicare levy surcharge and various tax offsets. Even if the first $18,200 of taxable income is tax free for income tax, the Medicare levy may apply once your income exceeds the Medicare levy threshold (e.g., $26,000 for singles in 2024–25), which is separate from the $18,200 tax‑free threshold. Some taxpayers may also face an extra Medicare levy surcharge if their income is higher and they do not have appropriate private health insurance.

Low- and middle-income earners may be eligible for the Low-Income Tax Offset (LITO), which can reduce tax payable by up to $700 for incomes up to $37,500, phasing out by $66,667. These offsets do not affect how much tax is withheld during each pay period, but they can change the final result when you lodge your tax return. For small business owners, understanding the combined effect of the tax-free threshold, Medicare levy and offsets is key to estimating how much tax they will actually pay.

What Are Common Mistakes With The Tax-Free Threshold?

A common mistake is claiming the tax-free threshold from more than one employer at the same time, especially when people pick up a new job or work multiple jobs. When this happens, each payer may withhold tax as if you are only earning from them, so less tax than needed is deducted from your combined income. At tax time, this can turn into an unexpected tax debt, even if your take home pay during the year felt comfortable.

Another frequent issue is assuming that if no tax was withheld, no tax will be payable, even when other income or previous years’ profits are involved. People can also run into trouble when they do not update their TFN declaration or fail to consider business income and investments on top of employment income. These errors make tax affairs more stressful and can lead to extra tax plus interest if you do not stay on top of your tax obligations.

How Can Small Business Owners Use The Threshold In Their Tax Planning?

Small business owners can use the tax-free threshold as part of a simple plan to manage how much tax they pay and when they pay it. In a lean year, you might choose to keep your drawings close to the threshold so you pay less tax and leave more money in the business. In stronger years, you might accept that you will move into a higher tax bracket and plan your cash flow so that tax payable does not come as a shock.

If you have family members involved in the business, you may be able to spread income across more than one person so that more than one tax-free threshold is used, within the rules. Choosing when to draw extra pay, when to reinvest profits and how much to contribute to superannuation are all levers that affect your final tax bill. Thoughtful planning also makes it easier to pay any PAYG instalments on time and keep your tax account with the Australian Taxation Office in good standing.

When Should You Seek Help with the Tax-Free Threshold?

You should seek advice when your income changes significantly, such as when you move from one main job into your own business or start earning other income from investments. It also makes sense to get help when you take on multiple jobs, change employers or begin paying yourself through your own company. These shifts can change how much tax is withheld by each payer and whether you should claim the tax-free threshold with a new employer.

Professional guidance is especially useful if you are unsure how much tax you will owe or whether you are on track for a refund. Getting help means your tax return, payment summaries and other details line up properly with the information held by the Australian Taxation Office. That way, your tax affairs stay simple, your tax obligations are met, and you can focus more of your energy on growing your business and looking after your clients.